It’s not just the usual suspects: some oil exporters also have low official reserves levels.

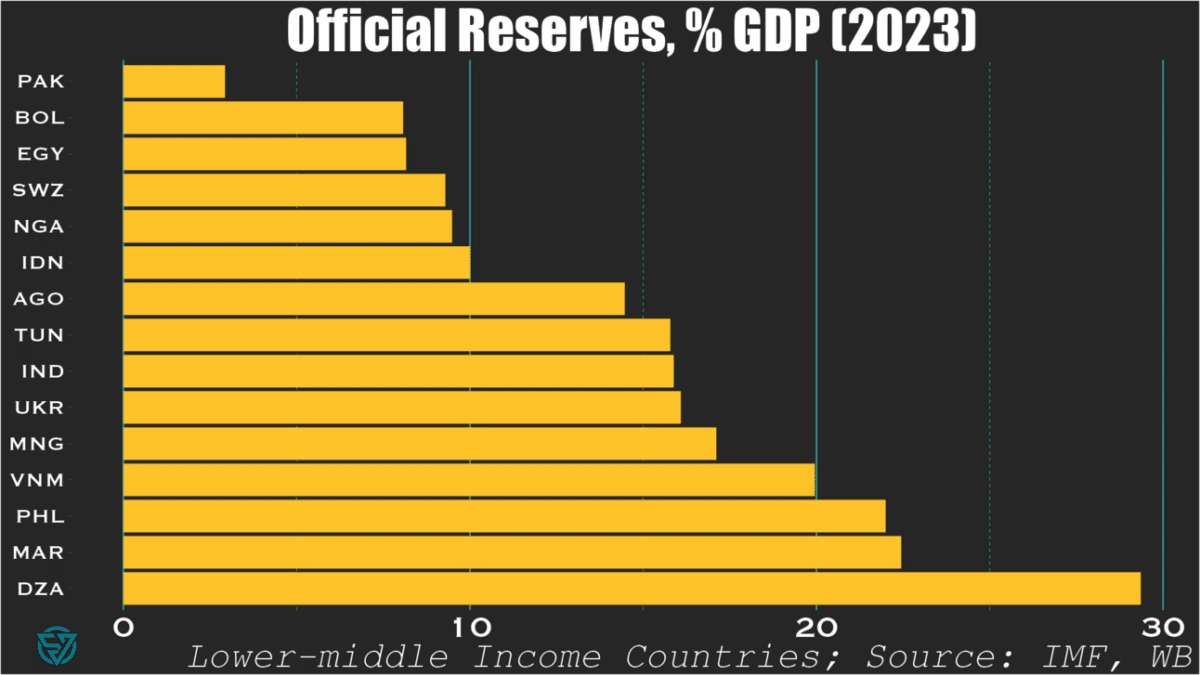

When writing last week’s piece on the IMF’s shoddy deal with Pakistan, I was blown away at the country’s astonishingly-low level of international reserves.

$9.5 billion for a $350 billion economy. That’s only around 3% of GDP and 1-2 months of import cover. Such a low amount of cash on hand isn’t exactly best practice, whether it’s sovereign, corporate, or personal finance.

So it got me thinking: is Pakistan really such an outlier? Or am I just crazy or ill-informed?

Lower-middle income countries

Turns out I was right: among countries in its income bracket, Pakistan has the lowest reserves-to-GDP ratio of all.

Bolivia, Egypt, Swaziland, Nigeria, and Indonesia are not far behind, at 10% or less.

Yet international reserves are far from the only macro indicator that matters of course. So I suppose we should be forgiving of Indonesia, which generally has much of its (macro) house in order.

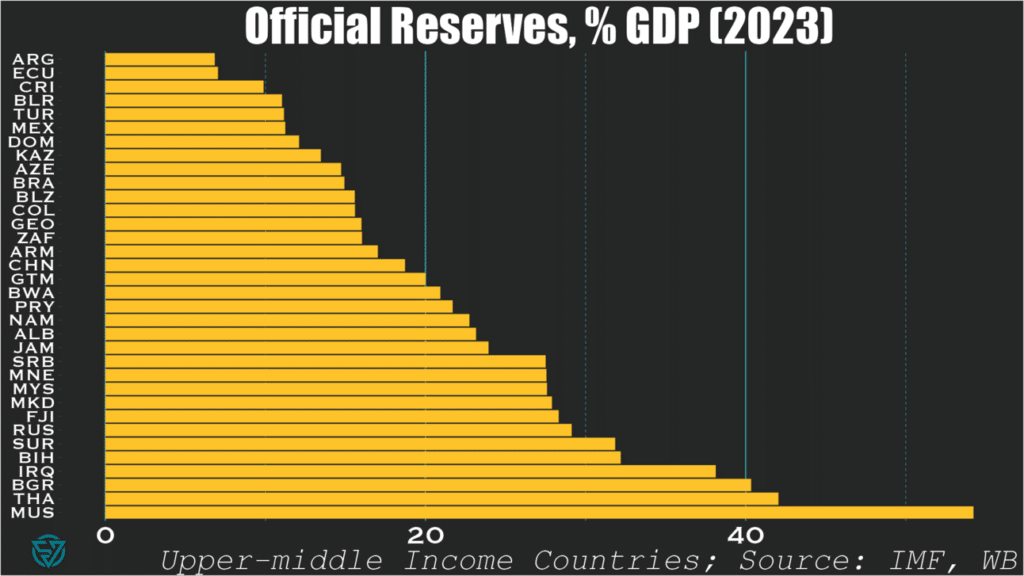

Upper-middle income countries

Looking at upper-middle income countries, only three in-sample are sub-10%: Argentina, Ecuador, and Costa Rica. I suppose Latin America really does have a savings problem.

As expected, these slightly richer countries generally exhibit higher reserve-to-GDP ratios than their poorer counterparts. No surprise there.

What is surprising, however, is to see oil-exporters like Azerbaijan, and Kazakhstan sub-15 percent.

Mexico, Brazil, and Colombia also produce oil and also have low ratios. But, then again, they are also Latin American…

“What’s the big deal?”, I hear you asking.

Well, Ukraine is a lower-middle income country fighting a war and undergoing debt restructuring. Yet Kyiv still manages to have more in the bank than wealthier countries with much lower-levels of security threats.

To me, that speaks volumes about economic management.

Pakistan and the IMF recently agreed on a program worth $7 billion, which appears woefully insufficient to resolve the country’s macroeconomic imbalances. The Fund claims that the Extended Fund Facility over the next 37 months intends to “cement macroeconomic stability and create conditions for a stronger, more inclusive, and resilient growth.” But this nothingburger of a deal – painfully, obviously so ($2.3 billion per year?) – will more likely achieve the opposite.

Some quick stats from 2023 pulled from my sovereign stress tracker, where Pakistan flashes red on reserve cover and debt-to-revenue:

Average annual interest payments over the next five years = ~6.5% / GDP (~$20 billion)

Average annual principal payments over the next five years = $19 billion

Imports typically range from $60-85 billion

Export revenues range from $30-40 billion

Tax revenues = ~10% / GDP (~$35 billion)

In 2023, the current account deficit narrowed to -0.7% of GDP (-$2.4 billion), but in the past these have been much larger (e.g. ~-$17.5 billion in 2022). But even financing small external deficits could prove difficult. With annual FDI generally under $2 billion and in the absence of other private capital inflows, the government will likely have to borrow more. This is a problem given already-high public debt levels at 77% / GDP, of which Pakistan owes 28% / GDP to external creditors.

So it is crucial that Pakistan runs small current account deficits or, dare I say it, surpluses. If the global trading system worked as it should (i.e. fantasy-land), non-commodity-exporting emerging and frontier economies should be expected to run current account deficits. The idea is that the current account surpluses of wealthy countries would fund the development and climate transition of poorer nations.

But since so few advanced economies run surpluses, I guess this nuclear power and world’s fifth-most populous country will just have to tighten its belt. Fantastic.

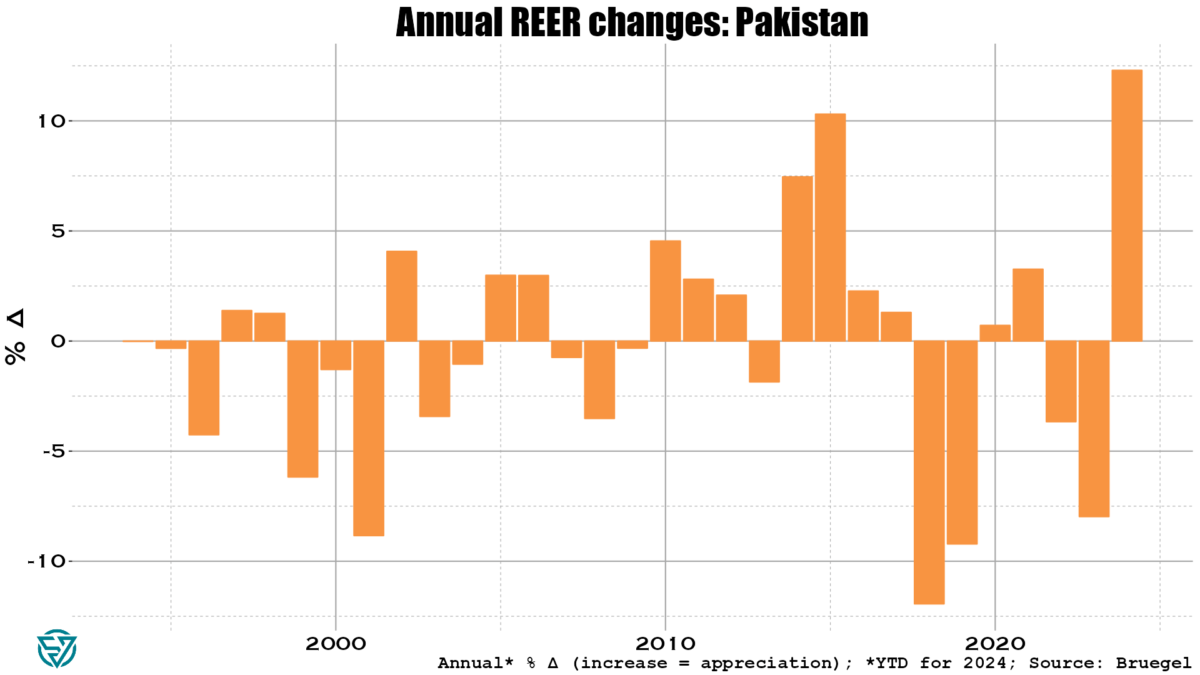

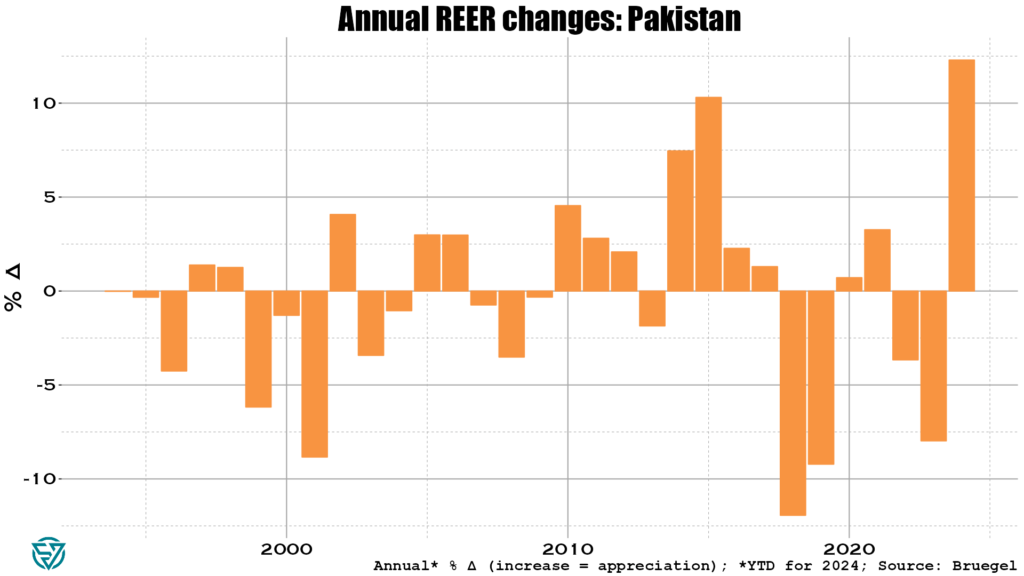

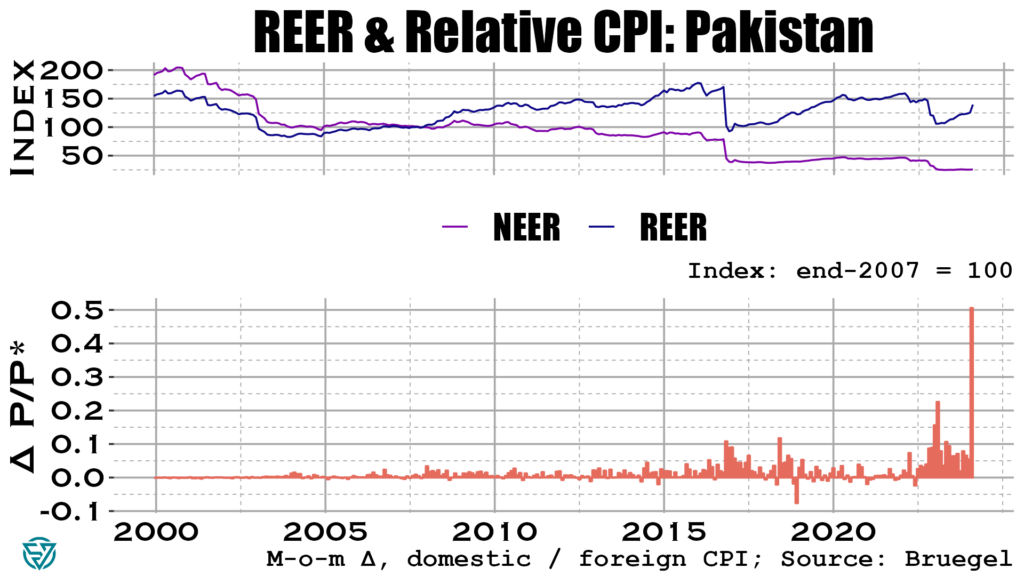

To avoid large external deficits, Pakistan’s real exchange rate needs to depreciate. Yet the exact opposite is happening, so don’t hold out too much hope for a small CAB deficit this year:

Olivier Blanchard once said that inflation is the canary in the coal mine. In the chart below you can see that Pakistan’s weighted inflation differential with its trading partners skyrocketed in May 2024.

Consider the alarm sounded. Even on the off-chance Pakistan manages to run a small CAB deficit in 2024 (say, like the -$2.4 billion in 2023), annual IMF support ($2.3 billion) will barely help bridge that gap. Islamabad still has to cough up about $39 billion in combined principal and interest payments every year going forward. This sum is roughly equivalent to export receipts and slightly larger than tax revenues.

This looks to be a solvency issue. And with inflation through the roof, it’s hard to see how this doesn’t get worse before it gets better. Watch this space.

Behold the dashboard for low- and middle-income country external sovereign debt!

After peaking at $188 billion in 2021, for the first time in two decades the stock of low- and middle-income country sovereign debt that China holds declined in 2022. At just under $181 billion, this is still more than the US, France, the UK, Germany, Italy, and Canada combined. Nevertheless, this reversal confirms China’s pullback from its Belt and Road Initiative-driven lending that began in the early 2010s. It is also part of a broader global trend that saw LMICs’ external debt stock dip by $43 billion, from $3.490 trillion in 2021 to $3.447 trillion in 2022. Higher global interest rates are certainly part of the story.

China’s exposure to LMICs is $181 billion.

G7 ex-Japan exposure to LMICs is $161 billion.

There has been no shortage of coverage in recent years on Chinese lenders holding off on new loans to emerging and developing economies. Indeed, Beijing has been reconsidering its Belt and Road Initiative even as its sovereign lenders grapple with the consequences of having such large exposures to EMDEs for the first time. Chief among these of course have been the debt restructurings of recent years, which have underscored how the preferences of Chinese creditors diverge from those of other lenders.

The sharpest drops in percentage terms came in other private lending, which includes trade finance, and in the bilateral concessional category. While we shouldn’t read too deeply into this, I can’t help but muse that decreasing export credits is consistent with worsening frictions between China and its trading partners. Similarly, the drop in concessional overseas lending shouldn’t come as too much of a surprise in the context of domestic financial strains, as China’s property crisis roils onward.

bn USD

2022

2021

% Δ

$ Δ

Bilateral: Concessional

6.6

7.1

-7.8

-0.6

Bilateral: Non-Concessional

142.3

147.7

-3.6

-5.4

Private: Commercial Banks

29.1

30.1

-3.2

-1.0

Private: Other (incl. ECAs)

2.8

3.1

-10.3

-0.3

Total

180.8

188.0

-3.8

-7.2

Chinese lending to lower and middle income sovereign borrowers

Among LMICs, low-income countries are already feeling quite the pinch at China’s relative withdrawal. Chinese exposure to LICs has dropped by a full percentage point of GDP in just the space of a couple years. This is equivalent to a roughly 25% decline relative to output, as Chinese-held LIC debt has decreased from ~4% to ~3% of GDP since 2020.

Geographically, the outgoing Chinese tide is also affecting Africa. In 2022, China held less than $80 billion of African external debt, the lowest reading since 2018. While Sub-Saharan external debt actually increased in 2022, the pace has slowed compared to previous years. This reflects the lower exposure and significant weight of Chinese creditors, as they account for 1/6th of the $480 billion in global holdings of African external debt.

The World Bank’s International Debt Statistics are one of the top resources in the sovereign debt space. The data is released with about a year’s lag, meaning that full year data is currently only available through the end of 2022. But, as you can see, it’s such fertile analytical ground. So feel free to use this dashboard for your own purposes. Also available here.

EMDE sovereign borrowers walk a tightrope in the fragmented creditor landscape.

One of the main themes permeating the 7th edition of the Sovereign Debt Research and Management Conference – aka “DebtCon” – held in Paris on 29-31 May was the increasingly challenging environment that sovereign borrowers face in accessing international capital and managing their balance sheets. These challenges are numerous and complex, with some of the best-known ones being the more diverse creditor landscape, implementation problems of key policies such as the G20’s Common Framework of Debt Treatments beyond the DSSI, and geopolitical fragmentation.

The Chinese impact

DebtCon is a particularly useful forum for finding solutions to the day’s most pressing sovereign debt policy issues. Not only does it bring together stakeholders from across much of the sovereign space, including borrowers, creditors, academics, and practitioners, but the conference is also focused and small enough for participants to exchange ideas more efficiently than at larger, sprawling events.

One of the most impactful discussions was the closing panel, which addressed the geopolitics of sovereign debt and best encapsulated the myriad challenges in the space. Take, for instance, increased creditor diversity: one of the key newer features – alongside the emergence of bondholders – is that China has established itself as the world’s largest bilateral creditor to lower- and middle-income countries over the past decade plus. Resolving debt crises has become harder as a result, with more debt exposure to China making it less likely for a sovereign borrower to complete a Paris Club restructuring. Similarly, debt to China is associated with longer negotiating times for IMF programs.

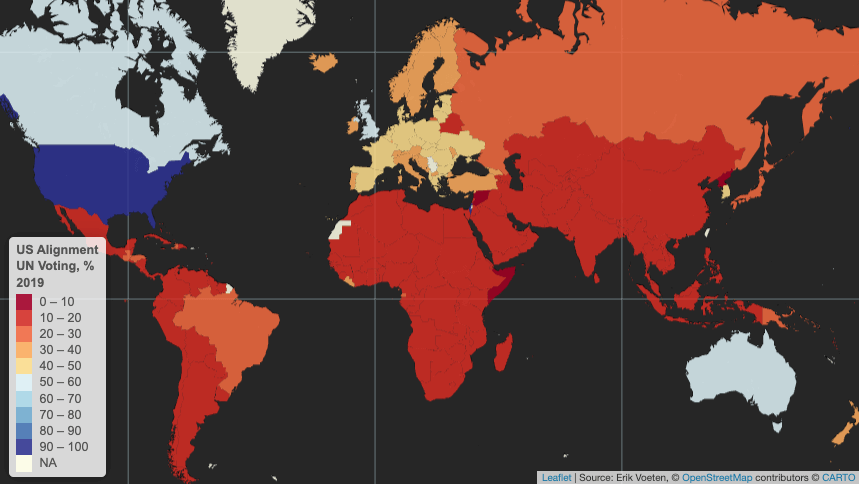

United Nations voting patterns

Yet emerging and developing economies as a whole are much more geopolitically-aligned with China than they are with the US. Using the latest available data on countries’ voting patterns in the United Nations’ General Assembly, in 2019 only a few EMDEs voted in alignment with the US more than 20% of the time. None did so in more than 50% of votes.

Only a handful of US allies tend to vote with the US in UN General Assembly votes more than half the time: Israel, Canada, the UK, Australia.

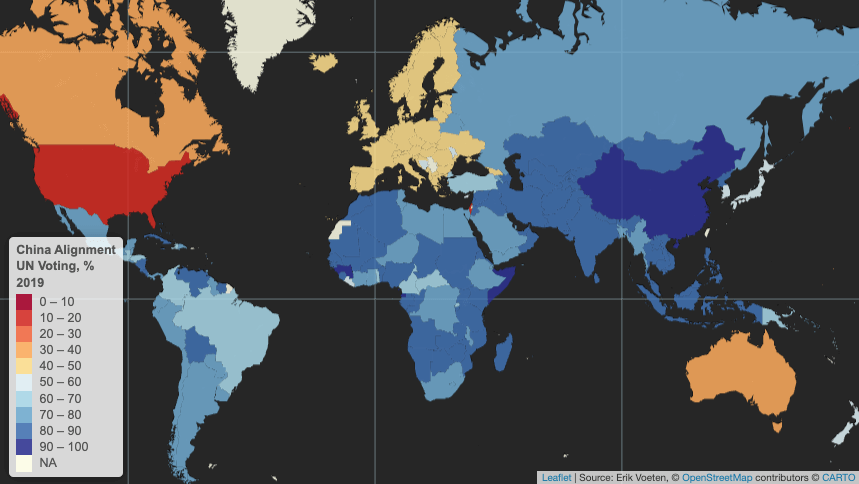

In contrast, EMDEs tend to vote in lockstep with China, which, after all is still considered somewhat of an emerging market itself. Virtually no EMDE votes outside of Europe were misaligned with China in the UN more than 50% of the time in 2019. Geopolitics is of course more complex than suggested by UN voting, and the world is not reverting to Cold War-era bipolarity, with multipolarity seemingly emerging on the horizon instead.

Sovereign borrowers in the “Global South” are aligned with China more often than not in UN voting.

Walking a tightrope

Nevertheless, the above data suggests that sovereign borrowers are navigating a complex environment in which they have to walk a tightrope between managing relationships with Chinese creditors and maintaining access to IMF support and lending from the Paris Club and private creditors. As such, some EMDE governments may not see that it is in their best interests to ask their largest creditors, which are often Chinese, to take steep haircuts during debt resolutions as has often been the case with past Paris Club restructurings and the Common Framework.

Instead, countries in debt distress may prefer to ask China for maturity extensions and for maintaining exposure while they implement structural reforms to set debt on a more sustainable path. This approach has the potential drawback of conflicting with or delaying IMF program negotiations, which typically require financing assurances from key creditors. Even so, some sovereign borrowers – especially those that are among Beijing’s strategic partners – may judge that their relationship with China is more important in terms of resources than IMF program sizes.

Still others may prefer to rely more on the G20’s Common Framework and the IMF and World Bank. This is especially true considering that Chinese lending to EMDEs has slowed to a trickle over the past five years as Beijing reconsiders its Belt and Road Initiative ambitions.

A poorly-functioning global trading system

Yet the drawback of relying on G7 countries and the Anglosphere for sovereign lending is that, ultimately, among these only Germany and Japan run meaningful current account surpluses. And while bilateral aid from the G7 is non-negligible, external deficits in the US, UK, Canada, and (historically) Australia mean that global capital flows towards these countries rather than from them to the world, as is the case with China.

One way to increase capital flows from rich to poor countries would be for more rich countries to begin running current account surpluses, which would effectively overhaul the global trading system. This is a highly unlikely outcome over the short- and medium-terms, for many reasons but partly because doing so would affect the US dollar’s reserve currency status, the ability to weaponize the dollar via sanctions, and undermine the power of US banks. In these murky waters, it is a small wonder then that many EMDE sovereign borrowers will continue to prefer to hedge their bets by viewing China as at least as important as the IMF and other creditors combined.

Today’s charts are an update of the Sovereign Vibe sovereign debt stress tracker initially released in 2023. This tool is based directly on the IMF’s Debt Sustainability Framework for Market-Access Countries, released in 2021, and is relevant only for countries that “principally receive financing through market-based instruments and on non-concessional terms.” Through extensive testing, the IMF developed a model that measures the probability of a borrowing country experiencing sovereign debt strains in the near-term based on changes in nine macroeconomic and governance variables.

Results

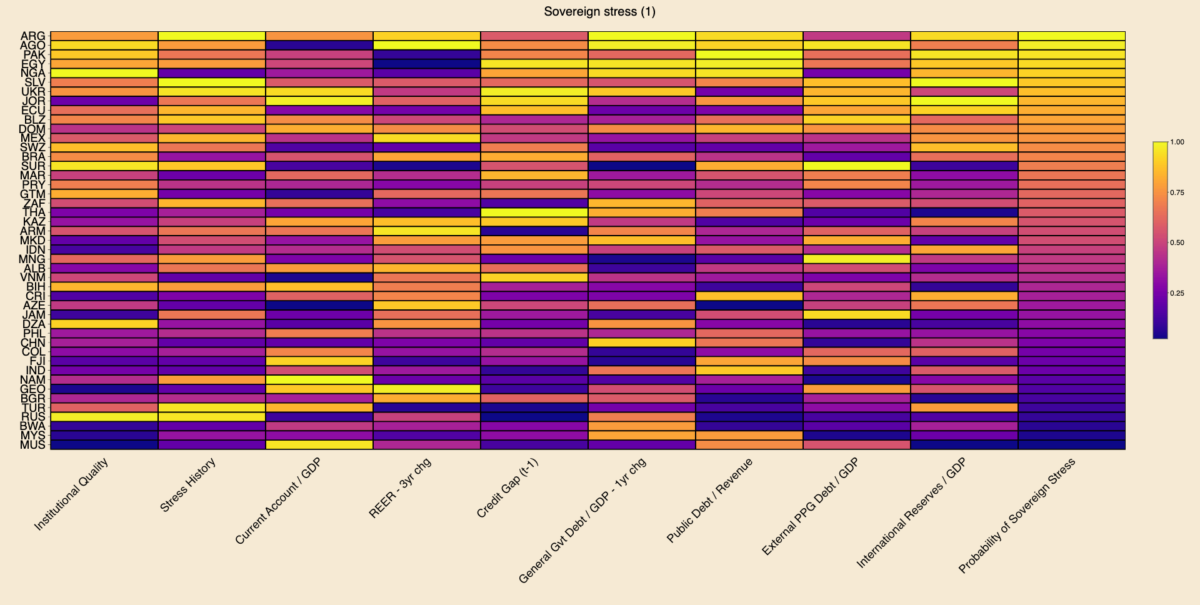

Among middle- and lower-income countries with market access with full data availability across all indicators, Argentina, Angola, and Pakistan are most at risk of sovereign debt stress. In the heatmap below, brighter colors indicate more risk, while darker colors indicate less risk. I use percentile scoring for each variable, including the probability of sovereign stress outcome.

Argentina defaulted on local currency debt in 2023, which penalized the country via the “stress history” indicator and propelled it into the “top” spot. The sovereign defaults that I tallied based on S&P for 2023 are El Salvador, Cameroon, and Ethiopia on foreign currency debt and Argentina, Ghana, El Salvador, Mozambique, and Sri Lanka on local currency. Let me know if I am missing any!

Caveats

Regarding the other 2023 sovereign defaults, El Salvador registered as sixth-most at risk of sovereign stress. I would expect Sri Lanka to rank fairly high on the sovereign stress heat-map above. But data for Sri Lanka has been patchy since its 2022 default, preventing me from making a full calculation on the same footing as other countries.

The IMF does not consider Cameroon, Ethiopia, Ghana, and Mozambique to currently be MACs. Other countries are borderline. For instance, Angola has been a market-access country for several years, but it seems like the IMF is in the process of declassifying it due to current vulnerabilities. So I may remove Angola from the next update. On the other hand, Nigeria still seems to be within the IMF’s MAC perimeter.

Also, this tracker shouldn’t be taken as gospel as to the likelihood of sovereign stress, as it only reflects macroeconomic-related indicators and which are mostly backward-looking. It fails to capture the qualitative aspects of a government’s commitment to reforms. Case in point: I wrote of Egypt’s brightening prospects last week.

Changes since October 2023

The table below outlines changes in the ten MACs most at-risk of experiencing sovereign debt strains. Argentina, Nigeria, and Ukraine have deteriorated by climbing up the ranking. Angola, Pakistan, Egypt, Jordan, Ecuador, Belize, and Mexico have seen their rankings improve. El Salvador continues to occupy the sixth spot.

Rank

May 2024

October 2023

🥇

🇦🇷 Argentina ⬆️

🇦🇴 Angola

🥈

🇦🇴 Angola ⬇️

🇵🇰 Pakistan

🥉

🇵🇰 Pakistan ⬇️

🇪🇬 Egypt

4

🇪🇬 Egypt ⬇️

🇯🇴 Jordan

5

🇳🇬 Nigeria ⬆️

🇦🇷 Argentina

6

🇸🇻 El Salvador

🇸🇻 El Salvador

7

🇺🇦 Ukraine ⬆️

🇪🇨 Ecuador

8

🇯🇴 Jordan ⬇️

🇧🇿 Belize

9

🇪🇨 Ecuador ⬇️

🇩🇴 Dominican Republic

10

🇧🇿 Belize ⬇️

🇲🇽 Mexico

I was surprised to see Mexico in October’s top ten, which points to some of this tool’s analytical limits. I and many others have generally perceived Mexico as a positive EM story in recent years, with an economy benefiting from supply chain reconfigurations and near-shoring, and an appreciating peso. Nevertheless, this IMF model can help challenge consensus narratives: in fact, Mexico is penalized precisely because of the strong appreciation of its real effective exchange rate over the past three years.

Angola, Pakistan, Egypt, Jordan, Argentina, El Salvador, Ecuador, and Belize are among the market-access countries most at risk of sovereign stress, according to the model presented below.Unsurprisingly, several advanced economies appear least at risk, including Norway, Ireland, Denmark, Singapore, the Netherlands, Luxembourg, Hong Kong, and Switzerland.

Earlier this year I published the high-level initial results of a sovereign debt stress tracker, based on a model developed by the International Monetary Fund for countries that it classifies as having access to international markets. The IMF presented this model as part of its update to its Debt Sustainability Framework for Market-Access Countries in 2021, claiming at the time that it had performed significant robustness checks to ensure forecast salience. Time will tell how useful this tool is in predicting sovereign debt strains, and, in any case, it should only be used in conjunction with other analytical approaches.

Heatmaps

Using the latest available data for 2023, the heatmaps below rank order countries by the probability of experiencing sovereign stress, as represented by the column farthest to the right. Neither the probabilities for the dependent variable nor any of the raw data readings for any of the independent variables is shown below. Instead, readers can see the percentile rank compared to the maximum value in each variable column, which is beneficial for visually detecting relative heat for each indicator.

Lighter colors represent more risk, while darker colors represent less risk. Independent variables with negative coefficients, i.e. are negative predictors of sovereign stress, have been reversed in order to ensure color scheme coherence. These include institutional quality, the current account, and international reserves.

The first heatmap below suggests that Angola, Pakistan, Egypt, Jordan, Argentina, El Salvador, Ecuador, and Belize are most at risk of experiencing sovereign debt strains. Looking across the independent variables for this group of countries:

They generally suffer from high external public debt burdens and from relatively poor institutional quality, though Argentina and Jordan fare better on those measures, respectively.

El Salvador is penalized relatively less on stress history, though this assumes spread widening in recent years remained under the IMF’s stress definition threshold (see “Model” section below).

One-year changes in general government debt in Angola, Egypt, and Argentina point to potential risks.

El Salvador, Jordan, and, to a lesser extent, Pakistan, appear to need some replenishing of their international reserve buffers.

Angola and – to a lesser extent – Argentina are marked down for surging REERs.

Pakistan and Egypt display relatively concerning public debt/revenue ratios.

Jordan stands out for poor current account performance.

Egypt, Jordan, and Ecuador exhibit high credit-to-GDP gaps, though several other countries fare worse on this measure.

Each value is divided by the maximal value in that column, resulting in its own empirical percentile. Each value shown is the percent of observations with that value or below it. Sources: IMF, WGI, WB, Bruegel, BIS, author’s calculations.

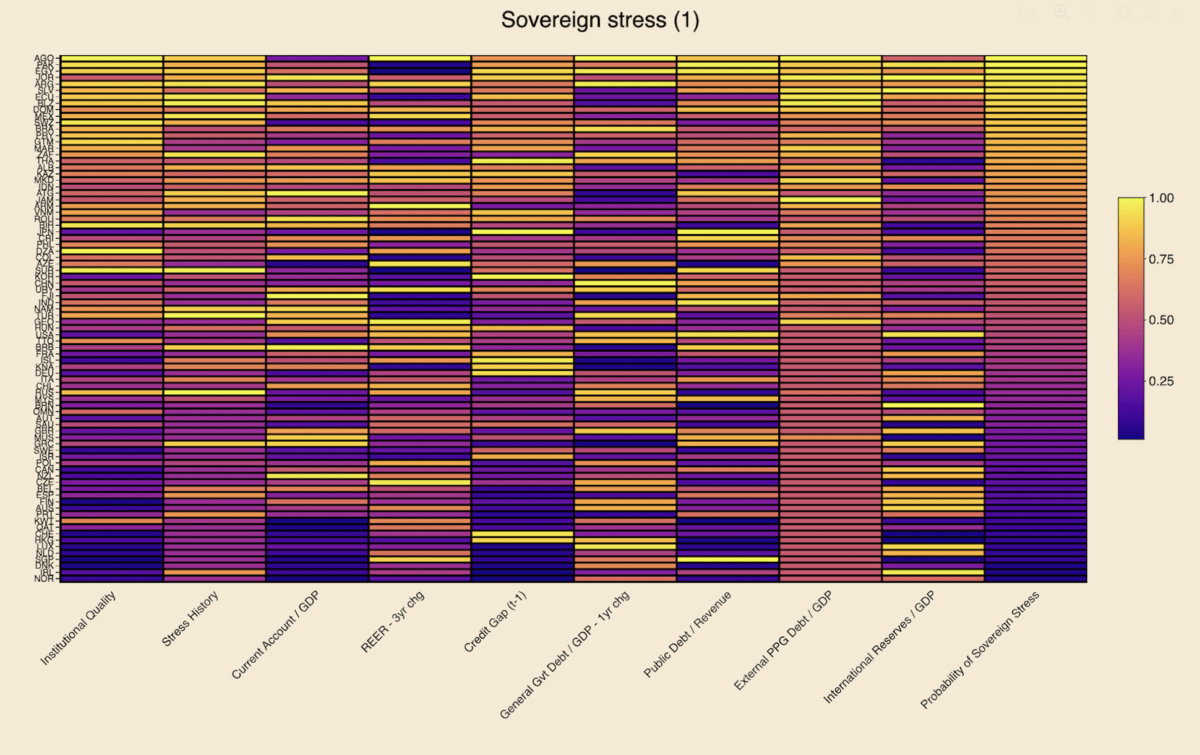

The second heatmap uses foreign currency general government debt to replace the external PPG debt indicator featured in the first heatmap (see explanation in “Data” section below). Neither of these indicators is ideal, as in both cases coverage for many countries is either lacking or data points are equal to zero. This is obvious in both heatmaps from the absence of dark-colored cells in the relevant column, meaning that many countries are zero. Overall country coverage on this variable is better in the first heatmap, but the second one provides value for countries where data is missing in the first one (e.g. Israel, Korea, Sweden).

The eight countries most at risk of sovereign stress in this second heatmap are the same as in the first one, albeit in a slightly different order and except for Mexico replacing Belize. On this latter point, FX general government debt data – sourced from the BIS (see “Data” section below) – is missing for Belize, conferring on it an unfair advantage over Mexico and other countries where data are present for this indicator. In the first heatmap, external debt data is present for both Mexico and Belize, with the latter appearing more at risk than the former.

Each value is divided by the maximal value in that column, resulting in its own empirical percentile. Each value shown is the percent of observations with that value or below it. Sources: IMF, WGI, WB, Bruegel, BIS, author’s calculations.

Interpretation

Focusing on a country case helps illustrate ways to interpret the data in this model. Take Angola, as it appears most at-risk. Using heatmap (1), the brightest and thus most concerning data points are in the institutional quality, REER 3-year change, general government debt 1-year change, and external public and publicly-guaranteed debt columns. This suggests that the government and public sector more broadly are borrowing heavily, while prices and the exchange rate have also combined to rise quickly. Moreover, the institutions to set a good policy framework appear to be lacking. This is already a dangerous mix.

On the other hand, Angola scores well on its current account balance and international reserves variables. This is easily explained by the fact that the country is an oil exporter, thereby keeping its current account balance high and accumulating foreign reserves from the proceeds of these oil sales to buyers abroad.

While these oil exports provide Luanda with ample benefits, heavy reliance on a commodity-based export sector is also a double-edged sword. The result is often an appreciation of the exchange rate, making the economy less competitive for developing other industries: a classic case of Dutch Disease.

More concerning still is the presence of high inflation. The country’s surging REER variable already suggests that prices are probably rising, as the overall increase is unlikely to be due to nominal exchange rate dynamics alone. Increases in government debt suggest potential fiscal profligacy, which can lead to undesirably-high inflation, the presence of which is confirmed by a glance at recent Angolan statistics. The credit-to-GDP gap, which measures the deviation from trend of credit to the non-financial private sector as a share of GDP, is not particularly alarming in Angola, but may be high enough to also be contributing to the rising price level.

Angola also exhibits a high public debt-to-revenue ratio, which is worrying, given all the oil revenues that the country is seemingly raking in, suggesting that less borrowing and more fiscal discipline are likely needed. Recent sovereign stress is also a concern, indicating that, for all its natural resources, the government is unable or unwilling to pursue policies required to maintain macroeconomic stability.

Model

To recap, the model’s dependent variable is the probability of sovereign stress, which the IMF has detailed criteria for defining – running the gamut from outright default to a mere spread widening beyond a certain threshold. Regarding the independent variables:

The first two represent how recently a country has experienced sovereign stress, and its government effectiveness and regulatory quality.

Other explanatory variables are macroeconomic in nature, including current account balances, real effective exchange rates – which also capture price changes, credit gaps to the private sector, and international reserves.

More specifically fiscal indicators include those on general government debt, foreign currency public debt, and public debt-to-revenue ratios.

With the exception of REERs and debt-to-revenue, these macro-fiscal indicators are all expressed as a share of GDP.

A global variable also features in the model, the VIX Index, which measures stock market volatility in the US, but is not presented in the heatmaps above, given its constance across countries.

Data

In the first iteration of the tracker, 2023 data was captured for 43 market-access countries, including both emerging markets-developing economies and advanced economies. Thanks to more available data for this year and refinements in data capture, coverage has been expanded to 82 MACs in these heatmaps.

Two similar heatmaps are presented in this article, with a difference in one of the independent variables and, as a result, slight changes to the overall results in the dependent variable. One of the IMF’s indicators is foreign currency public debt. In the first instance, the World Bank indicator for external public and publicly-guaranteed debt is used as the best available proxy for the IMF’s variable. While using this data from the World Bank remains the best possible option at this stage, there are some glaring omissions in coverage. For instance, the World Bank source suggests that Israel’s external PPG debt is equal to zero, which is clearly incorrect.

As a remedy to the World Bank’s data deficiencies, a second heatmap applies data from the Bank of International Settlements on foreign currency general government debt, as a proxy for this indicator in the same overall model. The BIS data does fill in some of the World Bank gaps – e.g. Israel – but in fact covers fewer countries than the first source. As such, the first heatmap is still preferable.

It is also worth noting that both the World Bank and BIS indicators differ from the IMF variable of foreign currency public debt. In the former case, external public debt differs somewhat from foreign currency public debt, even if virtually all external debt is in foreign currency. In the latter case, foreign currency general government debt excludes some types of debt that is covered under foreign currency public debt.

The World Bank Group-International Monetary Fund Annual Meetings drew to a close in Marrakech this past weekend, the first time these events have been held in Africa since the 1973 edition in Nairobi. While the Bank-Fund leadership expressed their usual endorsement of international cooperation and optimism for the future, this year’s agenda also explicitly aimed to address geopolitical fragmentation and fully acknowledged heightened threats to the goals of eradicating poverty; bolstering sustainable, inclusive growth; and preserving macroeconomic stability.

The main problem at this year’s annuals wasn’t a new one and goes by many names: geopolitical competition, fragmentation, deglobalization, trade frictions, or decoupling. A whole host of challenges to multilateral financing efforts stem from the political obstacles to international cooperation that have emerged over the past decade, with the 2007-2009 Global Financial Crisis marking the end of America’s “unipolar moment” and ushering in a new, more competitive era. The prospects for a new capital increase for multilateral development banks, innovative hybrid financing solutions to boost World Bank lending, and sovereign debt restructuring processes are all suffering from the fractured backdrop.

IMF Global Policy Agenda

The IMF’s policy priorities are a response to the main macroeconomic challenges in today’s global economy:

tame inflation

ensure financial stability

restore fiscal room

boost medium-term growth

Indeed, inflation has not yet reverted to central bank targets in many countries, while the rapid rise in interest rates in the past few years have strained parts of the US banking system. At the same time, expansionary fiscal policies have pushed up yields on government debt in various countries, with the return of bond vigilantes evident in the US in 2023. The prospect of higher fiscal deficits can also sometimes undermine financial stability, as exemplified by the UK mini-budget straining pension schemes in September 2022. Tighter fiscal policy will be necessary in many countries to guard against future shocks, while appropriate reforms are also widely-needed to revive the dimmed outlook of medium-term growth.

In parallel with the macroeconomic policy priorities, the Fund is pursuing complementary objectives. The IMF launched, with the government of Morocco, the Marrakech Principles for Global Cooperation, which include reinvigorating inclusive and sustainable growth; building resilience; supporting transformational reforms; and strengthening and modernizing global cooperation. These principles are a welcome attempt to stem the tide of global divergences, even if they are unlikely to meet with much success in the short term. In a similar vein, the IMF has attracted more funding for the interest-free Poverty Reduction and Growth Trust and for the climate change-focused Resilience and Sustainability Trust.

Of note, the IMFC Chair committed to concluding the 16th General Review of quotas by December 2023, in light of agreement on a significant increase of quotas this year. Crucially, there seems to be support for quota realignment by June 2025 to reflect current economic realities, including through an updated quota formula. The IMFC has also called for the creation of a third chair on the IMF Executive Board for Sub-Saharan Africa, in order to improve the continent’s representation.

Yet the IMF has not been able to deliver more in the way of impactful policy successes. One potentially high-impact policy area would be finding a solution for re-allocating SDR usage from the wealthy countries that don’t need them to the poorer countries that do. A further work-stream with outsized effects would be to do more to strengthen the Global Financial Safety Net, which includes the IMF’s toolkit, bilateral swap arrangements, regional financial arrangements, and international reserves – a tall order in the current environment.

Global Sovereign Debt Roundtable

The official sector has achieved a modicum of progress on improving the sovereign debt restructuring architecture in recent months. Probably of most importance to private creditors is improved information-sharing during restructurings, with new possibilities for private lenders to access debt sustainability analyses and related elements at the same time as official creditors, under certain conditions. The Fund has highlighted the increasing speed from staff-level approval to Board approval, from 11 months in Chad in 2022, to 9 in Zambia, 6 in Sri Lanka, and 5 in Ghana most recently, while recognizing that this is still above the 2-3 month average in the past.

The IMF maintains that external public debt strains are not currently as high as they were in the 1990s, even considering the existence of larger local debt markets, which has led to some observers wondering if there is a sense of complacency about pending risks in low-income countries. The IMFC welcomed progress in Zambia, Sri Lanka, and Suriname but called for more results in Ghana, Ethiopia, and Malawi, while also calling for stronger creditor coordination for sovereign debt restructurings occurring outside the Common Framework.

One of the main pieces of news to come out of the meetings was that Zambia’s finance ministry and its official creditor committee signed a memorandum of understanding, thus formalizing the agreement reached in June, and paving the way for Zambia to seek comparable treatment from its commercial creditors. It was also revealed that Kenya may be seeking exceptional access to IMF support ahead of a $2 billion bond maturing in June 2024.

There are some other minor new features in the sovereign restructuring framework, regarding cutoff dates (no later than staff-level agreement), state-contingent debt instruments (which shouldn’t be the norm), and the appropriate approaches to domestic debt (case-by-case) and SOE debt. Other areas remain contentious among the various creditor categories, such as appropriate discount rates to be used for NPV calculations for comparability of treatment. There is also no consensus on the treatment of arrears and on debt service suspensions during negotiations.

Show me the money: capital increases for MDBs?

Despite the ongoing efforts of senior staff to convince donor countries to provide more resources for development, the World Bank Group’s ambitions will continue to lack requisite firepower. The cause is an absence of political will in most of the G7 countries to make sufficient financial commitments to development, as evidenced by a succession of broken Western promises. To be sure, some efforts are under way, such as Japan’s pledge to significantly raise its contribution to the IMF’s zero-interest loan tool, the Poverty Reduction and Growth Trust. For its part, the US may transfer $2 billion in additional funding to the World Bank Group this year, though this is a far cry from the scale that is needed.

Additional annual financing required to meet the United Nations’ Sustainable Development Goals stands at around $3 trillion. The G20’s Capital Adequacy Review framework suggests that a general capital increase for the multilateral bank system, including the IBRD, could unlock $200 billion in annual lending, with a further $80 billion annually from balance sheet optimization (e.g. callable and hybrid capital). The Center of Global Development suggests that the international development finance system should boost its annual financing by $500 billion by 2030, with multilateral development banks providing $260 billion and national development finance institutions delivering the remainder. Private capital ought to match that half-trillion increase, for a combined public-private total of $1 trillion.

Yet these figures still fall well short of the additional $3 trillion needed annually. By the CGD’s calculations, each dollar of new equity in MDBs can be leveraged for $15 of external sustainable investment financing, of which $7 in direct MDB lending and $8 in private capital. Assuming that private finance can be crowded in to such a degree is likely overly optimistic, as the CGD’s own figures indicate that MDBs currently mobilize only 60 cents for each dollar lent. Even so, public and private stakeholders will have to come up with financing solutions to achieve the SDGs, and this should be possible with enough political will: just look at the over $100 billion raised for Ukraine.

The World Bank’s Evolution Roadmap

The World Bank Group’s recently-appointed president, Ajay Banga, has laid out a roadmap to enhance the organization’s effectiveness. More efficient balance sheet management should unleash $157 billion in additional lending over 10 years, while preserving the Bank’s AAA rating. These measures include increasing the loan to equity ratio, launching a hybrid capital instrument, and creating a portfolio guarantee mechanism. Similarly, management is also exploring solutions using callable capital and SDRs. An elegant approach to channeling some of 2021’s SDR 650 billion windfall could be to have the Bank issue SDR bonds, to be purchased by national central banks.

A number of other changes are in the works under Banga. These include setting up a Global Public Goods Fund to grow concessional resources by attracting funding from governments and philanthropies, exploring maturities of up to 40 years for social and human capital investments, and exploring energy transition solutions. More importantly, efficiency gains are at the heart of the new strategy. There is an objective to slash project review and approval times by a third by simplifying procedures, while partnerships with other MDBs are already being pursued more actively so as to amplify impact. Similarly, Banga’s team plans on scaling knowledge-sharing in order to more easily share impactful solutions, and a private sector investment lab has already been set up to galvanize private financing.

Banga’s plans to streamline processes seem like a requisite pre-condition for convincing donor countries to increase the Bank’s share capital, though even if his team can deliver, any new equity is far from guaranteed. Early signs of the new president’s first few months in the role have demonstrated his dynamism and communication skills, and future success in reforming the institution’s bureaucracy, while likely challenging to achieve, could yield significant development benefits. However, his team is reportedly difficult to approach internally, which could potentially delay progress.

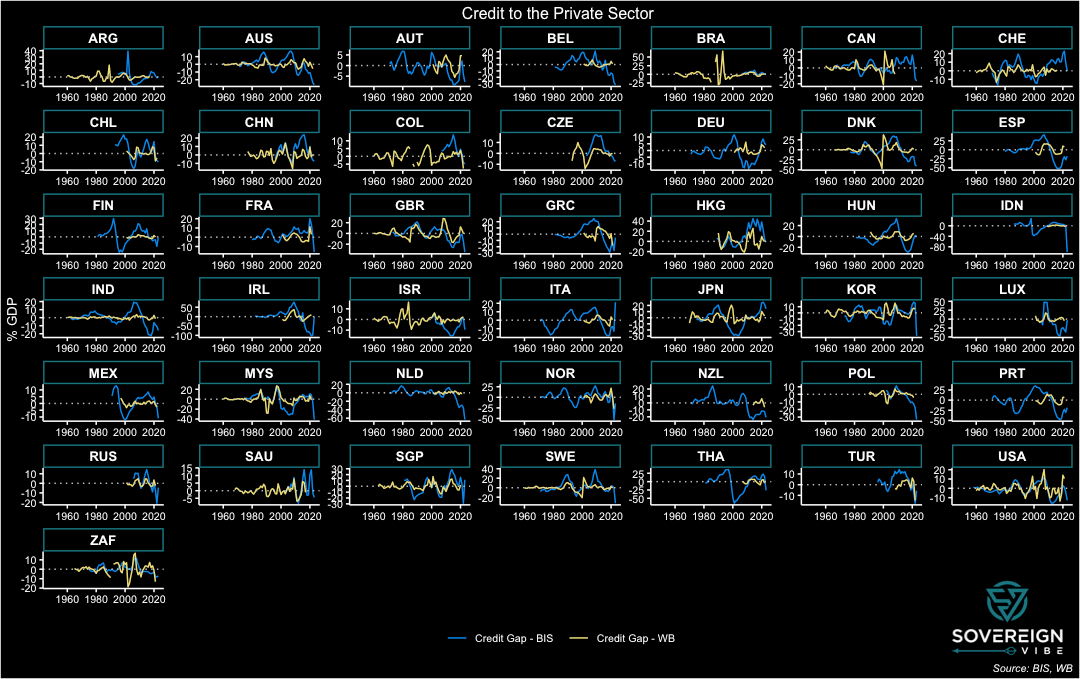

As part of tracking the probability of credit stress among 112 sovereign issuers, one of the variables of interest in the IMF’s model is the credit-to-GDP gap. This indicator matters not only because of its predictive power for sovereign credit events but for many other reasons as well, including monetary policy transmission and government borrowing. When analyzed in conjunction with other data, credit gaps are useful barometers for detecting the presence of credit bubbles, economic over- or under-heating, and policy distortions such as financial repression and fiscal dominance.

Credit gaps are derived from observations of credit extended to the private sector as a percentage of GDP, and then a statistical technique, usually Hodrick-Prescott filtering, is used to smooth out the data points in the time series as a way to measure an underlying trend. While there are some shortcomings to this approach, including the arbitrary nature of the smoothing parameters used to identify the trend, it helps ascertain whether the cyclical component of lending is above or below long-term expected processes.

A credit-to-GDP gap is thus an actual observation at time t minus the trend in the same time period. As such, a positive credit gap is one in which lending is above trend, whereas a negative one is below. The credit gap coefficient in the IMF model is positive, as is the case in other models in the financial crisis academic literature, meaning that higher values are associated with an increased likelihood of sovereign debt strains. Looking at quarterly data through end-202212023 data will be presented in future posts on credit gaps. from the Bank of International Settlements on 43 countries plus the Euro Area, this first set of charts presents the actual credit-to-GDP ratios in blue, the smoothed trend in yellow, and the credit-to-GDP gaps in green.

SLIDE DOWN: actual data vs trend; SLIDE UP: the cyclical gap between the two; XM = Euro Area

In the chart above, credit gaps in this mix of developed (DMs) and major emerging market economies (EMs) are currently mostly negative. This makes sense given the tighter monetary policy stances around the world to combat inflation, with EM central banks having begun their rate-raising cycles2Some EM central banks are so far ahead of DM that they have already begun cutting rates in 2023. before their DM peers. A spike in credit gaps can also be observed in 2020 as policymakers worldwide lowered interest rates and facilitated the extension of credit as part of emergency measures to mitigate economic scarring at the height of the pandemic.

The BIS credit gap data is extremely useful for this set of countries, which, after all, comprise the world’s largest economies, and all the more so because it is available on a quarterly basis. The BIS describes its credit-to-GDP ratio as capturing total borrowing from all domestic and foreign sources by the private non-financial sector.3https://www.bis.org/statistics/about_credit_stats.htm However, other sources are needed for measuring credit to the private sector in other countries, and, thankfully, the World Bank has a similar indicator: domestic credit to the private sector by banks.4 https://databank.worldbank.org/metadataglossary/jobs/series/FS.AST.PRVT.GD.ZS The World Bank data series has far broader country coverage than the BIS data, thus opening vast additional swathes of the world to analytical coverage.

In contrast to the BIS data with its inclusion of both domestic and foreign credit to the non-financial private sector, the World Bank indicator appears to only include domestic sources of financing. Moreover, the BIS data appears to include sources of non-bank financing, unlike the World Bank data. Taken together, these two differences likely explain much of the discrepancy between these two datasets. Further, the World Bank data appears to only be available at a yearly frequency, thus requiring the BIS quarterly data to be transformed to yearly averages for the purposes of comparison.

The charts below present BIS data in blue and World Bank data in yellow, in yearly form through end-2022 in both cases. As seen above, the BIS provides credit gap and trend data alongside its credit ratios and uses a one-sided Hodrick-Prescott filter with the smoothing parameter λ set to 400,000 for this quarterly data. The World Bank only provides its credit ratios on a standalone basis, meaning that the trend and credit gap need to be estimated independently. This is simple enough for one country, and thankfully panel statistical techniques enable scalability for quick estimation across a large number of countries and years. As such, trends and credit gaps are derived from the World Bank’s credit ratios using a two-sided HP filter with λ = 100, the recommended setting for annual data.

SLIDE DOWN: actual data; SLIDE UP: trend data, smoothed with HP filters

Consistent with the inclusion of foreign sources of credit, the BIS credit ratios are usually higher than those from the World Bank, especially in many European countries, e.g. Luxembourg and Belgium. Elsewhere, the figures track more closely, as is the case with Japan, Malaysia, and the UK. The US and China also fell into this category, but the datasets have diverged in recent decades for those countries. Surprisingly, there are also a few countries where the World Bank ratio exceeds the BIS reading, despite the former excluding foreign credit sources, with South Africa and the US standing out most prominently from this perspective.

The point of comparing the two datasets is to use the BIS as a benchmark to get a sense if the World Bank data is at least somewhat aligned with the former and it is any good for predictive purposes. Certainly, the similar characteristics of the actual and trend data above are a positive sign. As for the credit gaps themselves, the BIS and World Bank figures are presented below. While there are large differences in most countries, there are also similar processes at work in many countries, e.g. the United Kingdom, Malaysia. The BIS credit gaps appear to be more volatile than those of the World Bank, which could be explained by the former’s inclusion of foreign lending: capital flows of the portfolio variety, which includes debt, are prone to sudden stops and starts.

To simplify further, the difference in the BIS and World Bank credit gaps, where the former is subtracted from the latter (difference = WB – BIS), features in the chart above. Ideally, the data readings would all be horizontal lines at zero or at least resemble a stationary process hovering above and below zero. While some countries do have these features – Sweden, the UK, the US, and Switzerland, among others, a large cohort exhibits some sort of bias. A statistical test of this difference in credit gaps across this panel of countries over these years would likely reject the notion that the difference is equal to zero. Nevertheless, the World Bank domestic credit to private sector by banks indicator seems fit for purpose, particularly given the large role that domestic banks play in credit provision in most economies.

Future posts will expand further on the importance of credit gaps and present broad country coverage of World Bank credit gap data.

1

2023 data will be presented in future posts on credit gaps.

2

Some EM central banks are so far ahead of DM that they have already begun cutting rates in 2023.

I spent most of 2012 working in Gabon, a gem of a country well-endowed with some of the lushest rainforest on the planet, abundant natural resources – oil, manganese, wood – and a small population. Like many observers, I was aware of the concerns leading up to the August 2023 presidential elections as President Ali Bongo sought a third consecutive term, especially given the post-electoral violence in 2016.

Yet the military coup of August 30th still comes as a surprise because, in recent years, the military takeovers in Africa had largely been confined to the Sahel region: Niger, Mali, Burkina Faso, Chad, and Sudan. There were two other recent putsches, one in Guinea, on the Sahel’s doorstep, and another one in Zimbabwe.

These countries have much lower income/capita and larger populations. Unlike Gabon, most of them are landlocked and have arid climates.1Guinea is neither landlocked, nor does it have an arid climate. Zimbabwe is also not as arid as the Sahel. So what do these countries have in common with Gabon? Plenty, whether their colonial pasts under France2With the exceptions of Sudan and Zimbabwe. or the nitroglycerin-like combination of weak institutions and ethnic divisions.

Country

Coup d’Etat(s) date

GNI per capita – USD

Population – mn

🇬🇦 Gabon

August 2023

7,540

2.6

🇳🇪 Niger

July 2023

610

25.3

🇹🇩 Chad

October 2022 & April 2021

690

17.2

🇧🇫 Burkina Faso

September & January 2022

840

22.1

🇸🇩 Sudan

October 2021 & April 2019

760

45.7

🇬🇳 Guinea

September 2021

1,180

13.5

🇲🇱 Mali

August 2020

850

21.9

🇿🇼 Zimbabwe

November 2017

1,500

16.0

Sources: World Bank, author’s research

My analytical fallacy was to think about the coups in the Sahel as some sort of wave with common drivers, which would have a bearing in other parts of Africa and beyond. Not so, or at least not beyond the Sahel where several weak, poor states having trouble coping with terrorist insurgents is a commonality. Rather than a wave of African coups with a shared set of narrowly-defined underlying causes, a version of the Anna Karenina principle applies: “Each unhappy country is unhappy in its own way.”

Moreover, it is good discipline to keep ethnicity front of mind when analyzing African politics, as this helps reveal some of the political forces at play that make each country unique. Even though ethnic factors are often of secondary importance, as in the case of Gabon, considering ethno-linguistic and cultural differences also provides contextual granularity that is often absent from English-language coverage of francophone Africa.

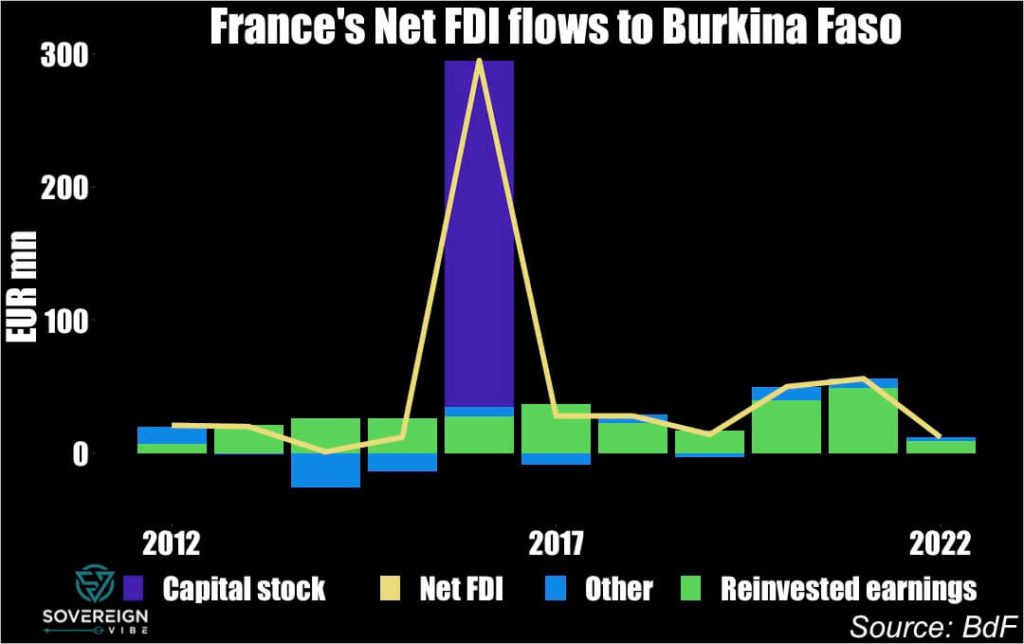

Below, I also provide charts on France’s net FDI to each of the francophone countries as a simple gauge of its ongoing involvement in each economy. This simple measure does not explain the coups in each country, nor does it encompass the complexity of the bilateral economic, political, and security relationships, but it provides relevant context as observers ponder Paris’s links to the continent.

🇬🇦 Gabon

August 2023: The military overthrows Ali Bongo, who hails from the small Téké ethnicity (~<10% of the population) in the remote Haut-Ogooué region, minutes after his electoral win is announced. The takeover appears to have elements of both popular dissatisfaction and of a palace coup. The leader of the junta, Brice Clotaire Oligui Nguema, was head of the Republican Guard’s special services unit. Also a Haut-Ogooué native, Nguema had long served under the previous president, Omar Bongo, before being sidelined for several years after Ali came into office.

Omar Bongo had long relied on French support, while his son Ali had made some concessions to the larger Fang ethnicity (33% of the population) and others at various points during his terms.

In Africa, only the Seychelles and Mauritius have higher GNI/capita than Gabon, where 1/3 of the population lives below the poverty line.

Clearly, any wealth redistribution from the rapacious Bongo clan was insufficient for the population to allow him to continue pilfering the country indefinitely amid suspicions of electoral fraud in the current and previous elections.

Enfeebled by a stroke in October 2018, Ali Bongo – and his reportedly dissolute family members – provided a complacent atmosphere at the presidential palace, thus combining with popular discontent to set the ideal conditions for Nguema and his co-conspirators.

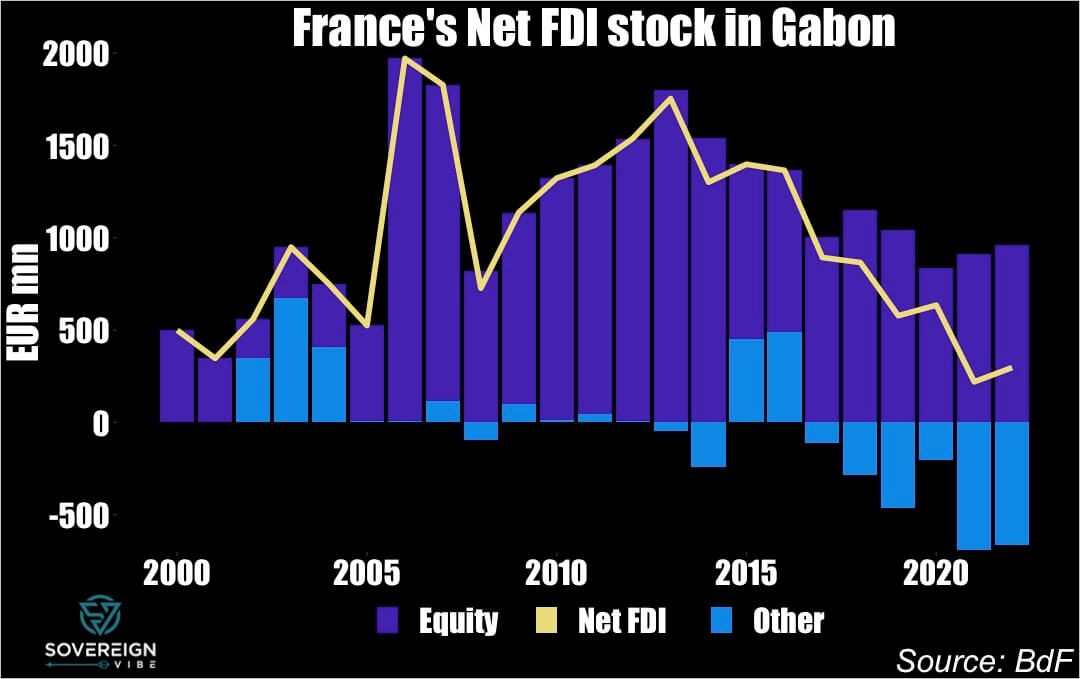

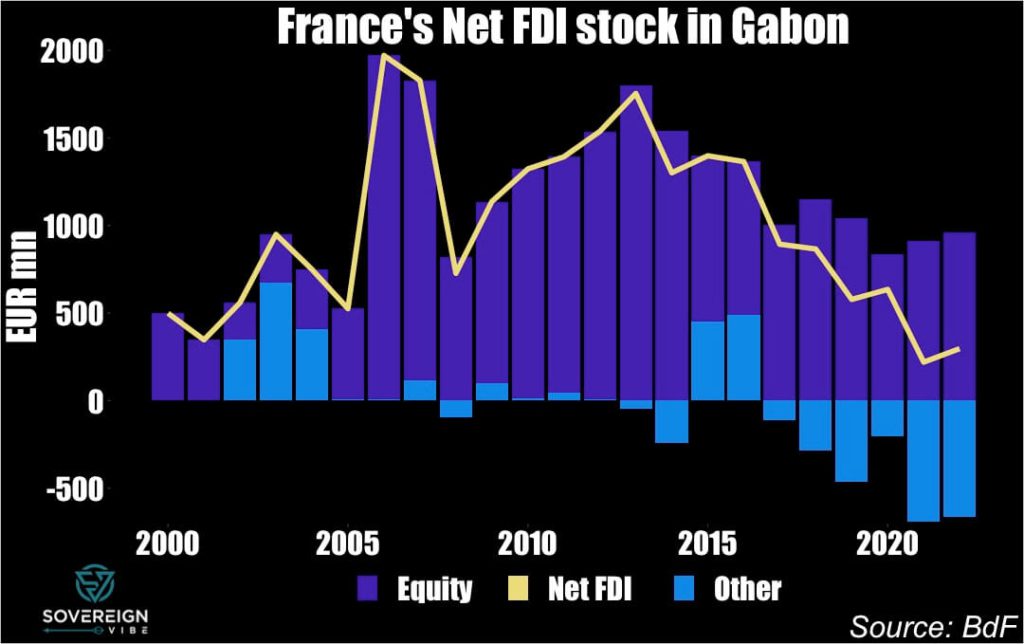

Of note, France’s net foreign direct investment stock in Gabon has been on a downward trend since the mid-2010s (see charts below), declining from around €1.8bn in 2013 to under €500mn in 2022. This is despite the global net FDI stock in Gabon rising over the same period, pointing to France’s diminished stature in the Gabonese economy. More detailed information on this topic will be available in future posts.

🇳🇪 Niger

July 2023: Junta leaders oust President Mohamed Bazoum, who is of Arab ethnicity ( < 0.5% of the population), purportedly for leniency towards islamist insurgents. This underscores the political importance of the security situation, as in several other countries throughout the Sahel.

Bazoum succeeded Mahamadou Issoufou (Hausa, 55% of the population), who completed two terms as president without trying to run for a third term, instead nominating Bazoum as his preferred successor.

Issoufou had himself come to power through elections a few years after a military coup ousted a previous president – Mamadou Tandja – who had attempted to stay on as president for longer than two terms, much like Ali Bongo in Gabon today.

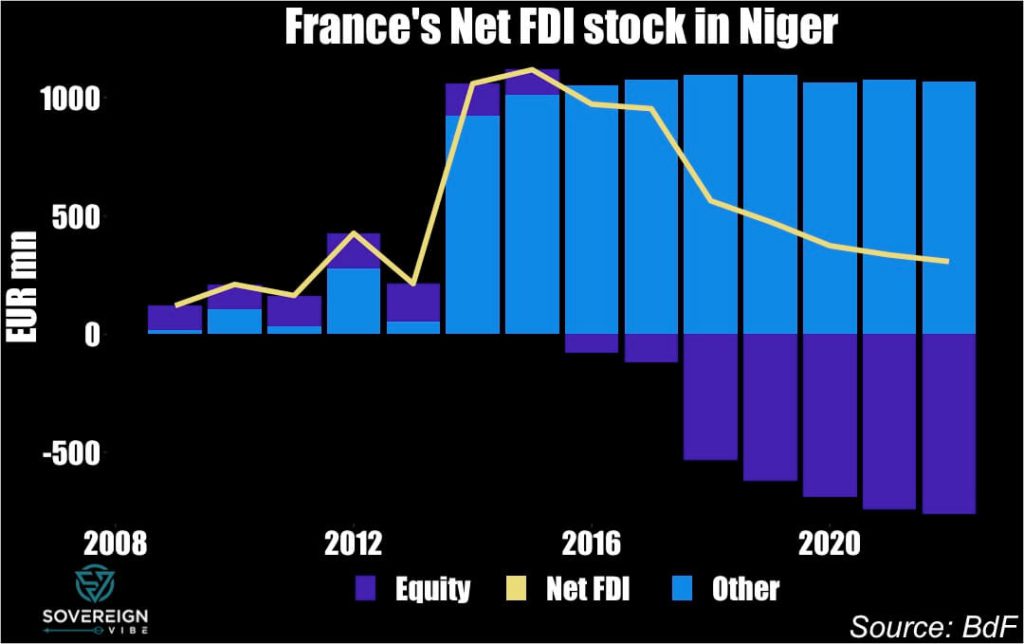

As in Gabon, France’s net FDI stock in Niger has been on the wane since the mid-2010s, declining from over €1bn to under €500mn as of last year. The entirety of French exposure to the country appears to in the form of debt and other instruments, including in all likelihood intra-company debt.

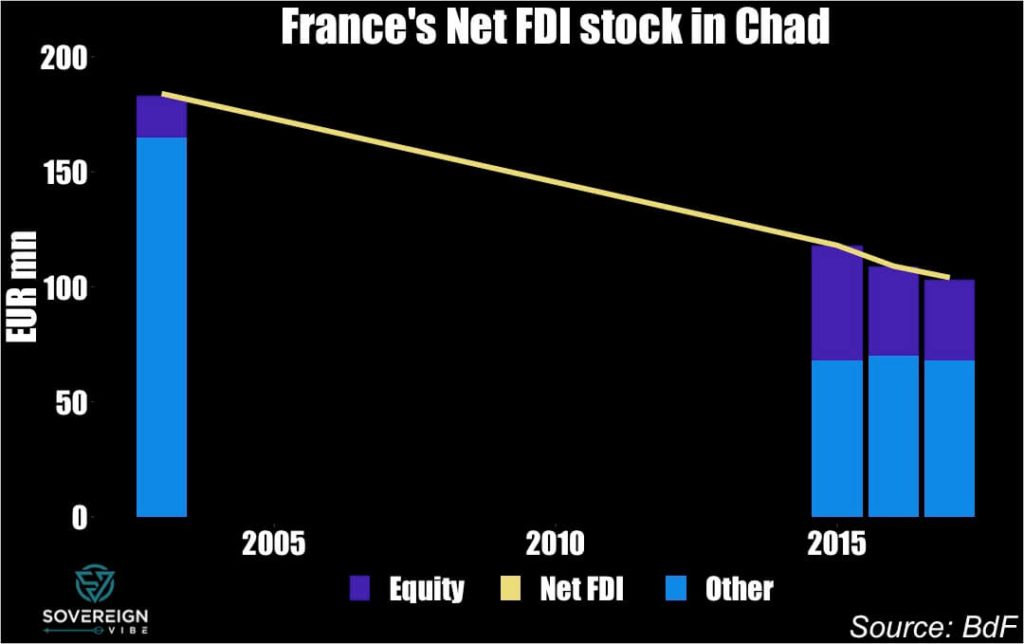

🇹🇩 Chad

April 2021 – October 2022: Long-serving President Idriss Déby (Zaghawa, ~1%) had taken power via a French-supported coup in 1990 against then-president Hissène Habré (Gorane, aka Daza or Toubou, ~4-5%) and was fatally wounded in April 2021 during hostilities with insurgents, mainly of Gorane extraction.

Déby’s son Mahamat Idriss Déby (half Zaghawa, half Gorane, married to a Gorane, father of nine children) seized control of the country at the head of a military junta immediately after his father’s death with a commitment to an 18-month transition period to culminate in elections, which he postponed by two years in October 2022.

Despite limited French net FDI exposure to Chad, even here France’s presence is declining, from nearly €200mn in the early 2000s to around €100mn today.

🇧🇫 Burkina Faso

September 2022: Captain Ibrahim Traoré (b. 1988) overthrew Lieutenant-colonel Paul-Henri Sandaogo Damiba for not having followed through on the promises of the January 2022 coup and following several deadly terrorist attacks, notably in Gaskindé, where jihadists ambushed a provisioning convoy, resulting in at least 11 deaths.

Mutineering soldiers ousted President Roch Marc Christian Kaboré (Mossi, ~56%) in January 2022 following a crushing defeat of burkinabè armed forces by jihadists in November 2021, amid widespread disappointment at the government’s management of the conflict and failure to provide rations to troops. Lieutenant-colonel Paul-Henri Sandaogo Damiba succeeded Kaboré as transitional president.

In October 2014, a popular uprising ousted then-president Blaise Compaoré’s (Mossi, ~56%) upon his attempt to change the constitution and thereby allow himself to stand for a fifth term after 27 years in power. After a year of transition, Kaboré was elected president in November 2015.

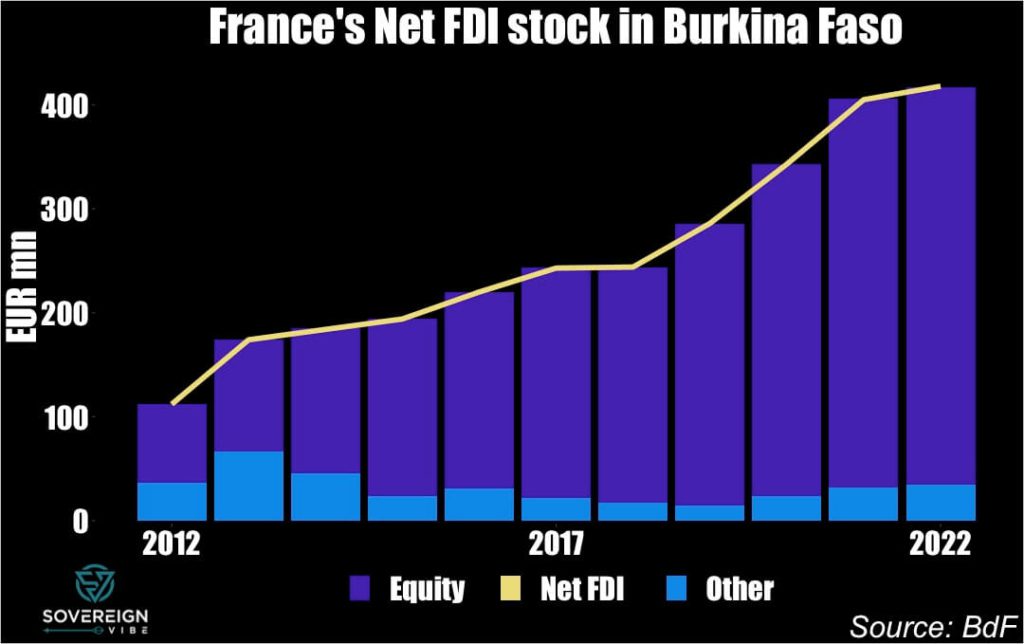

In constrast to Gabon, Niger, and Chad, France’s net FDI stock in Burkina Faso has been rising steadily for the past decade, driven mainly by reinvested earnings into increasing shareholder equity. Overall exposure has jumped from ~€100mn in 2012 to ~€400mn in 2022.

🇸🇩 Sudan

April 2019 & October 2021: General Abdel Fattah al-Burhan seized power in 2021, placing Prime Minister Abdalla Hamdok under house arrest. The Sudanese Armed Forces ousted the long-reigning Omar al-Bashir in 2019 under the leadership of Ahmad Awad Ibn Auf.

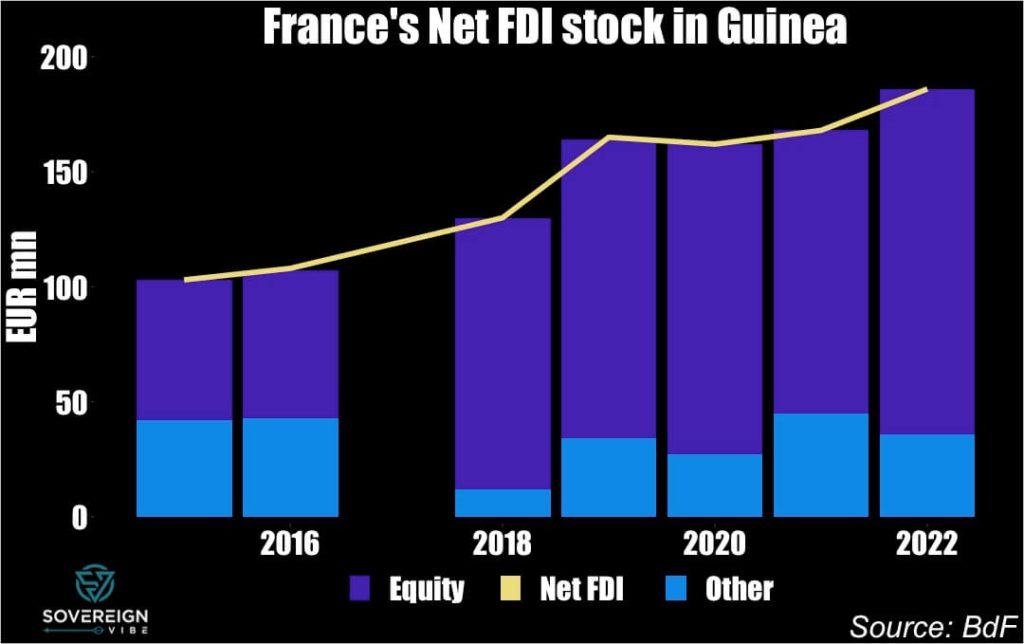

🇬🇳 Guinea

September 2021: Amid widespread popular dissatisfaction with the government, military putschists arrested President Alpha Condé (Mandingo aka Malinké, 23%, second-largest group) as special forces commander Mamady Doumbouya dissolved the government and seized power as interim president. Of these recent coups, the Guinean case most closely resembles the current situation in Gabon.

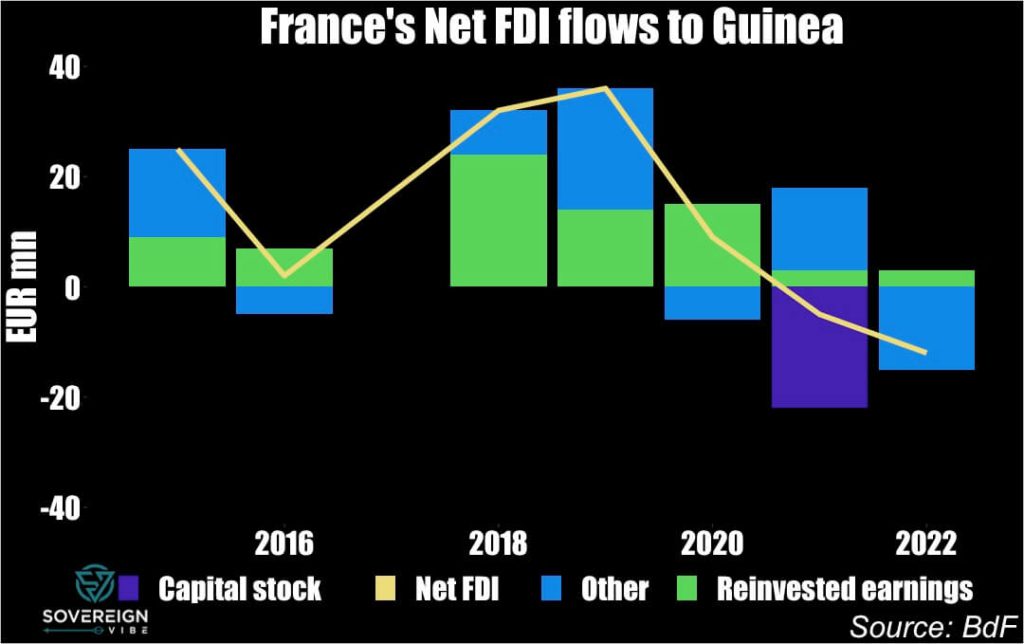

France’s net FDI exposure to Guinea has been rising steadily since the mid-2010s, albeit from a low base, partly reflecting Conakry’s historically relatively cool relations with Paris. Up from €100mn in 2015, French FDI stock stood at ~€175mn in 2022.

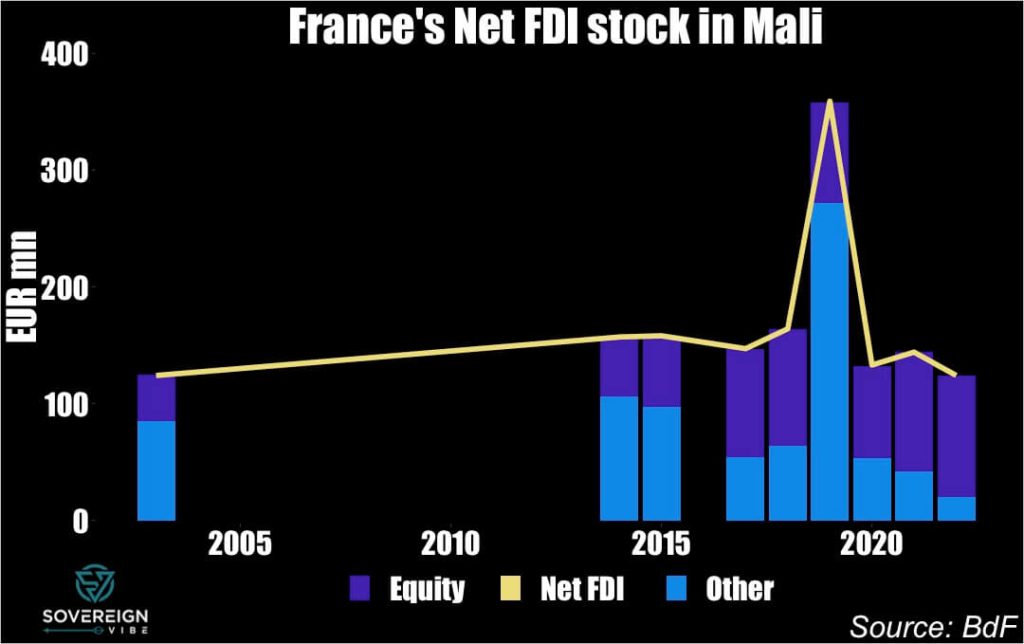

🇲🇱 Mali

August 2020: A colonel in Mali’s special forces, Assimi Goïta (Minianka, ~7%, b. 1983) has been the country’s de facto leader since a successful coup ousting IBK in August 2020.

Ibrahim Boubacar Keïta (Mandingo, aka Malinké or Maninka, ~8%, d. 2022) is elected president in 2013 after the elections were delayed by a year, following the military putsch of 2012 and the ongoing war against islamist insurgents. He rejected the coup but agreed to negotiate with the junta, which adopted a neutral position towards him. In 2020, after months of political crisis stemming from economic pressures, the Peul/Fula-Dogon ethnic conflict, and the pandemic, a coup removed IBK from power.

Amadou Toumani Touré (Bambara, ~25%, largest group, d. 2020) was president from 2002-2012 after having been elected democratically and later ousted via military coup two months before the 2012 elections, in which he was not running. The coup was to denounce the management of the conflict in northern Mali between the army and the Touareg rebellion at the time. He had himself participated in a coup d’Etat in 1991 against the then-long-standing president Moussa Traoré (Malinké, ~8%, d. 2020).

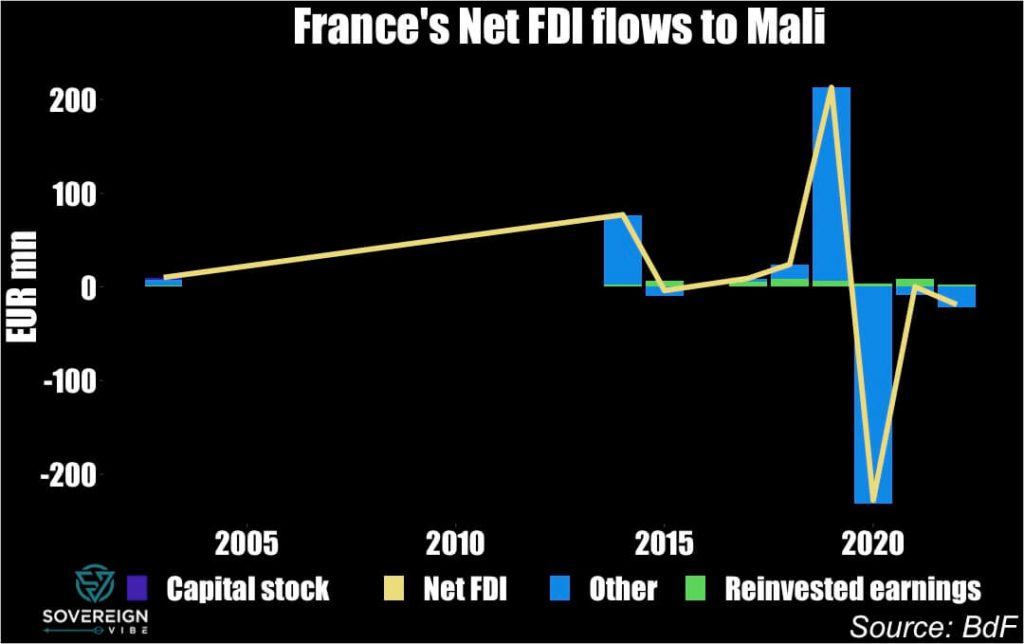

France’s FDI exposure to Mali has essentially moved sideways over the past 20 years, standing at around only €100mn.

1

Guinea is neither landlocked, nor does it have an arid climate. Zimbabwe is also not as arid as the Sahel.

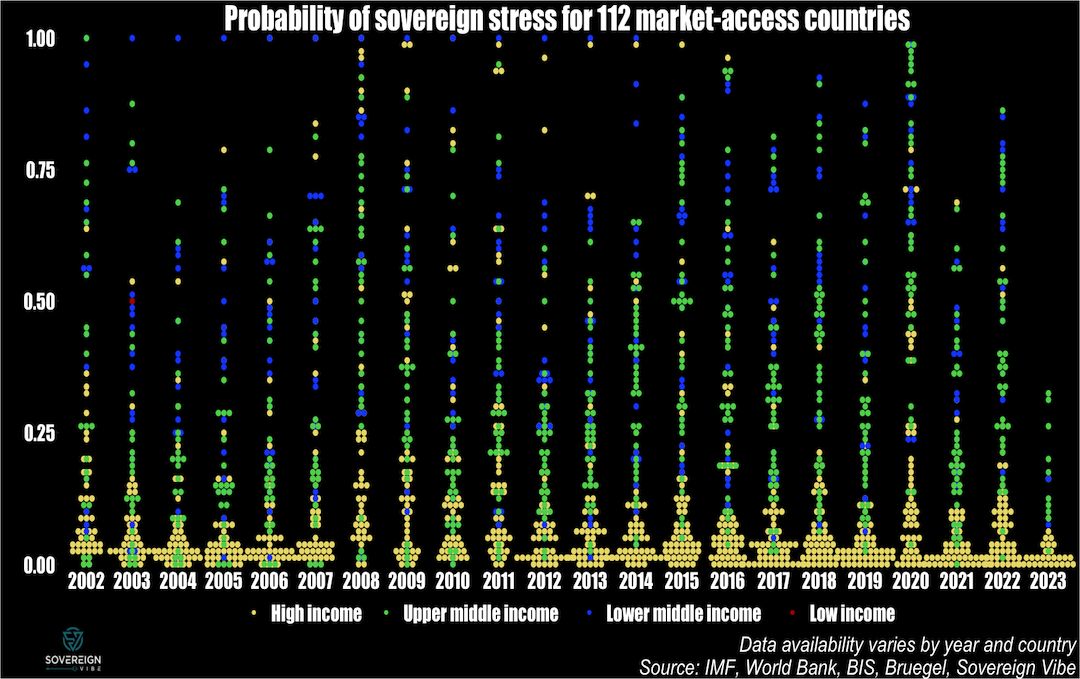

Introducing a sovereignstress tracker covering 100+ countries, based on the IMF’s Debt Sustainability Framework for Market-Access Countries.The model used in this analysis suggests that sovereign debt strains are lower in 2023 than they were in either 2022 or 2020 for this group of countries. MACs comprise all economies that are lower-middle income and above, including many emerging economies and all advanced economies.

Market-Access Countries

In 2021, the IMF released its new Debt Sustainability Analysis framework for Market-Access Countries, in line with its differentiation between MACs and low-income countries. The reasons given for distinguishing between these two groups is that MACs generally have significant access to international capital markets, whereas LICs rely on concessional resources to fulfill their external financing needs.

As such, the Fund has a separate approach to debt sustainability analysis for LICs, which is beyond the scope of this tracker. The strict definition is that countries eligible for the IMF’s Poverty Reduction and Growth Trust, which is an interest-free concessional financing tool, are treated as LICs, whereas the rest are considered MACs.

Geographic coverage

Overall, 140+ countries and territories were included in this analysis, but results were only obtained for 112,1Angola, Albania, United Arab Emirates, Argentina, Armenia, Antigua & Barbuda, Australia, Austria, Azerbaijan, Belgium, Bulgaria, Bahrain, Bahamas, Bosnia & Herzegovina, Belarus, Belize, Bolivia, Brazil, Barbados, Brunei, Botswana, Canada, Switzerland, Chile, China, Colombia, Costa Rica, Cyprus, Czechia, Germany, Denmark, Dominican Republic, Algeria, Ecuador, Egypt, Spain, Estonia, Finland, Fiji, France, Gabon, United Kingdom, Georgia, Equatorial Guinea, Greece, Guatemala, Hong Kong SAR, China, Croatia, Hungary, Indonesia, India, Ireland, Iran, Iraq, Iceland, Israel, Italy, Jamaica, Jordan, Japan, Kazakhstan, St. Kitts & Nevis, South Korea, Kuwait, Lebanon, Sri Lanka, Lithuania, Luxembourg, Latvia, Morocco, Mexico, North Macedonia, Malta, Mongolia, Mauritius, Malaysia, Namibia, Nigeria, Netherlands, Norway, New Zealand, Oman, Pakistan, Panama, Peru, Philippines, Poland, Portugal, Paraguay, Qatar, Romania, Russia, Saudi Arabia, Singapore, El Salvador, Suriname, Slovakia, Slovenia, Sweden, Eswatini, Seychelles, Syria, Thailand, Trinidad & Tobago, Tunisia, Turkey, Ukraine, Uruguay, United States, Venezuela, Vietnam, South Africa given insufficient data availability in around 30 cases. The analysis is based on a multivariate model, meaning that a missing data point for a single variable across all years makes it impossible to derive a final measurement for the country in question, resulting in exclusion.

The calculated probabilities of sovereign stress for the 112 countries do not cover all years, unfortunately. For instance, there are only results for 43 countries in 2023, given less availability of annual data and/or forecasts for the current year. Data coverage will be improved in future iterations of the tracker.

All countries included are either high, upper middle, or lower middle income countries, with few exceptions, such as Syria, which the World Bank reclassified as a LIC in 2018. There is also some debate as to whether Venezuela constitutes an UMIC or a LMIC, though it is treated as a LMIC here.

Model

The IMF claims that extensive testing demonstrates that its new MAC DSF is much better at accurately predicting sovereign debt distress. Predictive analysis is based on a multivariate logit model developed by Fund staff. Passing the required data into the model provides a probability that a sovereign borrower experiences debt stress:

Multivariate logit model specification

Regressor

Coefficient

Institutional quality

-1.073 ***

Stress History

0.514 ***

Current account balance/GDP

-0.024 **

REER (3-year change)

0.013 **

Credit/GDP gap (t -1)

0.086 ***

Δ Public debt/GDP

0.052 ***

Public debt/revenue

0.002 ***

FX public debt/GDP

0.024 ***

International reserves/GDP

-0.034 ***

ΔVIX

0.015 ***

*** / ** indicate statistical significance at the 1 percent / 5 percent levels

Results

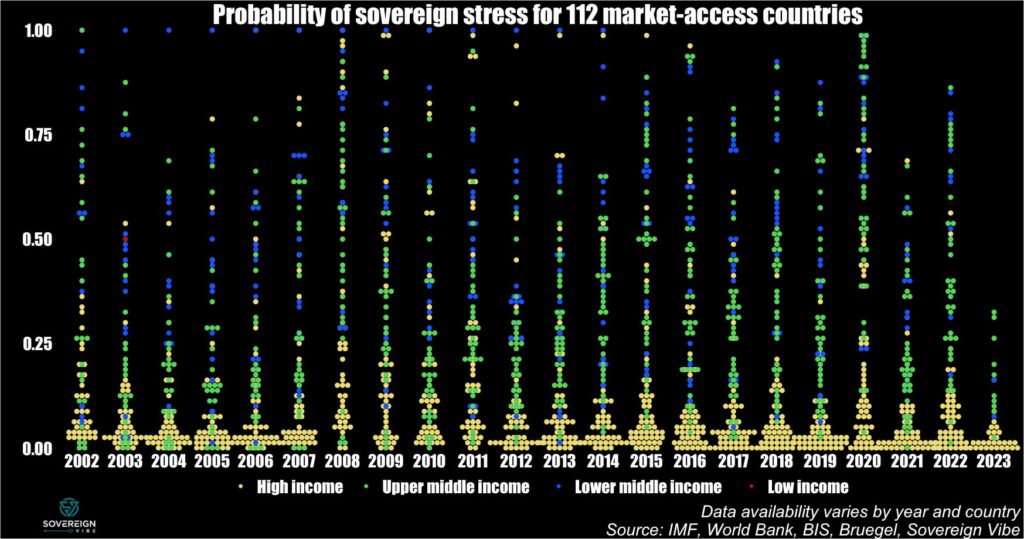

In addition to the dotplot chart above, a further way to view the broad results from this analysis of 112 countries is as a boxplot, presented below. I fully acknowledge that this data is unbalanced, given the limited number of data points in 2023 and also in the early 2000s – as can be seen in the first chart above – compared to better country representation in the middle years of the sample. More charts are presented in the next section below in order to address this issue.

As can be seen in the data, in 2023 there appears to be less systemic sovereign stress among MACs as compared to previous years, particularly 2022 and 2020. Future posts will provide granular details and heatmaps at the country level.