Markets cautious on newly-elected President Dissanayake, renegotiations.

In one of Sri Lanka’s greatest political shake-ups in decades, this weekend’s presidential election saw the victory of neo-Marxist Anura Kumara Dissanayake ahead of the country’s two main, established parties.

With the political establishment now swept away, Dissanayake now faces the arduous task of consolidating the economic recovery and setting public finances on a sustainable, growth-inducing trajectory.

Political Thunderbolt

Markets have had a mixed reaction to Anura Dissanayake’s victory in Sri Lanka’s presidential election over the weekend.

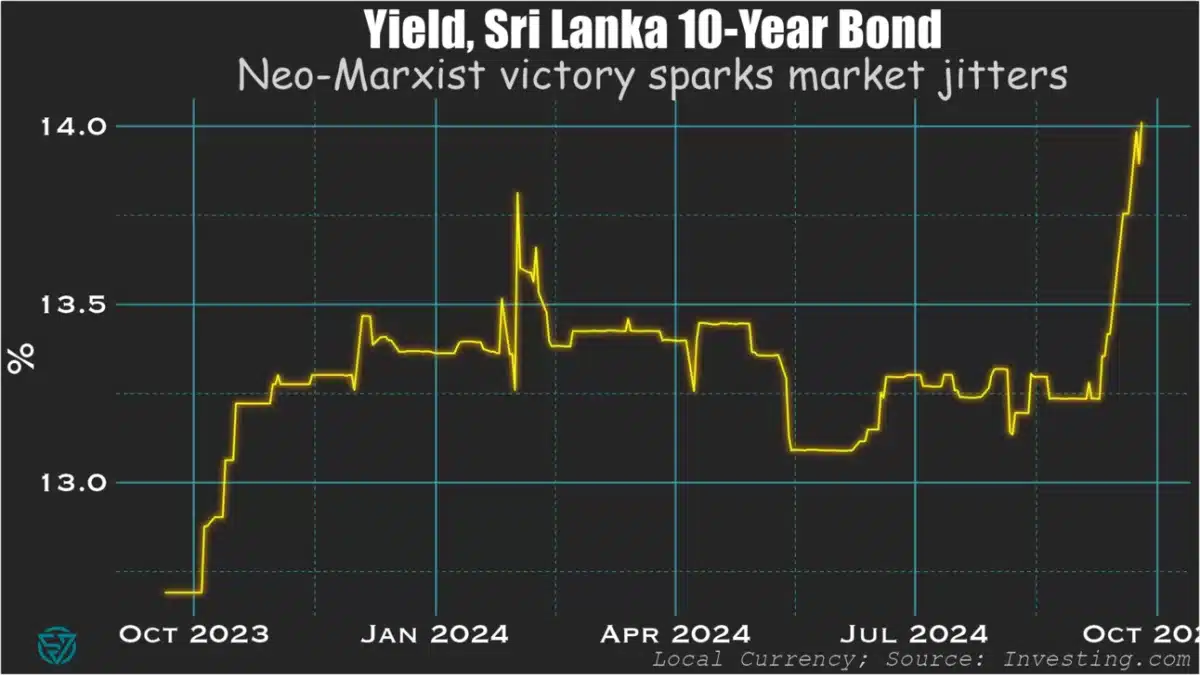

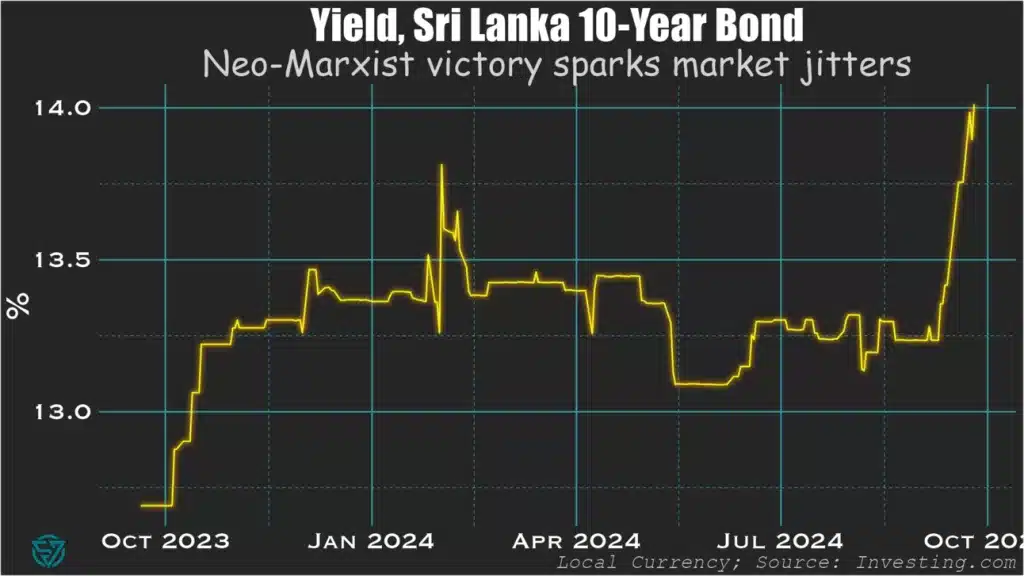

The bond market reaction has been fairly predictable for the election of a neo-Marxist, with Sri Lankan government yields sent soaring.

There are concerns that Dissanayake’s neo-Marxist leanings will lead to renegotiations of provisional debt restructuring deals and may even call some IMF conditionality into question.

Yields are also up over market uncertainty around how the new president and his party will govern, and whether that will threaten reform momentum.

The situation is fluid, with Dissanayake having dissolved parliament yesterday, where his party only holds three seats.

An End to Corrupt Rule?

There are some reasons to be hopeful. Local equities have been rising this week.

This could be related to the potential end to corrupt rule in the country and, with any luck, a pivot towards more transparent, inclusive governance and the stability that brings.

It’s easy to forget that what matters for governance is inclusivity, rather than focusing excessively on the left-right political spectrum.

The deeply-corrupt Rajapaksa dynasty was more market-friendly than Dissanayake on the surface.

But it was the endemic clientelism under their rule that led the country over the brink of default.

More than anything, this electoral result has been the repudiation of long-standing patronage networks.

As such, it should give investors hope for improved macroeconomic stability and public financial management.

If Dissanayake and his team manage to avoid measures that are excessively punitive for investors and businesses, including SMEs, brighter days may well be ahead for Sri Lanka and its stakeholders.

A Silver Lining to Renegotiations?

Moreover, there could be a silver lining to revising provisional debt restructuring agreements.

The bondholder deal is problematic as it is, as the macro-linked bonds will increase Sri Lanka’s future coupon payments if nominal dollar GDP rises beyond a certain threshold.

The macro-linked instruments are supposed to reflect strong growth.

But merely a strong currency appreciation that pushes GDP in nominal USD above the threshold, rather than rising output, could trigger the step-up.