Debt management offices in emerging market finance ministries should be prepared for Fed rate cuts.

Emerging market sovereign debt issuance started 2024 off strongly with record-breaking issuance in January at ~$47bn and another ~$16bn in February, marking the highest January-February result since before the pandemic. Sub-Saharan African sovereigns even returned to the Eurobond market, with Côte d’Ivoire leading the way and Benin placing a debut issuance. Larger players including Saudi Arabia, Mexico, Indonesia, Hungary, and Romania made placements as well.

With borrowing costs having immediately fallen in the wake of Federal Reserve Chair Jerome Powell’s dovish comments on US inflation in December, the start-of-the-year timing for issuance was savvy given renewed concerns since March around higher-for-longer interest rates. With the 10-year US Treasury yield having climbed nearly 600bps since early March and the dollar also strengthening, debt management offices have likely become more circumspect regarding US inflation and the Fed.

The fading prospects of US rate cuts before H2 haven’t put a halt to activity this April out of Abu Dhabi and, more absurdly, El Salvador. And other debt management offices, including Tanzania, are also considering Eurobond issuance. Apparently EM sovereigns have issued about $93bn so far this year, which means about $30bn for March-April. These are still big numbers, but nothing close to that fast start in January.

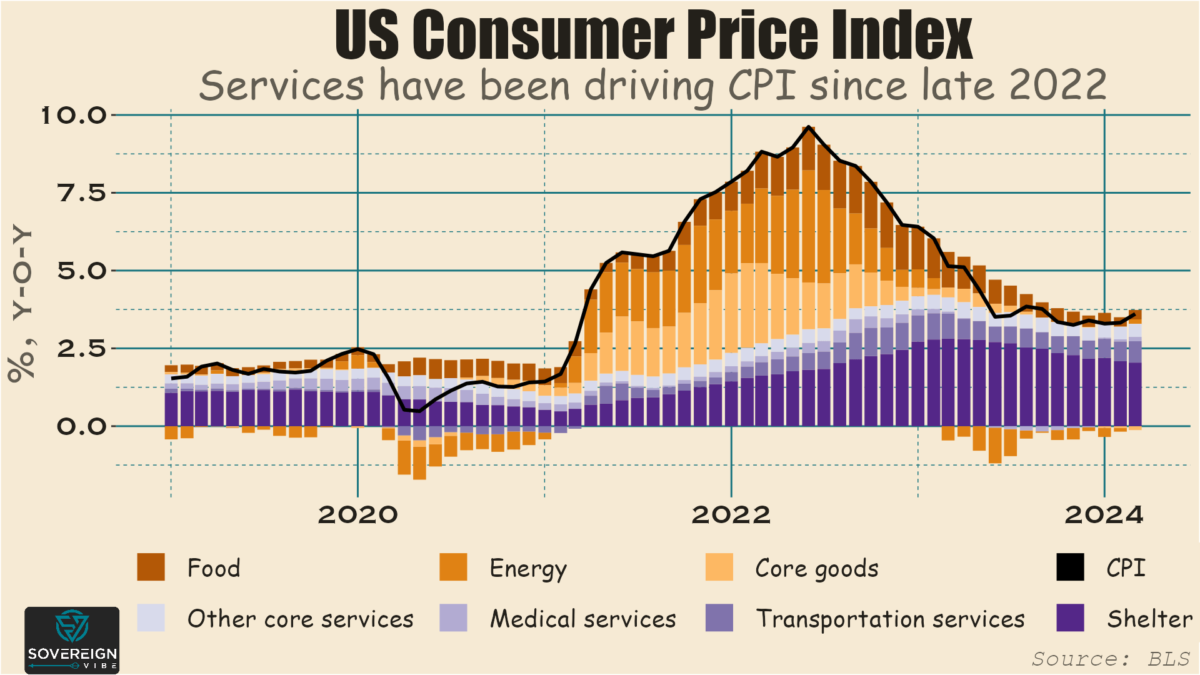

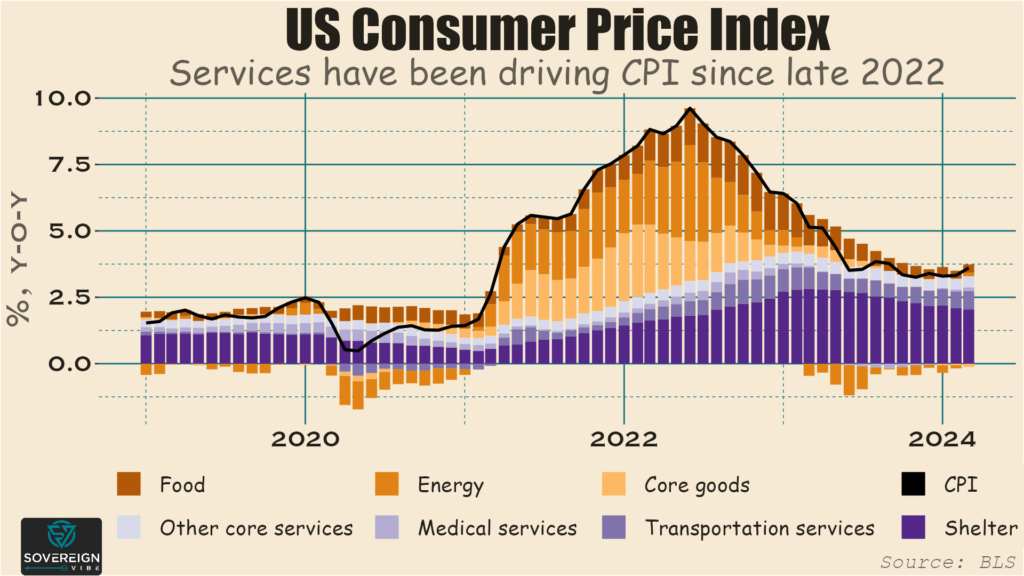

Friday’s US inflation print came in hotter than expected, fueling ongoing concerns that rates will have to stay high for a while yet. The Fed’s preferred metric is core personal consumption expenditures (i.e. ex-food and energy), which rose 2.8% year-over-year in March – a third high monthly reading in a row. But digging through US data shows that the Fed may yet bring inflation lower soon. Looking at the consumer price index provides more granularity than is easily available through PCE, though it measures slightly different things.

In any case, it’s clear that almost all price pressures are emanating from services, with core (i.e. ex-food and energy) goods inflation having even turned negative. Within services, the largest component is shelter, which is often the case historically as well, but shelter inflation has moderated significantly over the past several months.

The main inflationary challenge is actually in the transportation services segment, which accounts for the lion’s share of services ex-shelter inflation. Within this category, motor vehicle insurance prices have been surging, e.g. 22% y-o-y in March, due to lingering Covid-era supply chain effects, changing car technology, higher car prices, and higher repair costs. It is likely that these factors are now locked in and will not rise much further, if at all. With the high base effect is now baked in, transportation services inflation will almost certainly fade over the coming months.

The upshot is that emerging market DMOs should expect US inflation to moderate over the coming months and for the Fed to cut rates at some point this year – and perhaps sooner rather than later. So I wouldn’t be surprised to see a pick-up in EM issuance again this year, though investor demand may be more for EM IG than for EM HY. Whether it’s wiser to place a Eurobond or a local currency bond, and whether offices should hedge their currency exposure in the former case is another matter. In the meantime, let the roadshows begin?

One of the major announcements at last week’s World Bank/IMF Spring Meetings concerns the unsustainable rise in US government debt. While it’s old news that the budget deficit is large – $1.7tn / 6.3% of GDP in 2023 and a projected $1.6tn in 2024, I want to highlight how US debt relates to the the role of the dollar internationally. Besides, the Springs also mean there is new IMF WEO data to play with:

De-dollarization has become a hot topic in recent years, with many observers siding ideologically “against” the USD, e.g. Brazil’s president Lula asking why international transactions should occur in dollars. Many also claim that the yuan and other BRICS currencies are rising in importance. While it’s true that RMB is playing a greater role in trade invoicing and international reserves, this increase is limited to either specific countries (e.g. Russia) or has been less than the rising prominence of other G7 currencies.

Yet such grandstanding belies ignorance of why the greenback is so dominant. China scholar and Carnegie Endowment fellow Michael Pettis explains this with his usual brilliance.

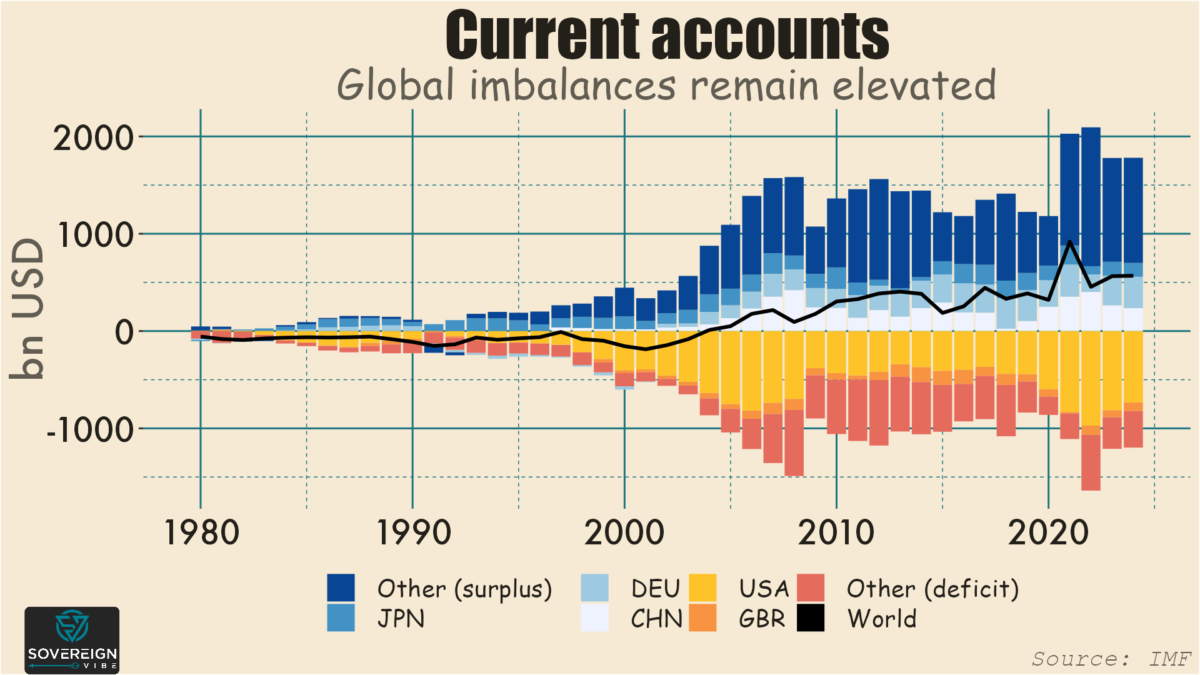

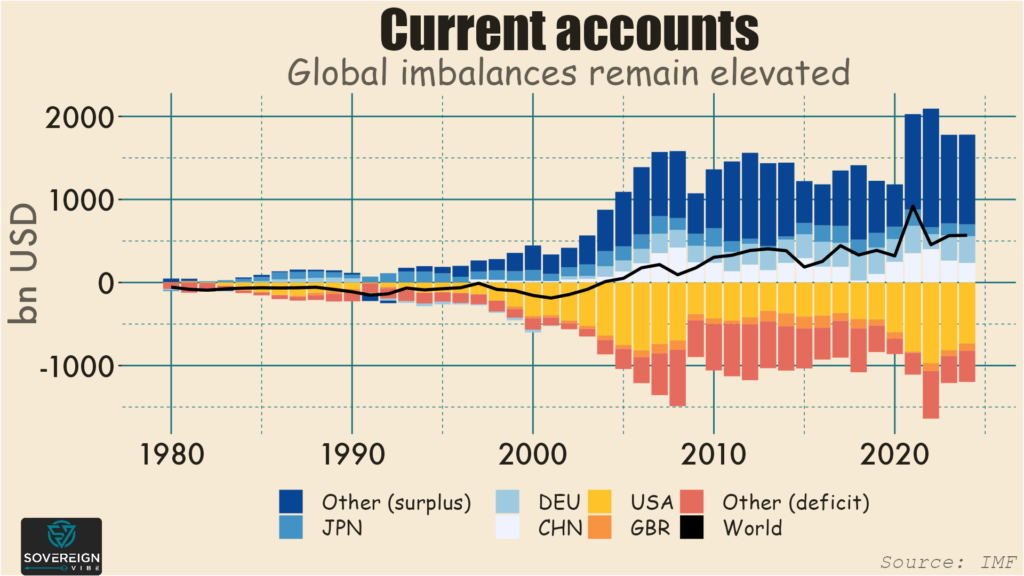

Essentially, countries that run current account surpluses – (remember that the current account is the trade balance plus other sources of foreign income) – are subsidizing manufacturing. China and Germany are prime examples.

In contrast, deficit countries are subsidizing consumption. The US and – to a much lesser extent – the UK have the largest average current account shortfalls in dollar terms.

One way to think about current accounts is that they are equal to savings minus investment, on a national level. Savings is of course the difference between income and consumption. So, when a country has a positive current account balance, it is saving more than it is investing. The reverse is true for CAB deficits:

Current Account Balance = Savings - Investment

It follows that for a current account to rise, savings increases and/or investment decreases. For a current account to decline, savings decreases and/or investment increases.

Capital account

Another important piece of the puzzle is the capital account, which is open in the US and other G7 countries, but not in China. Investors understandably prefer to send their capital to countries with strong property rights, institutions, and rule of law. These robust investor protections is one of the reasons why the US and the UK and, to a lesser extent, Canada and Australia have such large deficits.

In other words, in countries with open capital accounts, when net international capital inflows are positive, the balance of payments means that the current account has to be negative (barring some potential temporary effects via international reserves dynamics).

Transfers, both internal & external

Surplus countries such as China, Germany, and Japan subsidize manufacturing at the expense of domestic consumers. Low interest rates and low wages, in China and Germany’s cases at least, result in net transfers from savers (i.e. households and workers) to manufacturing firms. Along with their manufactured goods, they are also “exporting” weak domestic consumer demand to other countries.

To resolve this external imbalance, deficit countries like the US and UK have to either decrease savings and/or increase investment. But, with companies either holding large cash balances or using them to buy back stock, there seem to be few signs of increasing investment. This means that savings must be negative. This can occur via increased unemployment, but, to avoid this, the government instead subsidizes consumption (at the expense of manufacturing) via increased household and/or government debt.

As such, exploding US government debt is partly a result of these external trade imbalances. This begs the question why the US accepts an undervalued yuan and large negative trade deficit with China, though the White House has certainly pushed back against this arrangement at various points.

Narrow interests

As is often the case, the status quo is a result that serves a specific set of narrow interests. With the US running such a large current account deficit, other countries acquire US financial assets denominated in dollars, meaning that the US exports its financial assets to the rest of the world. Doing so ensures the dollar’s status not only as a store of value but also as a medium of exchange internationally, which is what gives the US government power to levy financial sanctions and US banks power to dominate transactions.

Yet this situation is neither sustainable for the US government and households, nor is it desirable for most Americans. Even disregarding the overuse of sanctions, the effects of USD prevalence are negative abroad as well. For instance, greenback dominance has generally resulted in a strong dollar, which is not beneficial for global trade.

Unsustainable status quo: here to stay?

In fact, the global trading system works terribly. Ideally, wealthy countries would run surpluses, and EMDEs would run deficits in order to funnel rich-world savings towards domestic investment. But EMDEs present a variety of risks to investors, who prefer to have higher allocations to safer countries, e.g. the Anglosphere.

It is not the yuan or some other currency that will dislodge the dollar. Rather, it would be some combination of push and pull factors outside and inside the US. China and other surplus countries could stop incentivizing manufacturing and instead increase consumption and, in some cases, investment. US policymakers could reduce fiscal and household debt accumulation while encouraging exports of goods and services.

In both the surplus and deficit cases, restoring that balance between consumption and manufacturing would have broad-based economic benefits. Unfortunately, the prospects for either of these outcomes seem remote because of the political priorities of Beijing’s surplus maximization and of Washington’s dollar weaponization, both of which are cornerstones of this deglobalizing era. Yet since these imbalances are so unsustainable, something’s gotta give, someday.

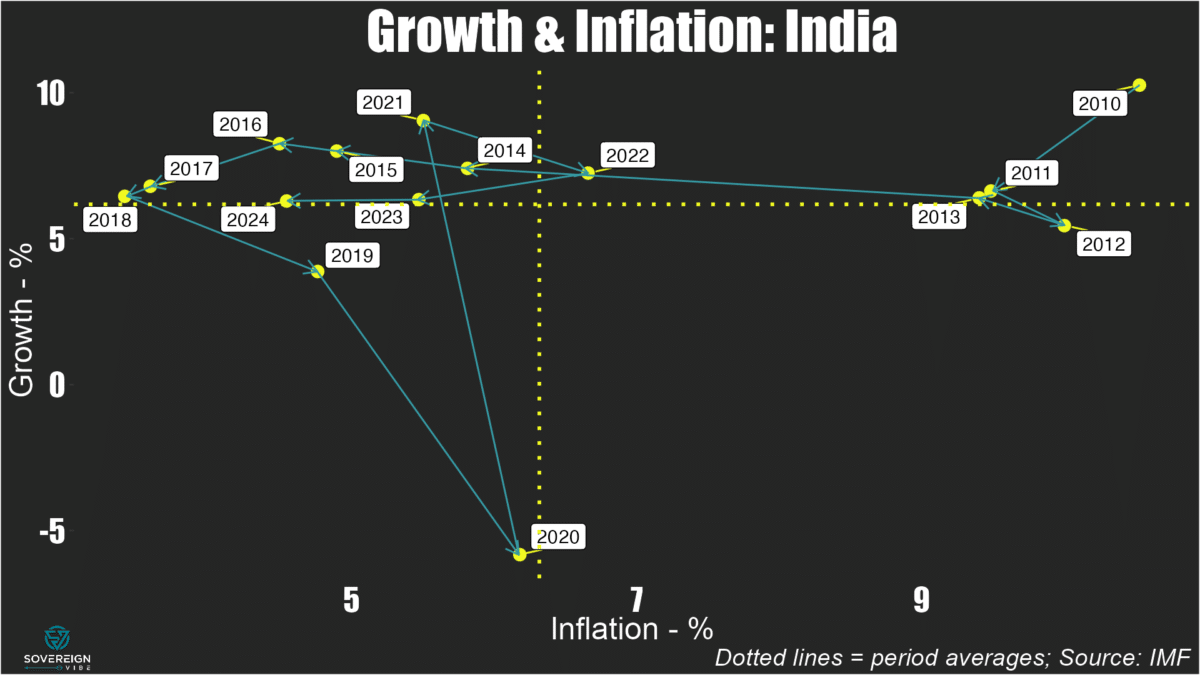

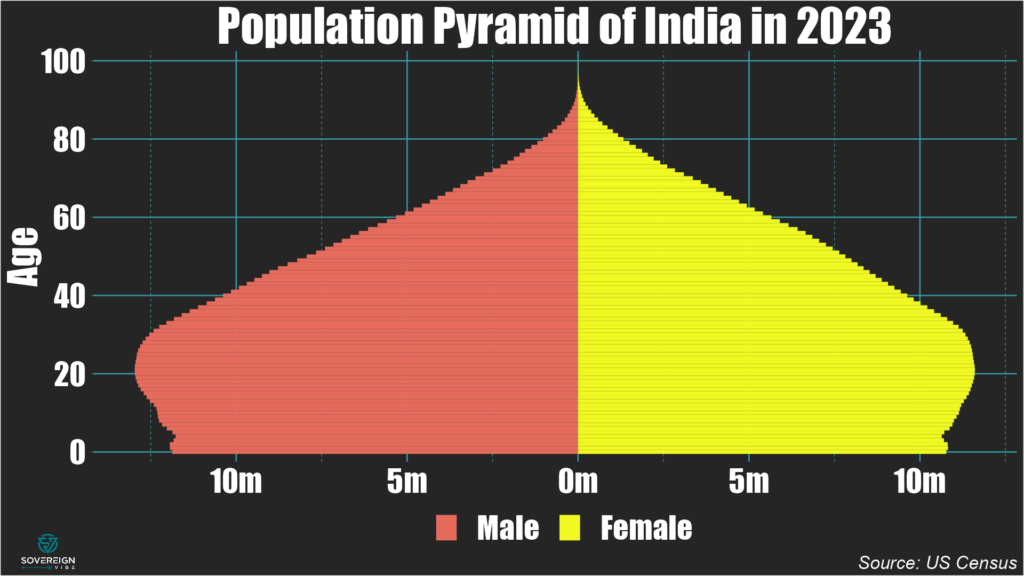

India’s economy is in great shape as it heads to the polls… but something’s off.

With India’s general elections getting under way on Friday, much of the focus this week will be on the world’s most populous country and largest democracy. So here are some charts to help you look beyond the headlines and arm yourselves with some facts.

Modi’s mojo

South Asia is the fastest-growing of all emerging market and developing economy regions, largely thanks to robust growth in India on the back of strong public investment and dynamic services.

Growth rebounded strongly thanks to a post-2020 base effect, breaching 9% in 2021 before moderating to ~7+% in 2022 and ~6+% in 2023 and 2024. These are excellent numbers, particularly given that inflation is gradually declining towards the Reserve Bank of India’s 4% target. All of this situates growth and inflation above and below their averages since 2010, respectively (see chart below). So it is little wonder that Narendra Modi’s BJP is so strongly positioned as India heads to the polls.

A global perspective

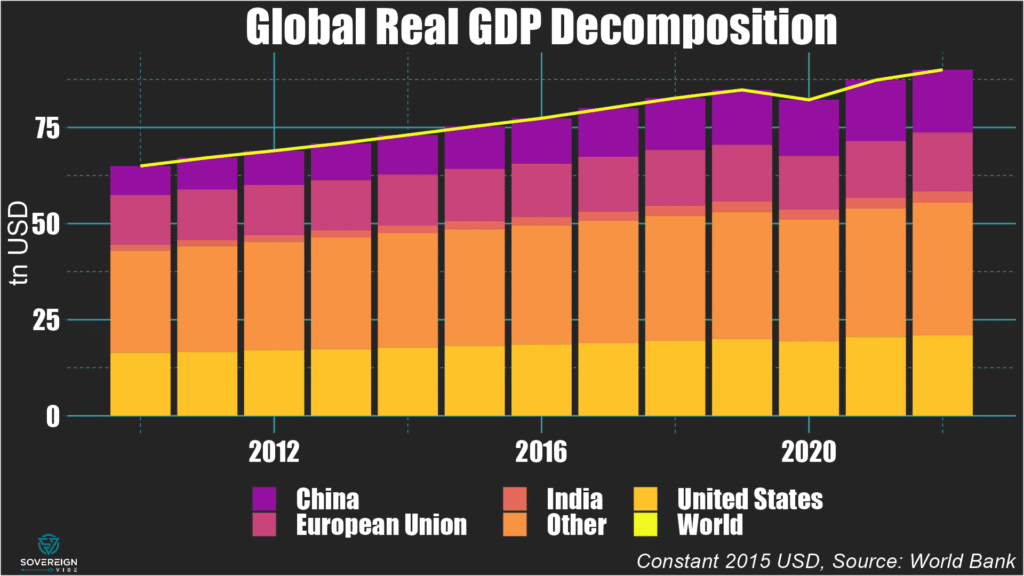

Zooming out, India’s population is still heavily under-represented in the global economy. Its 1.4bn+ souls account for nearly 18% of the world’s total, while its share of global GDP is only a bit above 3%.

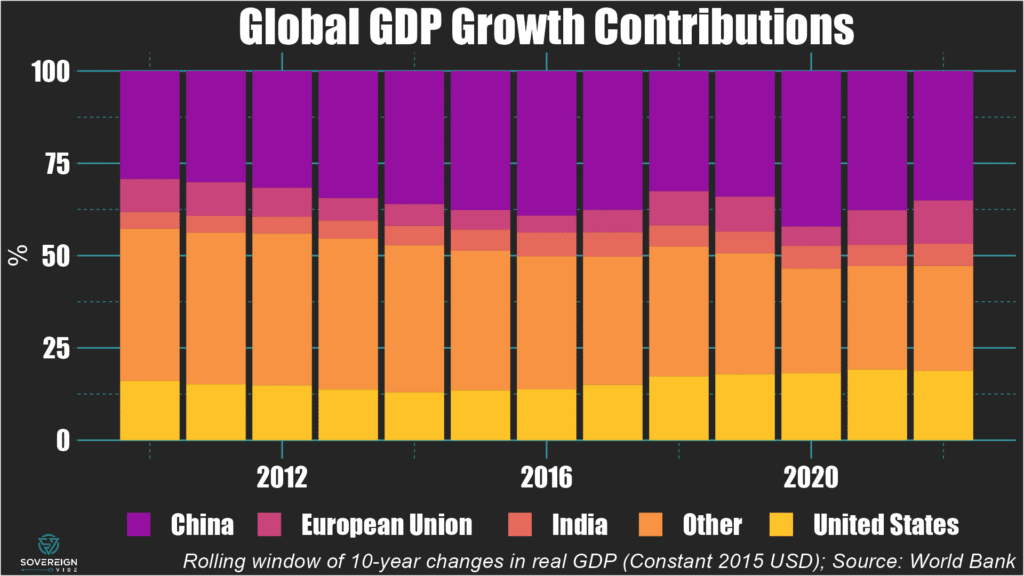

Yet the country is certainly punching above its weight when it comes to contributions to global GDP growth, as it is contributing 6% of global growth (see chart below) from its 3% slice. This ratio is likely to evolve favorably for India in coming years as China’s growth continues to slow.

Demographics

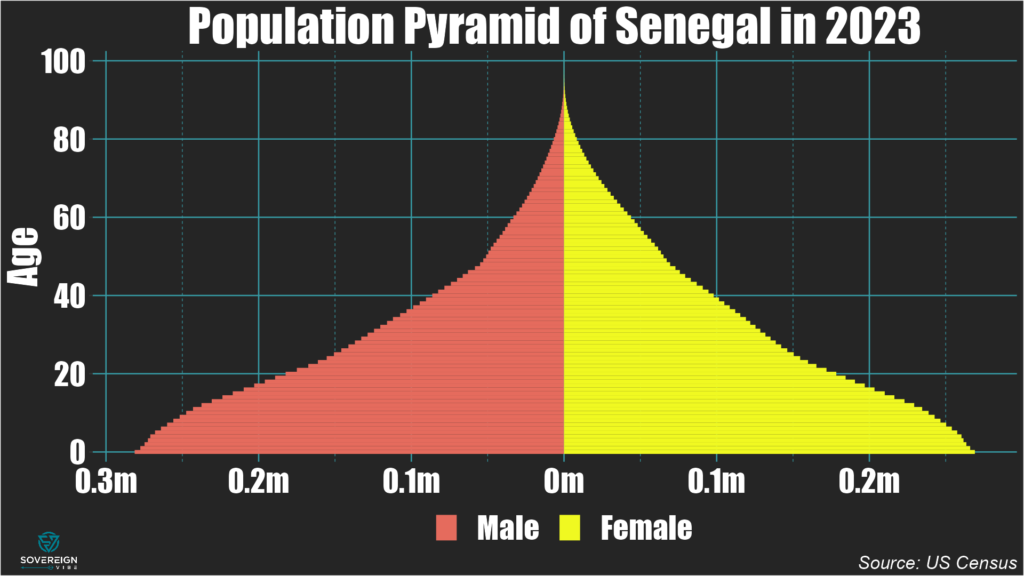

The pyramid below has an ideal shape for economic growth in India over the next decades. A huge cohort of young people – the world’s largest – is moving into the workforce, even as birth rates moderated over the past couple of decades. This will decrease the dependency ratios of the young and old on people of working age and likely contribute strongly to growth, savings, and development in the years ahead.

However, it is concerning to see such a large imbalance between the number of men and women in India, with men far outnumbering women. The gap is as wide as 2 million for each age for people in their 20s and 30s. It is estimated that there are around 106.5 men for every 100 women in the country. This is the type of ratio that could potentially lead to instability and violence under certain conditions, though hopefully India’s robust output growth can continue to be somewhat of a palliative to that.

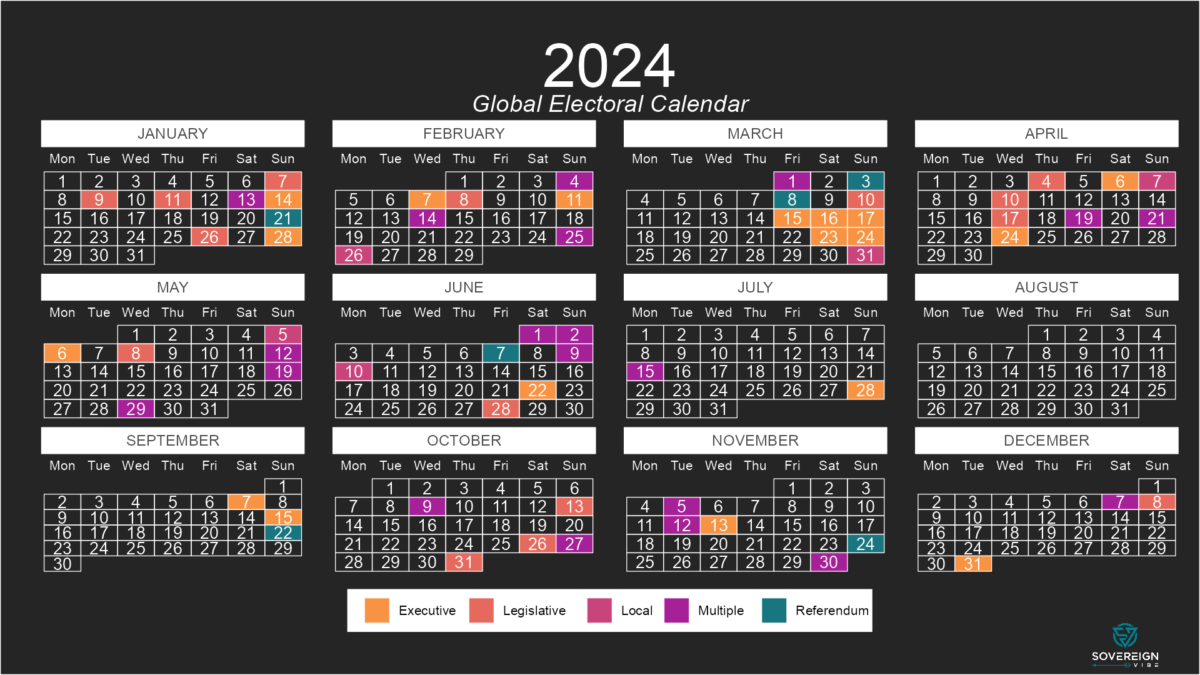

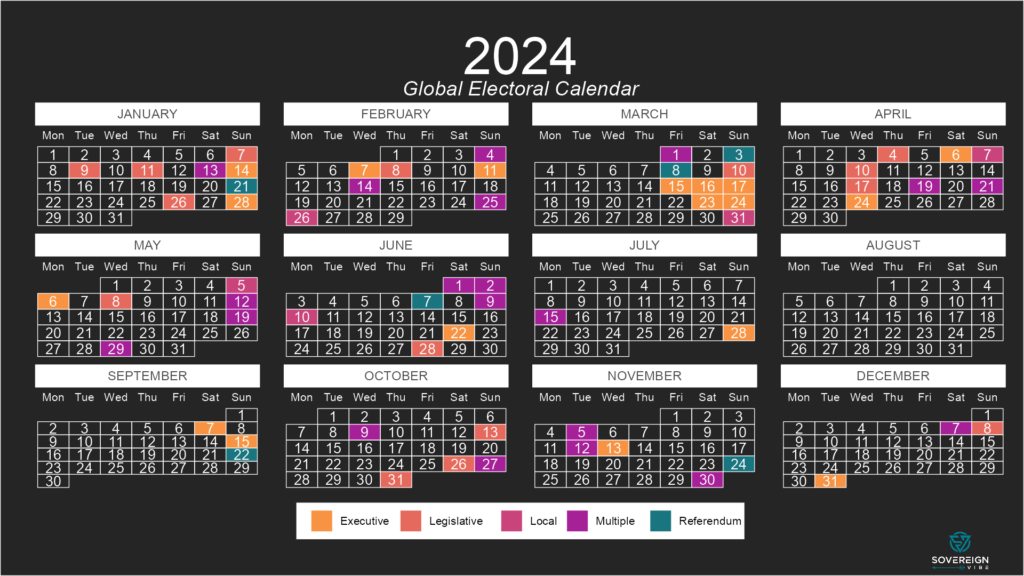

With so much of the world headed to the polls in 2024, a quick stock-take of results so far and a look ahead are in order. The outcome of each contest shapes broader international trends of deglobalization.

Of populists & liberals

The paradox is that both populist and liberal political parties have pursued policies leading to international economic fragmentation. On the populist side, trade tariffs à la Trump are the most obvious example. Populism has of course also lead to schisms in western cooperation, whether Republican reticence on NATO and Ukraine, or pro-Russian leadership in Hungary and, more recently, Slovakia (see below).

Liberal political forces are also responsible for deglobalization. The prime example is the widespread use of economic sanctions by the Biden administration and Western Europe against Russia. Yet the current US administration has not only kept the Trump era’s trade barriers in place, it has also introduced more protectionist measures through the landmark Inflation Reduction Act.

Moreover, the success of liberal parties in the broad West can benefit cohesion among allies at the expense of decoupling from opponents. Case in point, Finland’s new president comes from a pro-Europe, pro-NATO party, highlighting how joining NATO bolsters cooperation within the West while also – quite understandably – turning away from Russia.

Populism has the edge

Despite these nuances, a high-level view of electoral outcomes around the world sheds light on the direction that future international economic relationships will take. By the end of the year, the US, India, Indonesia, Mexico, and many other countries will have voted. The question isn’t so much whether the world will continue to fragment, but rather how, which is what monitoring elections can help answer.

So far this year, populist forces have advanced to varying degrees in Slovakia, Indonesia, Senegal, Poland, and will likely maintain power in India. The military continues to loom over politics in Pakistan, while Bangladesh’s authoritarian Awami League has left virtually no space for any opposition.

In contrast, results in Taiwan, Finland, and Turkey have favored more liberal political parties. Similarly, upcoming legislative elections in South Korea will likely see the center-left and center-right parties continue to dominate the political landscape.

Electoral highlights year-to-date

Poland: The nationalist, opposition PiS party came out ahead in local elections on April 7th, but Prime Minister Tusk’s ruling coalition will likely hold on to power in most regions.

Slovakia: The result of April 6th’s second round runoff in Slovakia are in, with the ascension of pro-Russian politician Peter Pellegrini to the presidency confirming the country’s pivot towards Moscow, after Robert Fico’s return as Prime Minister in October 2023.

Turkey: The victory of the opposition Republican People’s Party in local elections on March 31st were a setback to President Erdogan’s ruling AKP, with Istanbul’s mayor Ekrem Imamoglu strengthened by this outcome.

Indonesia: The general election on February 14th marks a turn away from incumbent Joko Widodo’s center-left PDI-P to the nationalist, right-wing populist Gerindra party under current defense minister Prabowo Subianto, who will be sworn in as president in October.

Pakistan: International media have contested the fairness of the February 8th elections, though former prime minister Imran Khan’s PTI secured the largest share of the vote despite being in prison. The PML-N’s Shehbaz Sharif is now prime minister of a coalition government.

Senegal: Political novice Bassirou Diomaye Faye rose to the presidency in the March 24th election, defeating the government-backed candidate. Although Faye has announced several significant policy changes, the composition of his economic team has reassured investors.

Taiwan: The results of the January 13th presidential election represent continuity for Taiwan in its opposition to the One China policy, with the center-left DPP’s Lai Ching-te to be inaugurated as president in May 2024.

Bangladesh: The US State Department claims that January 7th’s general election wasn’t free and fair. In power since 2009, incumbent Prime Minister Sheikh Hasina of the Awami League has won election for the fourth consecutive time.

Finland: The January 28th and February 11th two-round presidential election resulted in the victory of Alexander Stubb, of the pro-NATO, pro-European liberal-conservative National Coalition party.

April elections

India: While there is little doubt that Narendra Modi’s BJP will secure victory in the seven-round general election, the Lok Sabha, running from April 19th – June 4th, it appears voters are willing to accept some democratic backsliding in exchange for stronger economic growth.

South Korea: The center-left DPK holds the most seats in the National Assembly, while its historic rival, the conservative PPP, holds the presidency. These two main parties appear to be neck and neck in polling for the April 10th legislative election.

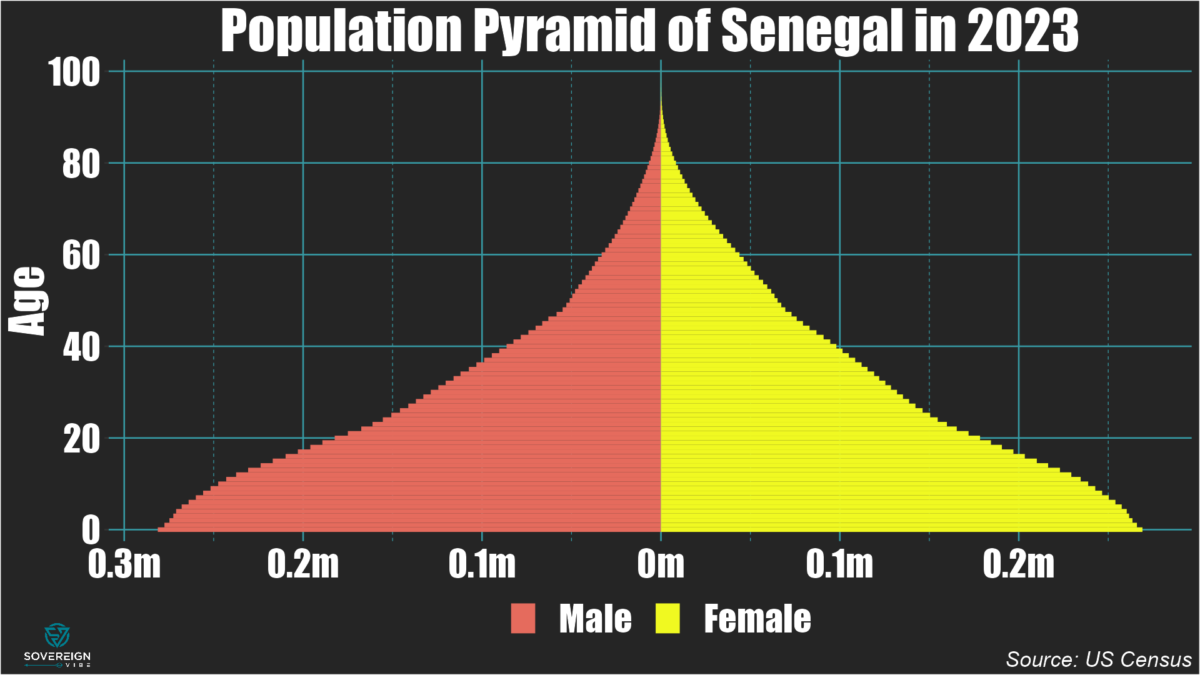

Today’s spotlight is on Senegal’s presidential election in March 2024 and the spectacular rise to power of political novice Bassirou “Diomaye” Faye, a 44-year old former tax inspector who went from prison to the presidency in scarcely 10 days. Digging beneath the surface of the electoral results reveals some oft-neglected ethnic undercurrents at play in Senegal and elsewhere in the Sahel that investors and observers should keep front of mind.

Why democratic stability is so rare in the Sahel

One of the things that struck me when living and working in Africa was the yawning gap between the international press coverage of electoral politics and the realities on the ground, which were both obvious and patiently explained to me by local friends.

I am of course referring to the ethnic dimensions of politics that are ever-present in so many African countries but that mainstream international media so often ignores.

In Africa, ethnicity doesn’t explain everything, but nothing can be explained without ethnicity.

Bernard Lugan

Democracy wins

Last month’s presidential elections in Senegal were first and foremost about the Senegalese people expressing their desire for change. As things currently stand, it is also a positive story of the country’s institutions resisting to pressure.

Indeed, Senegal has come back from the brink, after outgoing president Macky Sall sought to delay the elections indefinitely, and which – thankfully – the Constitutional Council overruled. The vote on 24 March saw opposition candidate Bassirou “Diomaye” Faye win a resounding victory that precluded the need for a second round runoff. A former tax inspector and political novice, Faye had been released from politically-motivated imprisonment only days before.

Source: Senegal’s Presidential Office, via Reuters & Le Monde

Yet the triumph was above all for Senegalese democracy, with government candidate Amadou Ba conceding the next day. The country thus remains a beacon of democratic stability with peaceful transitions of power since independence in an otherwise fragile region that has recently suffered a wave of coups d’état: Mali, Burkina Faso, Niger, Guinea. Beyond West Africa, Sudan, Chad, and Gabon have each had recent, idiosyncratic, coup-like political instability as well.

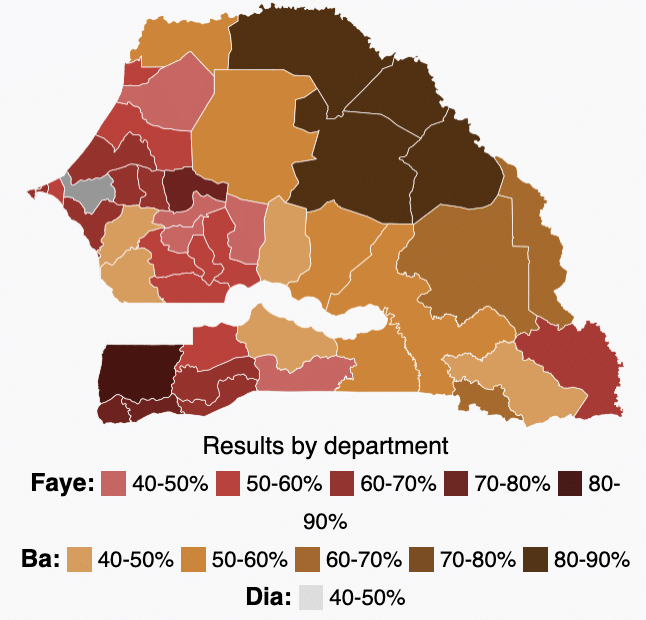

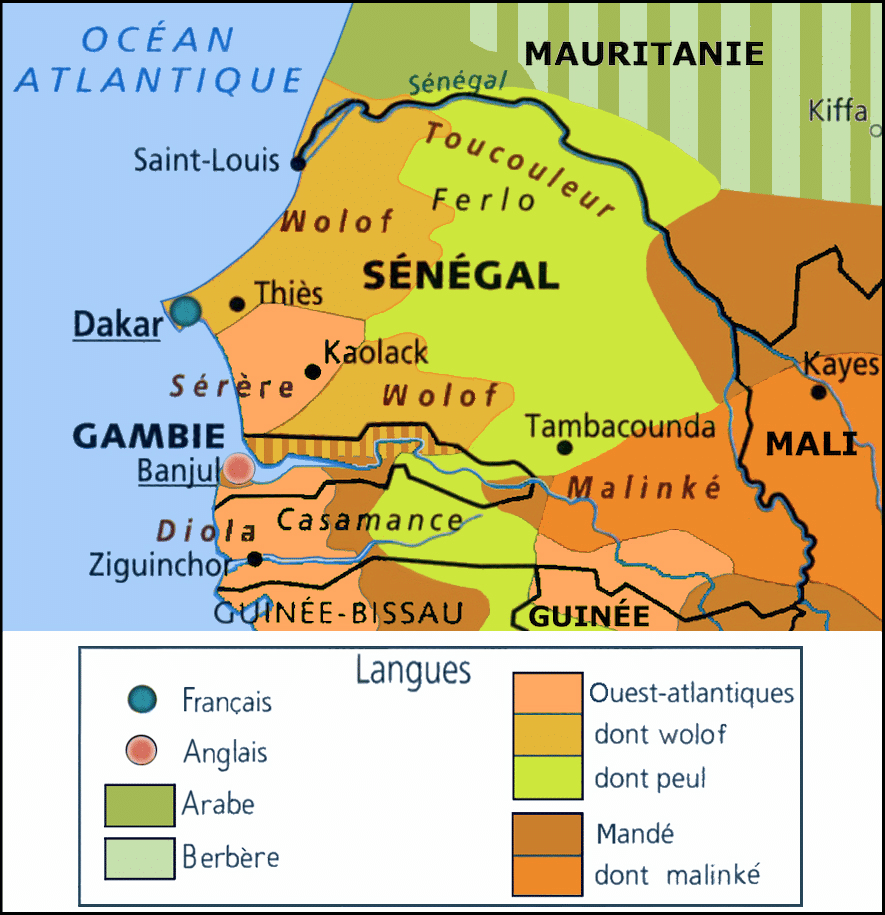

Mapping the ethnic X factor

I don’t want to exaggerate the importance of ethnicity in this election. For all intents and purposes, the result is a clear repudiation of Sall’s government and his anointed would-be successor, Ba, and overrides potential ethnic considerations.

Nevertheless, comparing a map of the electoral results to an ethno-linguistic map of Senegal suggests that ethnicity is still important. Sall is Fula (in French: Peul) and has had his political stronghold in the northern parts of the country, where many Fula live. These voting patterns were borne out in March’s election, with Ba getting much of his support from Fula-populated areas.

Source: Wikipedia

Source: G.G. Beslier, Le Sénégal

In contrast, Faye was much more dominant in areas populated by the Wolof, the Mandé / Malinké in the southeast and south, and in the southwest. Faye was until recently the right-hand man of Ousmane Sonko, who was ultimately prevented from running in the election. Sonko hails from the southwestern city Ziguinchor, where Faye secured a strong turnout, and has been chosen as prime minister.

The Sahelian ethno-democratic-demographic doom loop

On a continent that crams some 3000 ethnic groups speaking around 2100 languages into a mere 54 countries, it is myopic to completely ignore the ethnic undercurrents at play, even in cases where it isn’t the primary driver. Yet analyzing the political salience of ethnicity in Africa is more than just a useful intellectual exercise.

Think how, for example, as the largest nomadic pastoral community in the world, the Fula are present in Senegal and Guinea, and in Chad and Cameroon, and in every country in between. As climate change drives the Sahara’s expansion ever southward through the Sahel, we can expect land use-driven tensions to continue rising between the more martially-oriented nomadic pastoralists of the north and the more numerous sedentary agriculturalists to the south.

To that point on demographics, Western democratic ideals imposed on an African context partly explains many countries’ breakneck population growth. Individualism is at the center of the one-person one-vote approach to electoral democracy and works well in many parts of the world. But traditions of individual liberty were only introduced to African countries recently, where, historically, communitarian-led structures of societal organization tended to dominate.

Senegal’s population is growing at a rapid clip.

Thus Western-style democracy has incentivized each ethnic group to vie for political power by growing its population. This makes complete sense if one recognizes the communitarian focus that continues to drive politics in so many African countries to this day. Case in point, as of 2023 Senegalese women give birth to four children on average, and 75% of the country’s population is under 35 years old. Of course, the usual caveat applies: no single factor is fully responsible for a demographic outcome.

The bitter irony is that democracy has destabilized several of Senegal’s neighbors precisely because it has inverted the power relationship between the previously-dominant nomads and the sedentary farmers. Historically, these fierce warrior-pastoralists didn’t really require strength in numbers to subjugate their more pacific southern neighbors.

But in a context where democracy excludes the nomads from political power, it should not be at all surprising that these peoples would try to revolt or secede. This is precisely the driving force behind the ongoing conflicts and instability across the near-entirety of the Sahelian arc, rather than some inchoate jihadism. The several Tuareg / Azawad rebellions that have occurred since the 1960s serve as a prime example. Senegal alone has been spared. For now.

With all that in mind, can a victory of democracy in an African context be anything other than a pyrrhic one? I certainly hope so, and Senegal’s institutions give good reason to. Yet even as this result is rightly celebrated, the specter of roiling demographics and instability throughout so much of the region looms large over West Africa’s future.

What next for investors?

Investors have so far reacted to Faye’s victory with caution, as he is in many ways an unknown entity. It is still early days, so investors ought to remain circumspect while waiting to see the shape that his economic policies end up taking.

For now, what we know from Faye’s inauguration is that the economic agenda will focus on reducing cost-of-living pressures and on tackling corruption, while also having to address the high unemployment rate in this youthful country. On the external front, Faye and Sonko have espoused sovereignty and deep change, including reforms to or a complete transition away from the CFA currency.

Abandoning the CFA could prove tricky, as the currency has been a source of stability throughout much of the region, aside from a sharp devaluation in 1994. On the other hand, Senegal likely has the policy credibility and institutional strength to pull it off. Moreover, the CFA is almost certainly highly overvalued, so the move to a more flexible currency could benefit export activity.

The French Connection

As for the relationship with France, Sall had kept close ties while also diversifying Senegal’s partners. It seems likely that Faye will keep Paris at arm’s length, without necessarily shutting the door entirely, if the cordial 30-minute conversation he had with Macron last week is anything to go by.

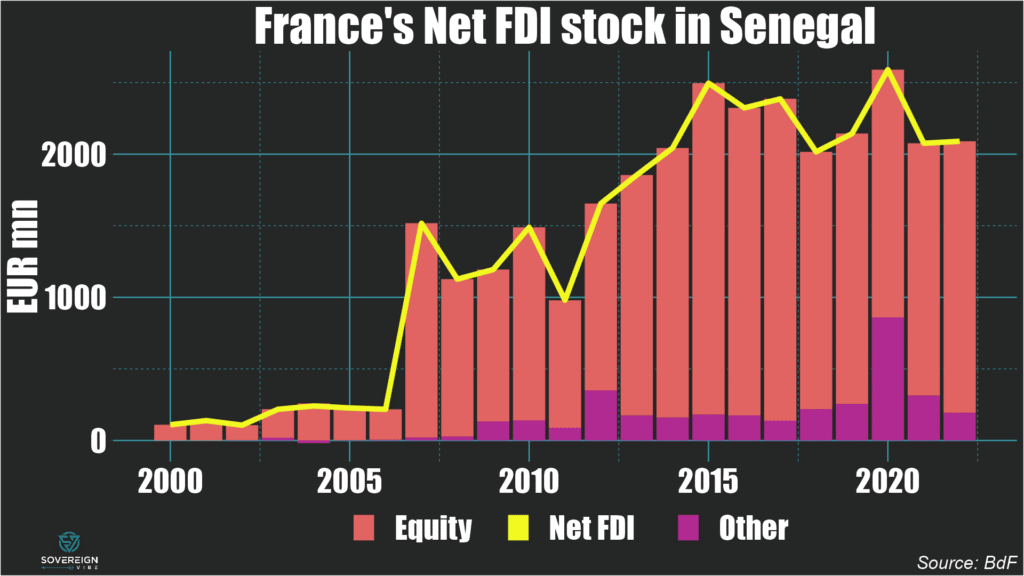

In the meantime, France’s net foreign direct investment stock in Senegal has remained above the €2bn mark in recent years, unlike declines in the French economic presence that have been registered elsewhere in francophone Africa. This level of FDI involvement in Senegal is close to 8% of GDP and represents nearly a fifth of FDI in the country, underscoring the ongoing presence that French economic interests are likely to have.

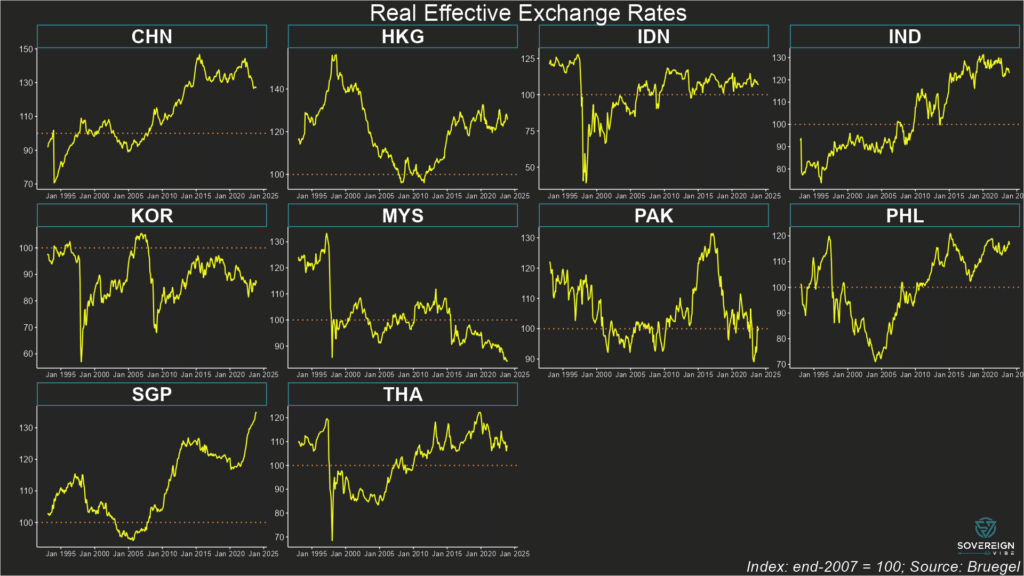

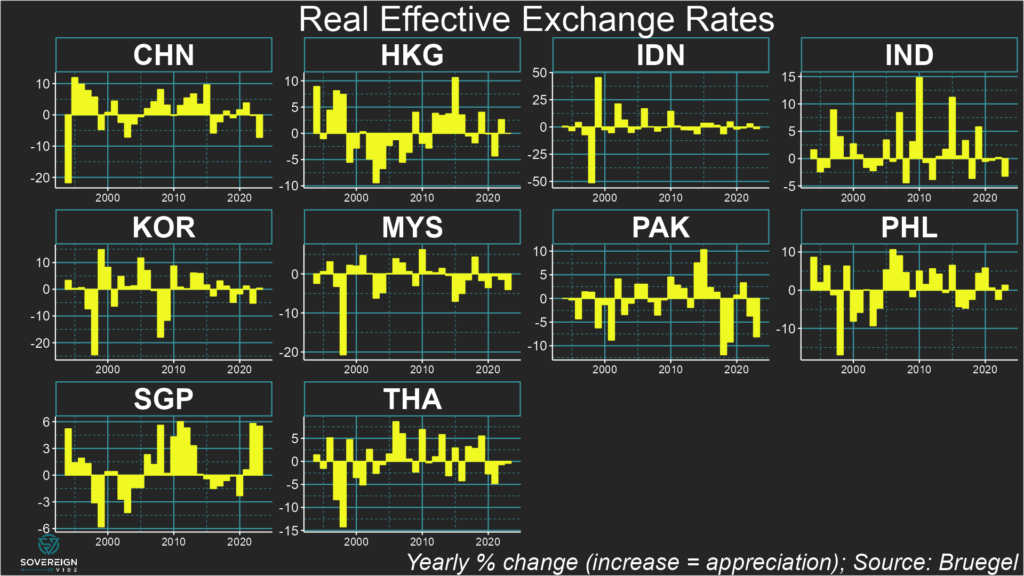

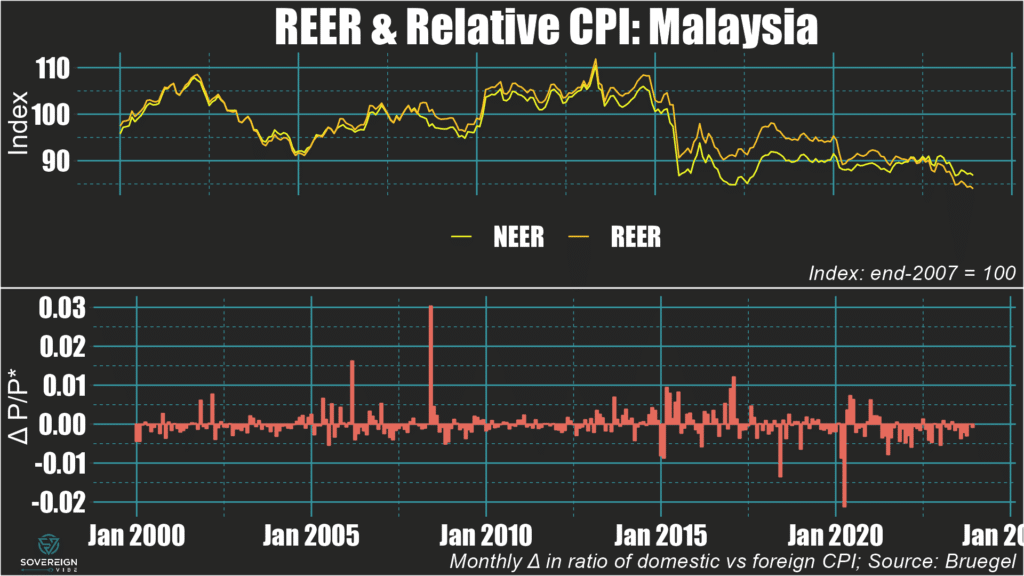

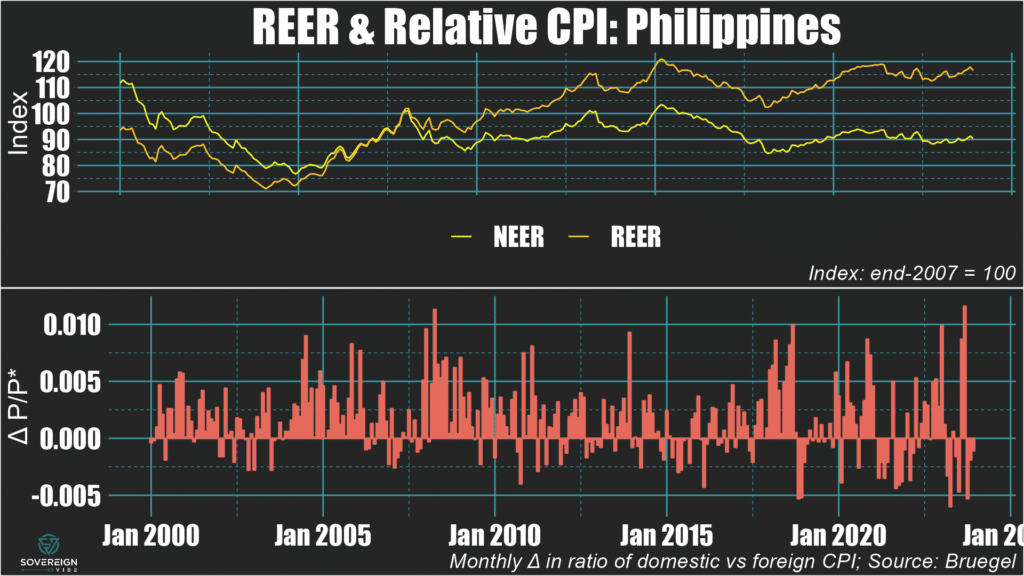

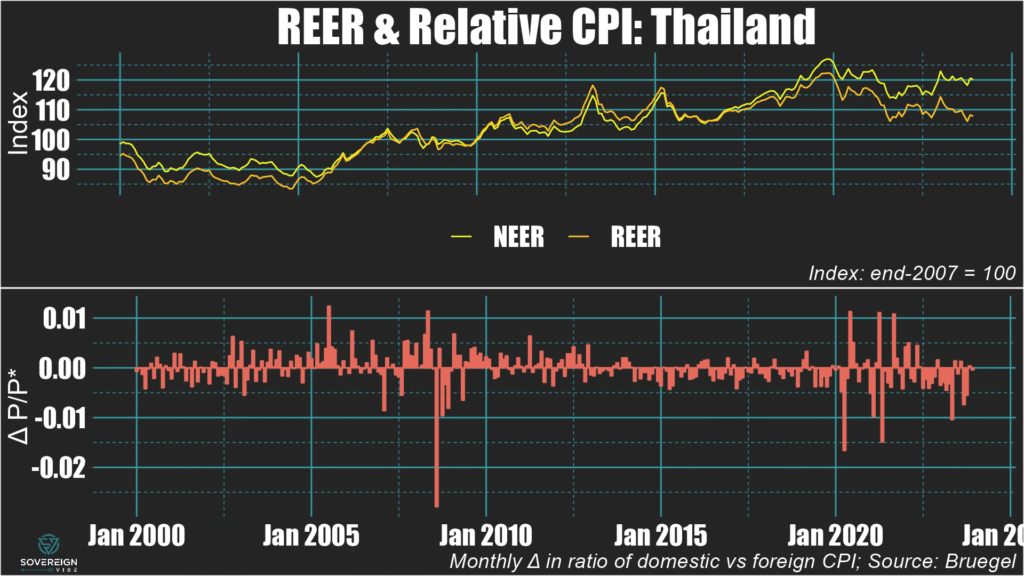

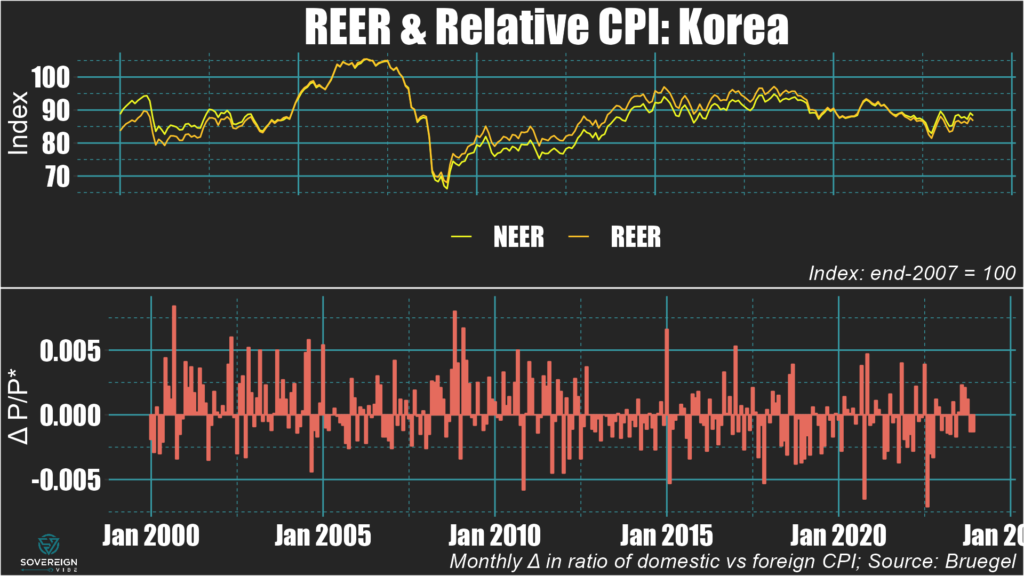

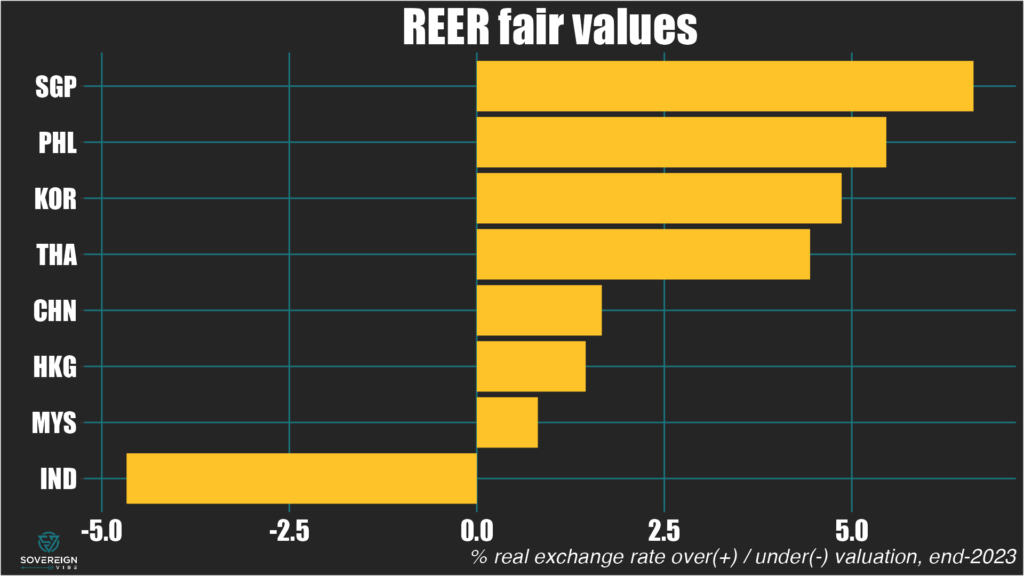

FX fair value estimates for eight EM Asia economies point to more over- rather than under-valuation across the region…

…so the real depreciations registered by most of the region’s currencies last year has pushed many (but not all) towards fair value.

Inflation differentials are now playing a larger role in determining REERs compared to the pre-pandemic era.

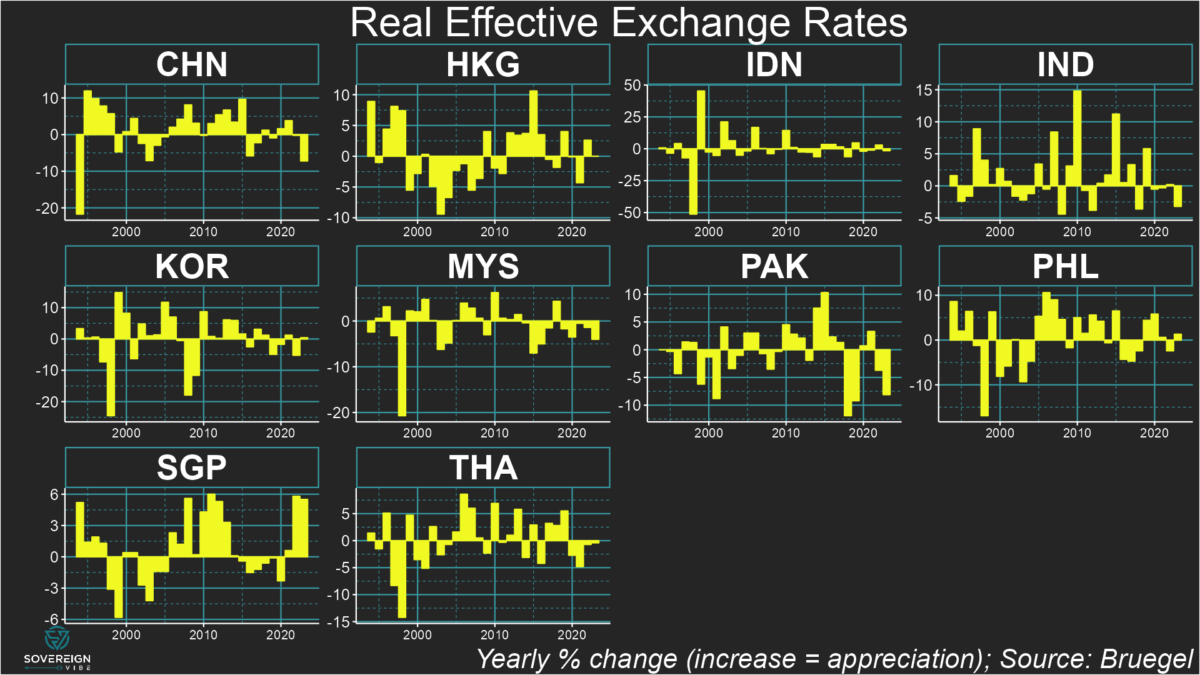

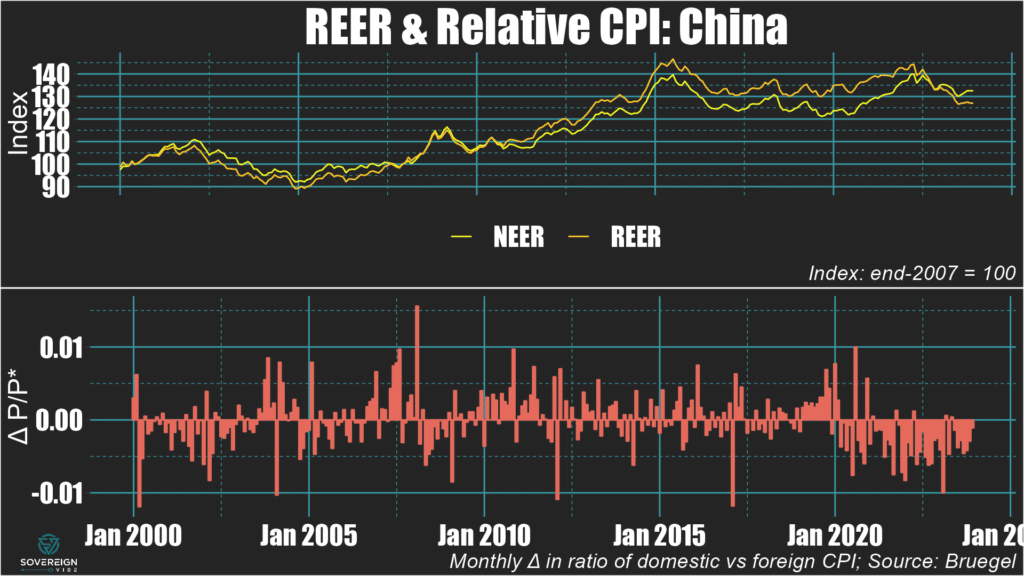

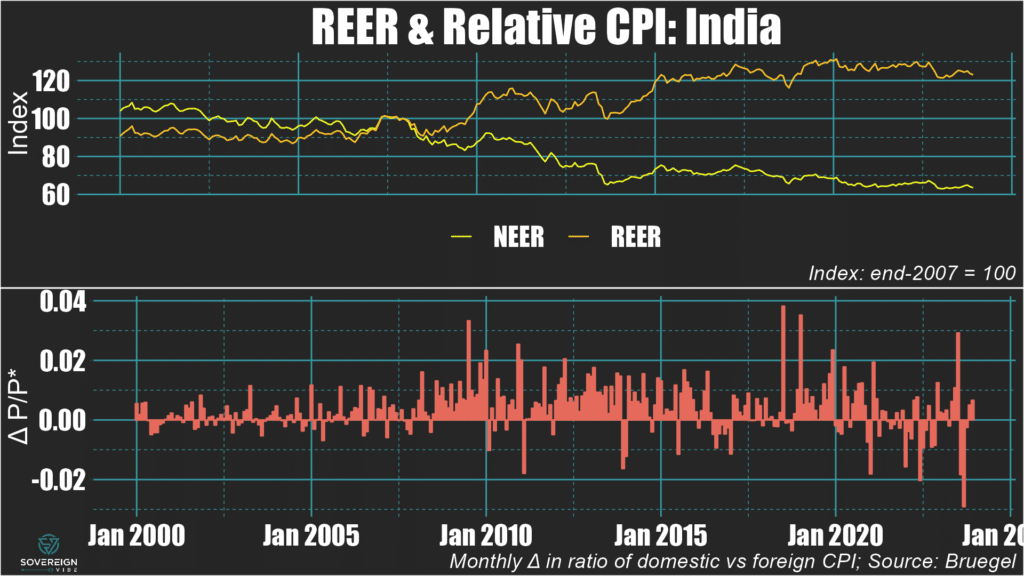

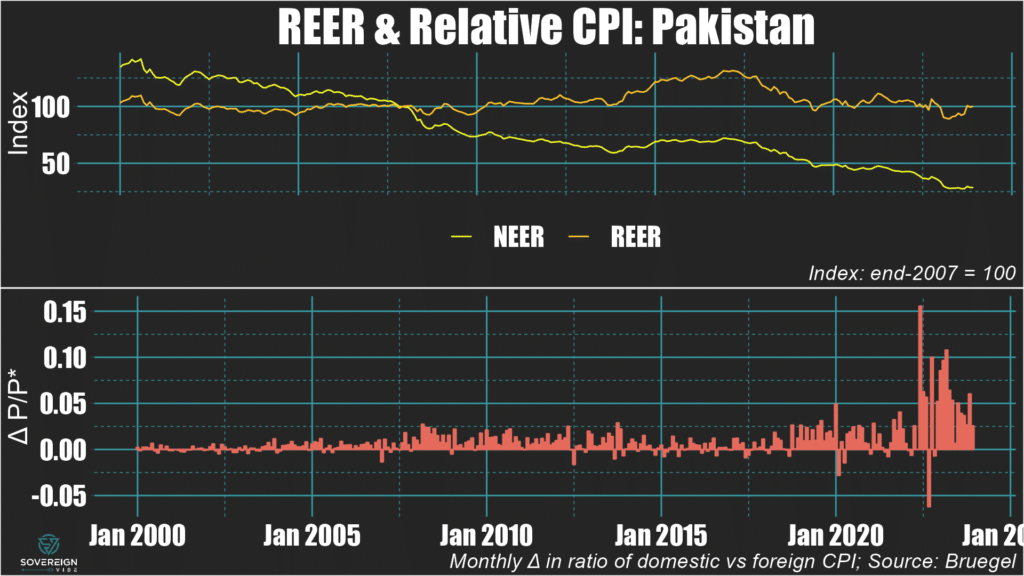

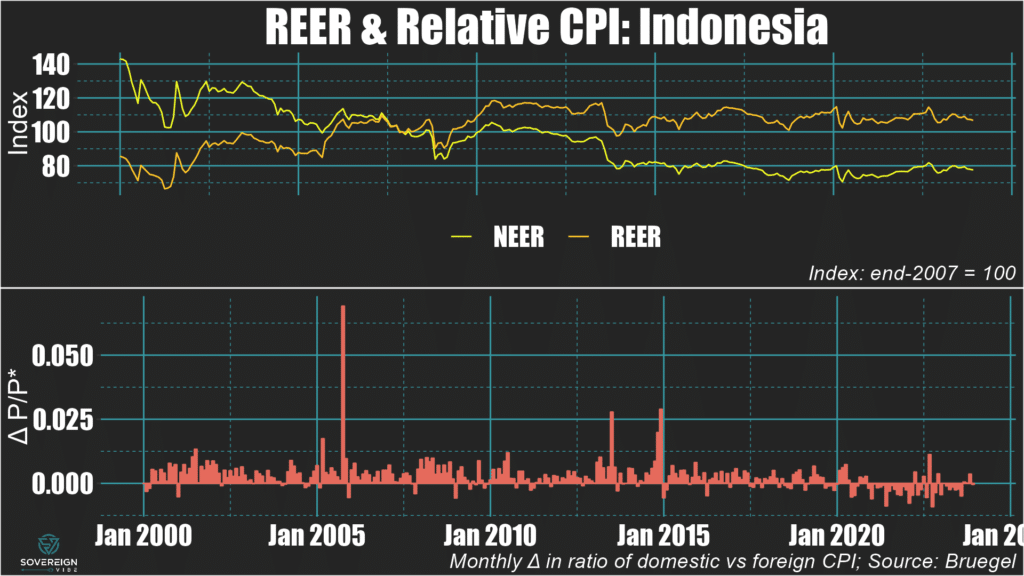

Currencies in emerging markets Asia mostly declined in real terms in 2023. Pakistan registered the sharpest real exchange rate depreciation, though China also weakened significantly on the back of much less inflationary pressure in the country relative to its trading partners.

REER trends in EM Asia

Of the eight EM Asia countries covered below, only the Philippine peso and Korean won strengthened in real terms in 2023, though the Singaporean and (possibly) Hong Kong dollars were also in positive territory for the year.

For each country, I provide a chart that breaks down the contributions of to the real exchange rate:

The nominal effective exchange rate: Remember that “effective” implies a trade-weighted calculation against all trading partner currencies.

Inflation differentials: This indicator looks at the month-on-month changes of the ratio of the domestic country’s consumer price index versus the trade-weighted CPIs of its trading partners. A positive (negative) differential means that the domestic country is experiencing higher (lower) inflation than its trading partners are.

As for fair values, those are covered in the next section of this post.

🇨🇳 China: The yuan depreciated by around 7.5% in real terms in 2023, on the back of two years of mild appreciation. Despite some nominal weakening, it is mostly inflation differentials driving the real depreciation, as deflationary pressures in the Middle Kingdom stand in marked contrast to the rising prices experienced by its trading partners in recent years.

🇮🇳 India: The rupee experienced a real depreciation of about 3% in 2023 against its trading partners. Comparatively low inflation and some nominal currency weakening in H2 were both at play.

🇵🇰 Pakistan: The rupee declined by around 8% in real terms in 2023, following a smaller drop the previous year. The decrease in nominal effective terms was even larger, as inflation in Pakistan was higher than that of its trading partners for the entire year.

🇮🇩 Indonesia: The rupiah’s real exchange rate was fairly stable in 2023, registering a very modest decline in real and nominal terms alike. Inflation differentials were small and alternated between positive and negative over the course of the year, so had a negligible effect.

🇲🇾 Malaysia: The ringgit depreciated by nearly 5% in real terms over the course of 2023, with both nominal weakening and negative inflation differentials contributing.

🇵🇭 Philippines: The peso is one of the few currencies in this selection of EM Asian countries to have experienced a real appreciation in 2023, alongside the Korean won and Singaporean dollar. This modest real appreciation was driven by nominal strengthening and a positive inflation differential.

🇹🇭 Thailand: The baht weakened very modestly in real terms in 2023, mostly as a result of a negative inflation differential, while trading flat in nominal terms.

🇰🇷 South Korea: The won’s real exchange rate strengthened slightly in 2023, mirroring the nominal dynamic, with any inflation differential with trading partners close to zero.

Fair Value REERs

In EM Asia, Singapore, the Philippines, Korea, and Thailand appear most overvalued.

China, Hong Kong, and Malaysia are also in positive territory. However, China’s current account is likely much larger than reported, suggesting that the yuan is almost certainly undervalued.

In contrast, the Indian rupee appears to be about 5% below fair value.

The sample of countries will be expanded in further updates of this analysis.

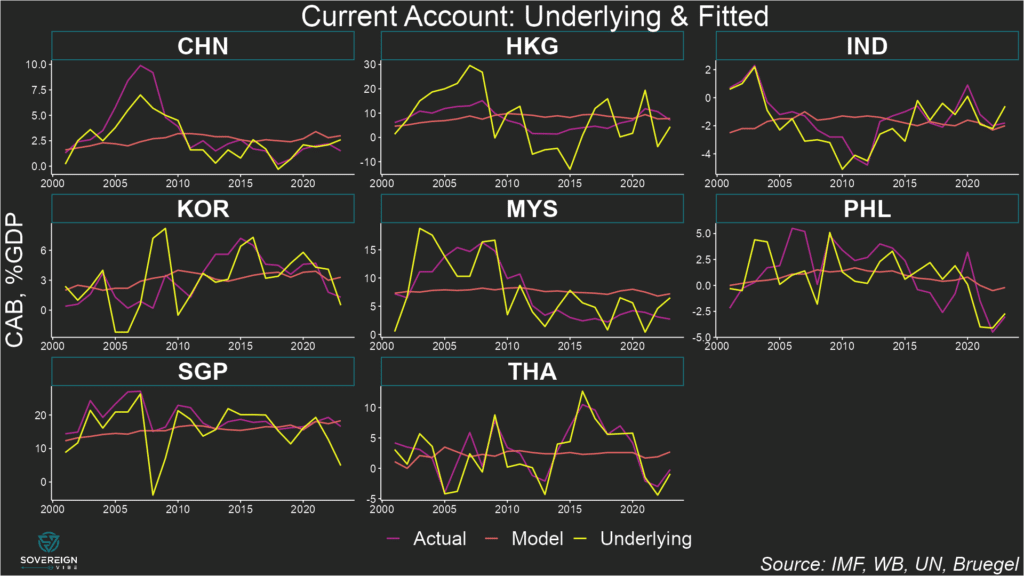

Underlying & Equilibrium CABs

The chart below shows actual, underlying, and equilibrium current account balances. When the underlying CAB is below the modeled equilibrium, the currency is overvalued in real terms. The percentage amount of over- or under-valuation of the currency is the percentage of real depreciation or appreciation needed to move the underlying CAB to equilibrium. For example:

The Philippines’ underlying CAB is well beneath equilibrium, suggesting overvaluation. The peso would need to depreciate by about 5% in real terms for the underlying CAB to rise to equilibrium level.

India’s underlying CAB is above the estimated equilibrium implied by the model, pointing towards undervaluation. The rupee would need to undergo real appreciation of around 5% to decrease the underlying CAB to equilibrium.

Readers should note that countries with high ratios of imports and exports as a share of GDP have CABs that are more sensitive to REER misalignment.

In other words, seeing where and underlying CAB stands in relation to equilibrium reveals where a currency is over- or under-valued, but not the magnitude of the divergence from fair value.

Today marks the grim anniversary of Russia’s full-scale invasion of Ukraine on February 24, 2022. Yet the conflict since 2022 is in many ways larger than the current military operations on the ground, both in terms of time and space. It is of course only the latest and most intense iteration of Russian aggression in the country, which started in earnest in 2014 with Russia seizing Crimea and launching military operations in the Donbas under the pretext of supposed separatism.

Spatially, events in Ukraine have global implications for geopolitical competition between the West and Russia, along with its allies of convenience – chief among them China but also pariahs such as North Korea and Iran. In tandem with the Covid-19 pandemic, the 2022 war in Ukraine marks the end of an era: the second of two death knells of the post-Cold War period.

Macroeconomic snapshot

Beyond the immense human toll, social disruption, and infrastructure destruction, the macroeconomic effects on Ukraine since 2022 have also been tremendous, obviously. The budget deficit went from a respectable -3.7% of GDP in 2021 to a gaping hole of nearly -30% in 2022, and possibly -20% in 2023. In 2024, the government’s shortfall is projected to reach $43 billion, which is probably equivalent to around a quarter of GDP.

Similarly, output dropped by about a third in 2022, with little in the way of recovery in 2023.

Output gaps have swung wildly in Ukraine since its independence. In percentage of potential GDP, IMF World Economic Outlook October 2023 data indicate:

These swung from positive double digits in 1992-1993 to negative double digits for the rest of that decade.

Actual output finally rose above trend in 2004, with the cycle accelerating until the global financial crisis forced a contraction in 2009.

Growth was recovering through 2013, until in 2014 Russia seized Crimea and began a covertly-led irredentist proxy war in Ukraine’s Donbas region. The output gap dropped to -10% in 2015.

From 2016 output rebounded again until the pandemic dampened activity in 2020, followed by a swift recovery to 2019 levels in 2021.

Since Russia’s full-scale invasion in February 2022, the output gap has once again plummeted, to -15% that year and to -10% in 2023.

Deglobalization, reglobalization, or slowbalization?

To be sure, deglobalization began at least as early as 2016, as that year saw the election of Donald Trump; the ensuing tensions with China and Iran; and Brexit. Global fragmentation has only worsened in the years since, with Covid; Ukraine and the related sanctions; and Joe Biden continuing Trump’s trade protectionism.

The world has now entered a new period in which countries are reconfiguring their trading relationships and supply chains in reaction to heightened geopolitical tensions, logistical frictions, and increased barriers to the movement of people and goods. The world’s borders have hardened, so cross-border movement is less fluid.

Hence the terms “deglobalization,” “reglobalization,” and “slowbalization,” though none of these encapsulates the nuances of what is happening. There is even evidence that international trade has rebounded strongly since the pandemic and that geopolitical alignment doesn’t explain much when it comes to international trade.

Still, the rafts of Ukraine-related sanctions; pandemic-related travel restrictions and supply chain disruptions; and trade reconfigurations such as “friend-shoring” or “near-shoring” are leaving their mark and, to a large extent, appear to have staying power. This is part of the reason I named this blog Sovereign Vibe.

21st-century global “stewardship”

It should come as no surprise that I, like Ukrainians and most of my fellow Westerners, consider the Kremlin to be at fault for the ongoing hostilities in Ukraine. Indeed, the Russian government is clearly responsible for seizing Crimea in 2014, jump-starting a war in the Donbas that same year, and fully invading the country in 2022. There are no legitimate justifications whatsoever for this aggression, Moscow’s propagandistic claims notwithstanding.

Yet the war in Ukraine is also symptomatic of Western, and chiefly American, failures in responsible global stewardship. Supporting Ukraine and opposing Russia is important in seeking an optimal outcome from a Ukrainian and Western point of view but provides no path forward on managing relations with Russia in the future.

The point is that there never should have been a war in Ukraine from 2022, or from 2014 for that matter. The heart of the problem is Russia’s revanchism under Vladimir Putin, which itself is an outcome in reaction to the Soviet collapse and ensuing chaos in Russia and the other newly-independent remnants of the USSR. This seems like an obvious point, but none of this was pre-ordained.

Geopolitical lessons

While authoritarianism under Putin is an outcome shaped almost exclusively by forces within Russia itself, the West missed a crucial opportunity in the 1990s to incentivize an erstwhile opponent into becoming an ally, much as visionary American and Western leadership did with Germany and Japan post-WWII. Although the USSR was not defeated militarily, observers should at the very least be able to imagine a post-Cold War order where Russia plays the role of a neutral cooperator, rather than an autocratic kleptocracy bent on geostrategic spoliation.

Shock therapy à la Dick Cheney

Western policy towards Russia failed miserably in the 1990s on at least two occasions. The first is in the immediate aftermath of the Soviet collapse, when Jeffrey Sachs and other Western economists advised the Russian government to adopt rapid market reforms, privatizations, and liberalization policies, known as “shock therapy.” Crucially, these advisors saw the need for significant Western aid to accompany these reforms, much as the Marshall Plan had helped Western Europe rebuild after WWII.

However, Dick Cheney, who was the US Secretary of Defense at the time, successfully pushed for shock therapy to be adopted without the aid. The predictable result was that, in the 1990s, Russia – and Ukraine as well as other former Soviet republics – suffered an economic and industrial collapse, a weakening of already-fragile institutions, a rise in poverty, and the emergence of robber barons who came to dominate the country’s politics.

“Dermocratia”

The second mistake of Western policy towards Russia flowed from the first. By the time Boris Yeltsin was up for re-election in 1996, Russian voters had become disenchanted with the economic suffering under the country’s new market economy and nascent democratic institutions. So much so that the term “dermocratia” was popularized, as a play on the words “democratia” and “dermo,” which mean “democracy” and “shit” in Russian, respectively.

Needless to say, Yeltsin was facing an uphill battle, but he had the support of the oligarchs, who were in fact more powerful than he was. Notably, Western governments also hoped to see him re-elected, as the chief opposition came from the Communist Party of the Russian Federation, which in some ways was the ideological successor to the Soviet leadership that had for so many recent decades been the US’s strategic foe.

To make a long story short, the election was marred by many irregularities, without which the communists might well have prevailed. Western capitals conveniently turned a blind eye to this meddling, further weakening the legitimacy of democratic institutions in the eyes of ordinary Russians.

No apologies

These Western mistakes in the 1990s are in no way an excuse for the authoritarian turn that Russia has taken under Putin. The Russian leadership alone is responsible for this outcome. Nor is the West somehow at fault for Russian aggression in Ukraine, Georgia, or beyond as a result of NATO expanding its European membership eastwards to countries willing to join of their own accord, as Putin apologists such as John Mearsheimer or Stephen Cohen claim.

But certainly American leadership in the 1990s under Bush and Clinton lacked the vision to try to bring Russia onside in the way that their more illustrious predecessors had done with Germany and Japan in the aftermath of WWII. Let this be a lesson for the future, as the West tries to imagine what Russia’s role in the world can and should be.

As tempting as it is to wish that Russia is a problem that would just go away, it won’t. Only by working backwards from “what good looks like” regarding Russia can Western leaders hope to address the root cause of the war in Ukraine, which is Russia’s revanchist position as international spoiler.

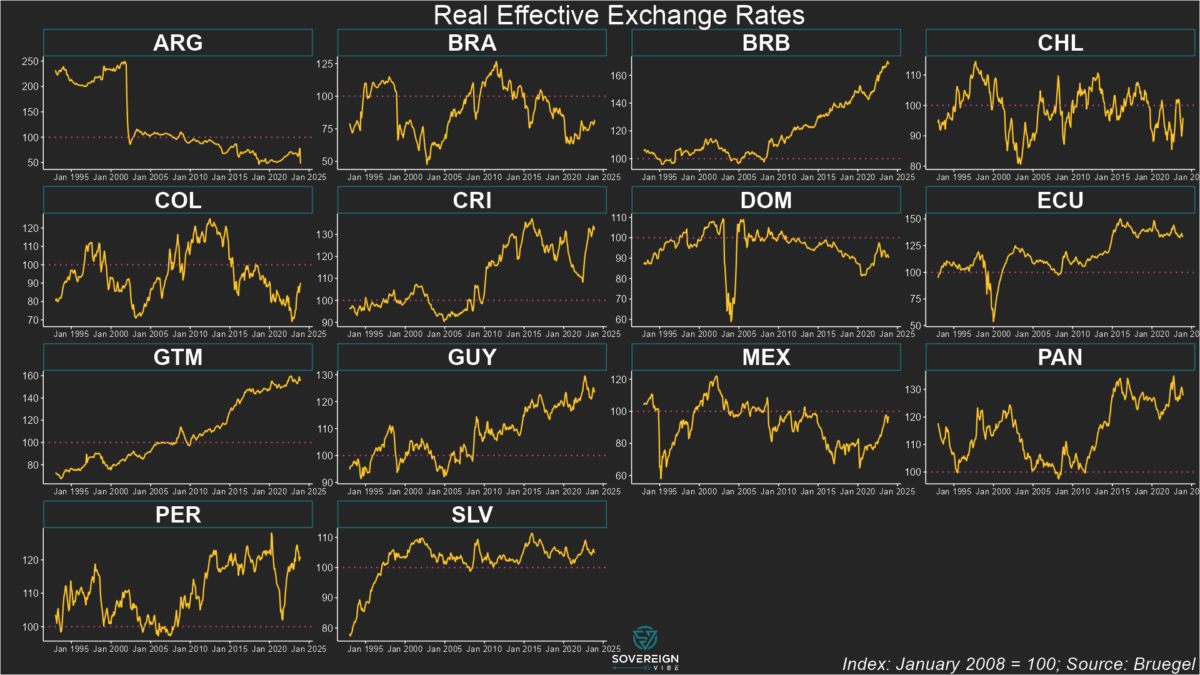

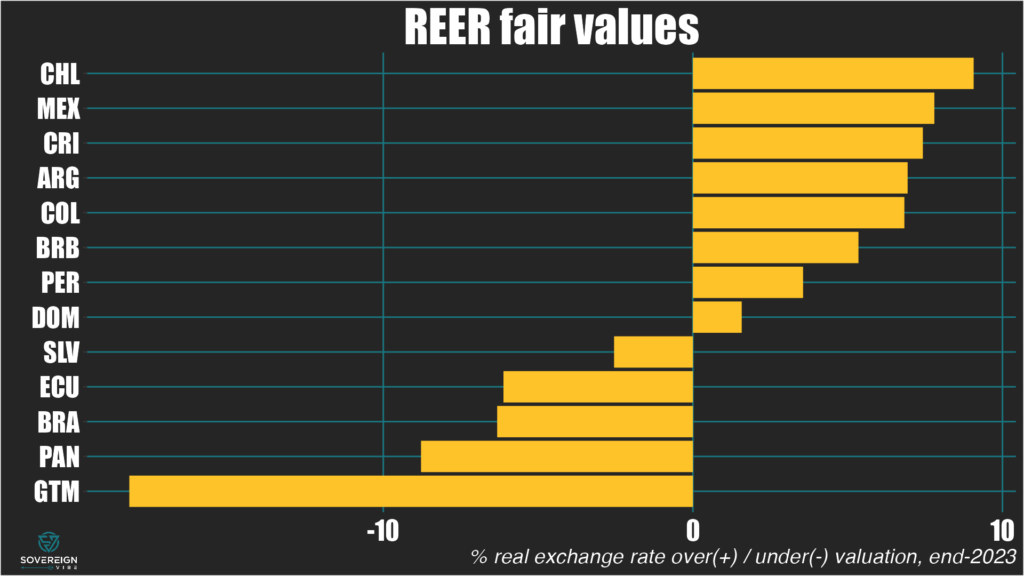

FX fair value estimates for 13 economies across LatAm at end-2023 underscore the idiosyncrasies of recent current account dynamics in the region…

…while also highlighting V- and L-shape nominal performance against USD since the pandemic in several countries,…

…even as the inflationary spike in ~2022 continues to abate across the main economies covered below.

As in other parts of the world, several Latin American economies saw their real exchange rates weaken during the pandemic only to rebound sharply amid the global inflationary shock. This v-shape trajectory of LatAm REERs is most evident in Peru and Costa Rica but is also visible to varying extents in Brazil, Colombia, the Dominican Republic, Mexico, and Panama.

REER trends in LatAm

In nominal terms against the dollar, the main currencies in the region weakened during 2020 before strengthening to varying degrees in the years since. Inflation was generally around the 2% mark in these economies in 2020 before peaking in 2022:

🇲🇽 Mexican peso: after dropping sharply during the early pandemic, the peso had mostly recovered by early 2021 and traded flat until October 2022. Since then, it has strengthened significantly, despite some wobbles circa October 2023. Inflation rose from 2% in 2020 to ~8.5% in 2022 before declining to the 4-5% range in 2023/Q1 2024.

🇧🇷 Brazilian real: weakened significantly in H1 2020 and has traded between flat and very moderate strengthening since. Inflation rose from 2% in 2020 to 12% by early 2022, and has remained mostly in the 4-6% range since late 2022.

🇨🇴 Colombian peso: a sharp drop in March 2020 before almost recovering by the end of the year. Then steady weakening until June 2022, when it dropped sharply, followed by a strong recovery throughout 2023. In early 2020, inflation stood at 4% but declined to sub-2% that year, before beginning to rise in H1 2021, culminating in a peak above 13% in late 2022/early 2023 and since declined to the 8-10% range.

🇨🇱 Chilean peso: came under pressure in March 2020 but only after having experienced a sharper drop in late 2019, so its decline during the pandemic coincided with a pre-existing weakening trend. By May 2021 it had more than recovered the early-pandemic weakness, then steadily weakened to October 2022. Subsequently, it bounced back in mid-2023 before declining again. Inflation hovered in the 2-4% range in 2020 before beginning a long steady rise from 2021 onwards, peaking at 14% in 2022 and declining to circa 4% by end-2023.

🇵🇪 Peruvian sol: a steady, significant decline from early 2019 to September 2021, followed by flat-to-moderate strengthening. Inflation stayed around 2% throughout much of 2020 before rising to around 8.5% in H1 2022, and then beginning to moderate in H1 2023, dropping to below 4% by the end of the year.

Regarding fair values, the broad REER trends described above don’t really shed that much light, as valuations depend on where underlying current account balances stand in relation to equilibrium.

Fair Value REERs

In LatAm, Chile, Mexico, Costa Rica, Argentina, and Colombia appear most overvalued, while Guatemala, Panama, Brazil, and Ecuador seem most undervalued.

In this sample, the Dominican Republic and El Salvador are closest to fair value. Peru’s overvaluation is also relatively small.

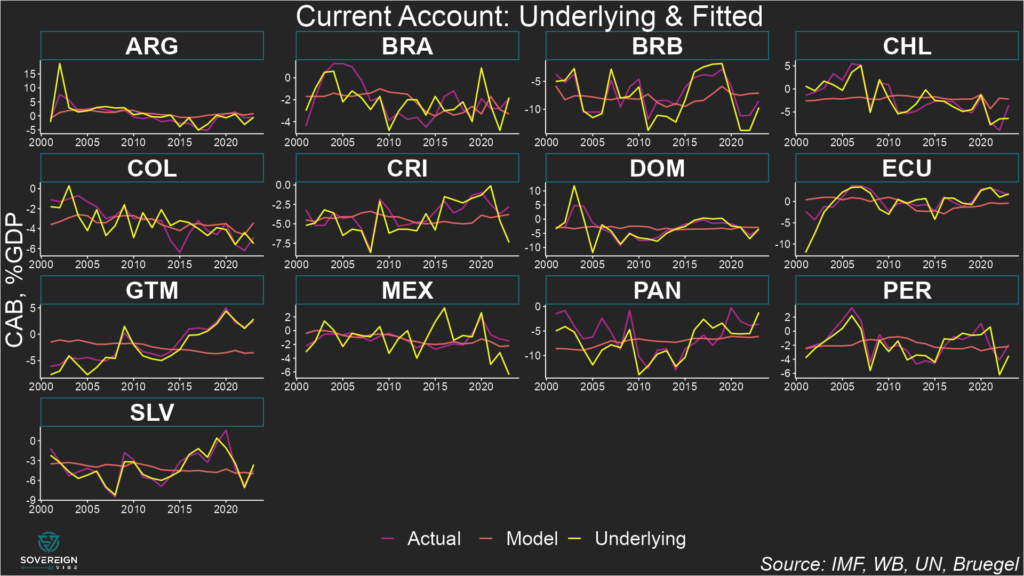

Underlying & Equilibrium CABs

The chart below shows actual, underlying, and equilibrium CABs. When the underlying CAB is below equilibrium, the currency is overvalued in real terms. For example:

Chile’s underlying CAB exhibits a significant drop-off, with the headline CAB also being below equilibrium.

Mexico’s underlying CA deficit is even deeper in the red at around -6% of GDP, well below equilibrium.

Conversely, when underlying CABs are above estimated equilibria, the currency is undervalued in real terms. For example:

Guatemala exhibits a CA surplus of around 2.5% of GDP, about 5 percentage points above its estimated equilibrium.

Panama’s CA deficit is above its estimated normal level, which is quite low at around -7% of GDP and explained by some of the unique characteristics of the country’s economy.

Brazil has registered some large swings in its underlying CAB in recent years, meaning that the real has alternated between over- and under-valuation.

Readers should note that countries with high ratios of imports and exports as a share of GDP have CABs that are more sensitive to REER misalignment.

In other words, seeing where and underlying CAB stands in relation to equilibrium reveals where a currency is over- or under-valued, but not the magnitude of the divergence from fair value.

Stay tuned for more currency fair values in Asia and beyond.

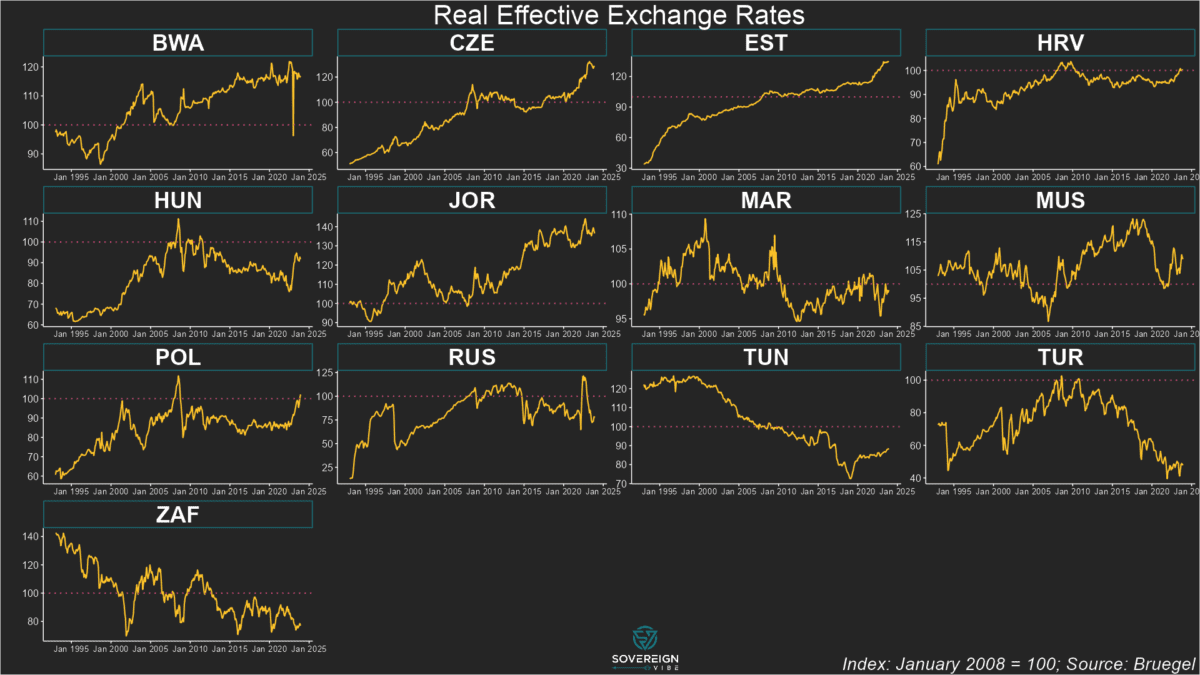

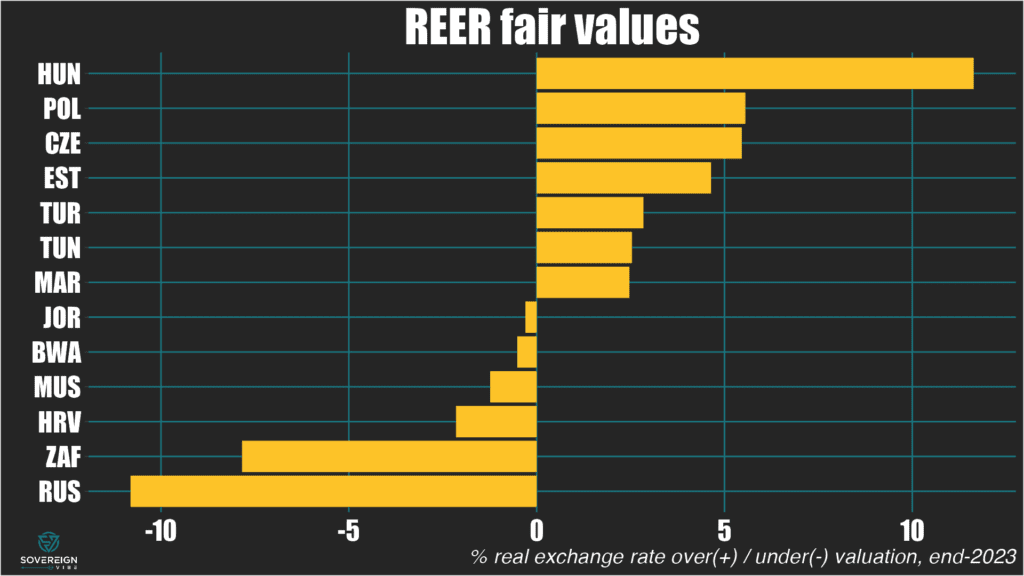

FX fair value estimates for 13 economies across CEEMEA at end-2023 underscore the impact of the war in Ukraine.

Real effective exchange rates spiked in various countries following the successive pandemic-Ukraine shocks…

…although Morocco and Croatia appear to be bastions of REER stability in an otherwise volatile group.

One way to value a currency is to assess the link between current account balances and real effective exchange rates, which merge the nominal exchange rate with the ratio of domestic to trade-weighted foreign prices. The IMF uses a fair value model that compares “equilibrium” to “underlying” CABs, with any difference a result of REER misalignment. FX fair values are presented below.

REER trends in CEEMEA

Several economies in Central & Eastern Europe, the Middle East, and Africa have experienced real exchange rate appreciation in the past few years. The dual pandemic-Ukraine inflationary shock since 2021-2022 is in large part responsible for this: annualized inflation remained in double digits in the Czech Republic, Hungary, Poland, Estonia, and Croatia until early- to mid-2023.

Moreover, the Czech koruna, Hungarian forint, and Polish złoty all weakened significantly in nominal terms in 2022, but inflation was so strong that these REERs still rose that year. In 2023, REERs in these countries continued to climb while the koruna traded flat and the forint and złoty registered modest nominal gains.

Russia saw yearly inflation fall from ~11% at the beginning of 2023 to the 2-3% range in Q2 before rising to ~7% by year end, while the ruble weakened significantly, resulting in REER weakening.

South Africa experienced declining inflation and a minor depreciation of the rand in 2023, albeit on the back of significant currency weakening since mid-2021, causing the REER to slide.

Turkey remains an inflationary basket-case, having spent almost all of 2023 near or above 50% in annualized terms, resulting in the lira’s ongoing decline. The net effect has been for its REER to move sideways – but after many years of secular decline.

Turning now to fair values, a number of REERs in CEEMEA exhibit significant over- or under-valuation.

Fair Value REERs

In CEEMEA, Hungary, Poland, and the Czech Republic appear most overvalued, while Russia and South Africa seem most undervalued.

It should come as no surprise that Hungary’s REER is overvalued, on the back of high inflation and (very modest) forint strengthening last year. But the real driver is that Hungary is running a massive underlying current account deficit at -15% GDP (see chart below).

Similarly, it also makes sense for Russia to be undervalued given the weaker ruble and moderating inflation. Its underlying CAB being above its equilibrium CAB confirms this is the case.

The same reasoning applies to South Africa: depreciated rand, lower inflation, and underlying above equilibrium.

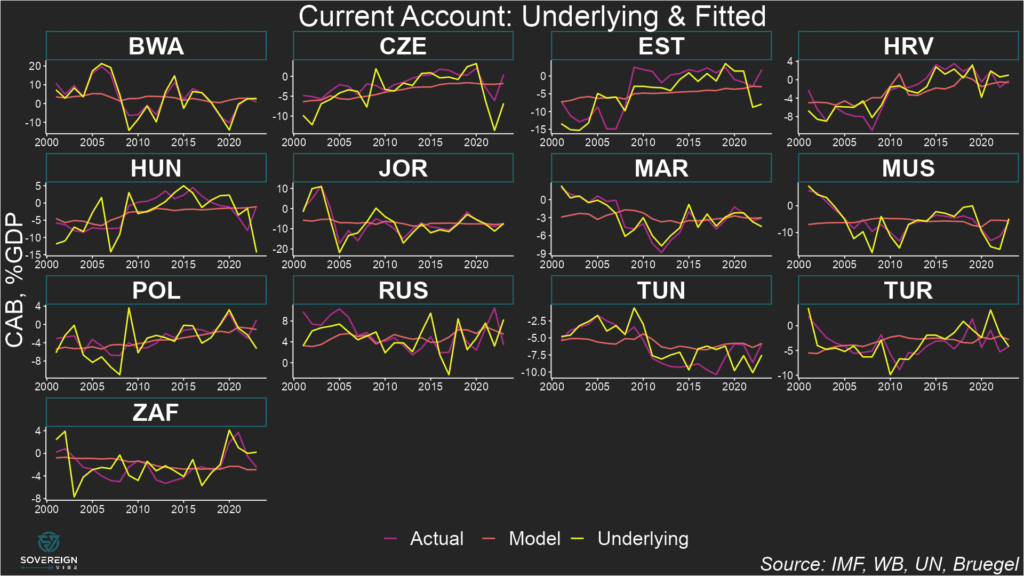

Underlying & Equilibrium CABs

When the underlying and equilibrium current account balances are equal, the real effective exchange rate is at fair value.

If the equilibrium CAB is above (below) the underlying CAB, then the REER is over- (under-) valued.

In the chart below, the fitted estimates of current account equilibria are labeled as “model” and are shown alongside actual and underlying CAB readings.

Countries with high ratios of imports and exports as a share of GDP have CABs that are more sensitive to REER misalignment. Turkey and Tunisia provide an example of different sensitivities. In the chart, in 2023 both look overvalued, as equilibrium is above the underlying CABs.

The gap between Turkey’s equilibrium and underlying CAB is smaller than that of Tunisia, yet Turkey’s REER is more overvalued than Tunisia’s, as depicted in the fair values chart above. This is because Turkey’s economy is more open than Tunisia’s, hence REER misalignment has a greater impact on its CAB.

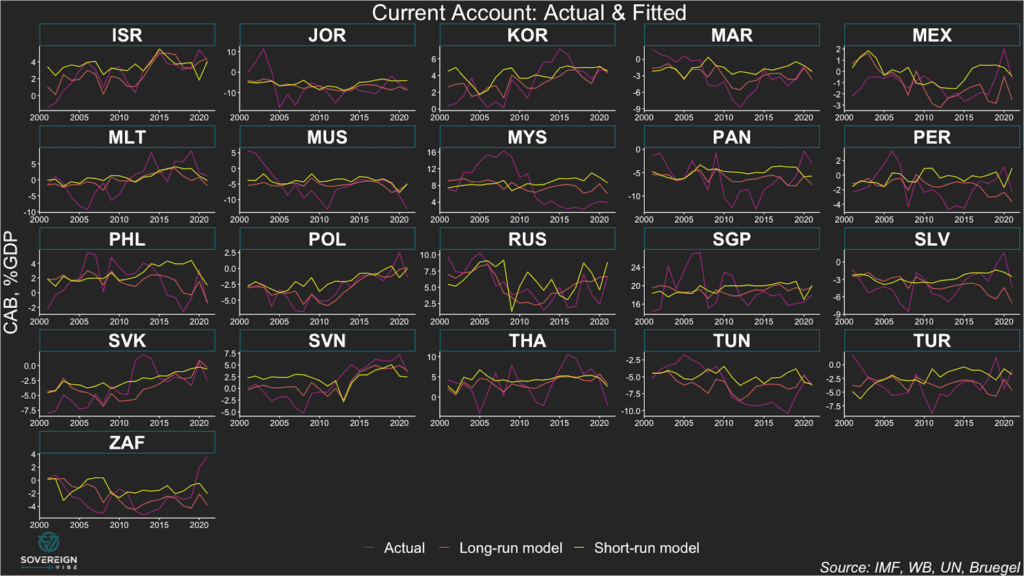

Following on from my estimates of current account equilibria in advanced economies, here I turn to emerging markets, which is after all the focus of this blog. I initially focused on AEs in an attempt to replicate as closely as possible an IMF empirical investigation of current account balances in this set of countries, as doing so is more methodologically prudent before expanding the analysis to EMs.

The goal of this work is to understand what a country’s current account balance should be (see my previous post for a breakdown of what CABs are), based on relevant characteristics as identified by the IMF in its model. These include the cyclically-adjusted government budget balances, demographic dependency ratios, and income level, which are all variables that tend to change only gradually over time. As such, they can be thought of as “long-term” variables, especially the latter two, which can be useful in trying to conceptualize where a country’s CAB ought to be.

In contrast, cyclical variables that are more volatile from year to year, such as real exchange rates, terms of trade, and domestic output gaps, as well as fiscal policy, theoretically should do a better job of predicting observed CAB readings. These can be thought of “short-term” variables, although I use the same fiscal variable in both the long- and short-run models.

The “long-run” model fitted values in these charts are the closest approximation I have now for current account equilibria in these EMs. But my confidence in these results is low and will require additional work, for the reasons described below.

Regretfully, I am far from satisfied with the results of this work so far, but have chosen to publish these interim conclusions in the interest of maintaining regular engagement with my audience. Worse still is that I had to exclude important EMs such as Indonesia from the analysis to maintain a balanced panel dataset, as data availability for some indicators didn’t go far back enough in time.

The good news is that both models have overall statistical significance and that each of the regressors in the short-run model is statistically significant.

Short-run model results

I’d still like to tweak the short-run model by adding a trade-weighted foreign output gaps as an independent variable and replacing the cyclically-adjusted budget indicator with a non-cyclically-adjusted budget variable. But, overall, I’m fairly content with the short-run model, as the fiscal, terms of trade, and real exchange rate regressors all behave as expected in relation to the CAB.

For methodological reasons, I dropped the lagged dependent variable that featured in the short-run AE model, which has decreased the R2 readings in this short-run EM model, though I don’t see this as much of a problem.

Surprisingly, the domestic output gap is not negatively-related to the CAB but exhibits a positive, strong, and significant association. A positive output gap, meaning that economic growth is above-trend, often results in increased imports, thus placing downward pressure on the CAB. And this is indeed what I found in the short-run model for AEs: a negative, strong, and significant relationship.

Perhaps the reason behind the positive output gap-CAB relationship in EMs is to be found in exports as a common driver: strong exports could lead to a higher output gap and a higher CAB. Many EMs rely heavily on exports for economic growth, whether of manufactured goods, commodities, or services.

Short-run model variables

Deviation from the in-sample average of the general government cyclically-adjusted budget balance adjusted for nonstructural elements beyond the economic cycle, as a share of potential GDP. Countries with higher-than average government budget balances should be able to attract larger portions of global current account surpluses. This is confirmed by the positive coefficient at 1% significance.

Domestic output gap: actual output minus potential output in current USD (logarithmic difference). Economies in the boom phase of an economic cycle can experience strong import growth, appreciated exchange rates, and stronger remittance and primary income outflows, putting the current account under pressure. Unexpectedly, the coefficient is positive, and is also large and significant. Theoretically, exports could be a common driver of output gaps and CABs in EMs, as they are positively associated with both.

One-year change in the terms of trade, i.e. the ratio of the price of exports to the price of imports. The coefficient is positive and significant, as expected.

One-year change in the REER. The coefficient is negative and significant, as expected, because high REERs can lead to imports becoming relatively cheap, thus increasing import volumes, and lead to exports becoming relatively expensive, thus decreasing export volumes.

Regression Results – 41 Emerging Economies

Dependent variable:

Current Account Balance, %GDP

panel

coefficient

linear

test

(1)

(2)

random.shortrun

random.pcse.shortrun

sur_dev

0.439***

0.439***

(0.056)

(0.065)

ogap_usd.logdiff

15.920***

15.920**

(3.543)

(8.019)

tot_1d

0.061***

0.061***

(0.022)

(0.022)

reer_1d

-0.072***

-0.072***

(0.021)

(0.018)

Constant

-1.054

-1.054

(0.735)

(1.022)

Observations

861

R2

0.097

Adjusted R2

0.093

F Statistic

92.337***

Note:

*p<0.1; **p<0.05; ***p<0.01

Long-run model results

As for the long-run model, alas only two of its four independent variables are statistically significant after controlling for heteroskedasticity and autocorrelation: the budget surplus indicator and the old-age dependency ratio.

The child-age dependency ratio and income level were both statistically insignificant, as was the case in the advanced economy model. As such, in further work on this I will be discarding these two regressors and replacing them with something related to private savings. Doing so would complement the public savings approach already captured by the budget variable.

Moreover, the adjusted-R2 is laughably low in this model. While achieving a high R2 isn’t the most important consideration in constructing a good model with unbiased, efficient estimators, I’d still like to see something higher.

One other area of improvement for this long-run CAB model would be to run the independent variables against underlying CABs – which have the cyclical impact of output gaps stripped out and real exchange rate effects worked in – rather than against observed, actual CABs.

Long-run model variables

Deviation from the in-sample average of the general government cyclically-adjusted budget balance adjusted for nonstructural elements beyond the economic cycle, as a share of potential GDP. Countries with higher-than average government budget balances should be able to attract larger portions of global current account surpluses. This is confirmed by the positive coefficient at 1% significance.

The deviation from the in-sample average of the child-age dependency ratio on the 20-64 year-old working-age population, i.e. people 19 and under. I tested this variable on the intuition that the child dependency ratio could well be negative, not only due to the income effect as noted by Faruqee and Isard, but also due to the large amounts of consumption (which pushes down savings, increases imports etc) associated with children’s parents at the height of their income generation, family activities, and the associated demographic profile that such countries might have. In this two-ways fixed effects model it is insignificant when standard errors are controlled for heteroskedasticity and autocorrelation. It is also unexpectedly positive.

The deviation from the in-sample average of the old-age dependency ratio on the 20-64 year-old working-age population, i.e. people 65 and over. My intuition with this variable is that it would be positive because of the high level of savings that elderly people have, despite doubts as to the degree to which the elderly can generate positive savings flows for themselves. The sign was positive, as expected, a statistically significant.

Deviation from the in-sample average of GNI per capita on a PPP basis, adjusted for the country’s output gap to equate the observation to what it would be if the economy were running at potential. Unexpectedly, the coefficient is negative: theoretically, greater availability of income and thus savings opportunities in wealthier countries should lead to a higher CAB. Yet this result is insignificant in the long-run model.