It’s not just the usual suspects: some oil exporters also have low official reserves levels.

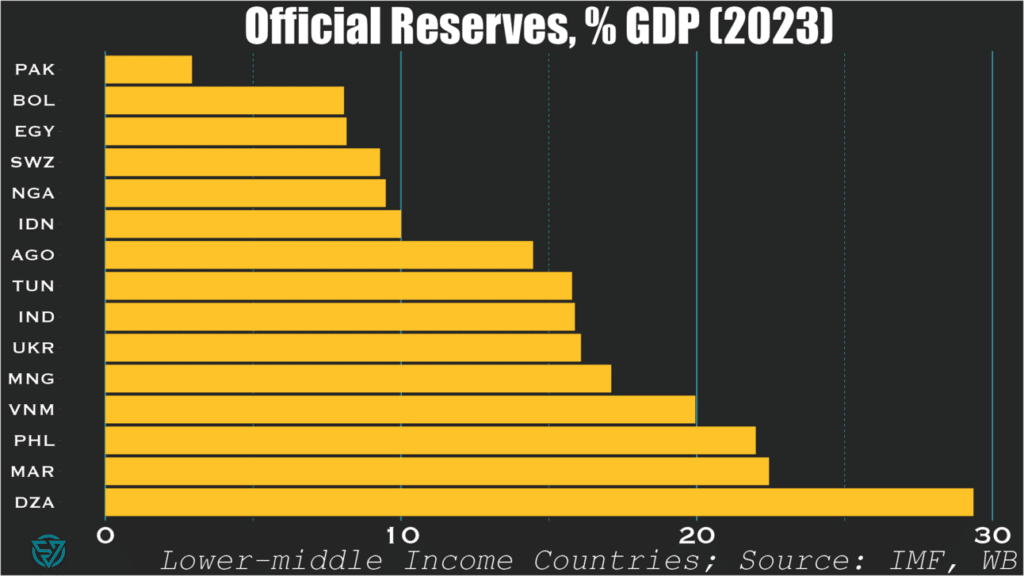

When writing last week’s piece on the IMF’s shoddy deal with Pakistan, I was blown away at the country’s astonishingly-low level of international reserves.

$9.5 billion for a $350 billion economy. That’s only around 3% of GDP and 1-2 months of import cover. Such a low amount of cash on hand isn’t exactly best practice, whether it’s sovereign, corporate, or personal finance.

So it got me thinking: is Pakistan really such an outlier? Or am I just crazy or ill-informed?

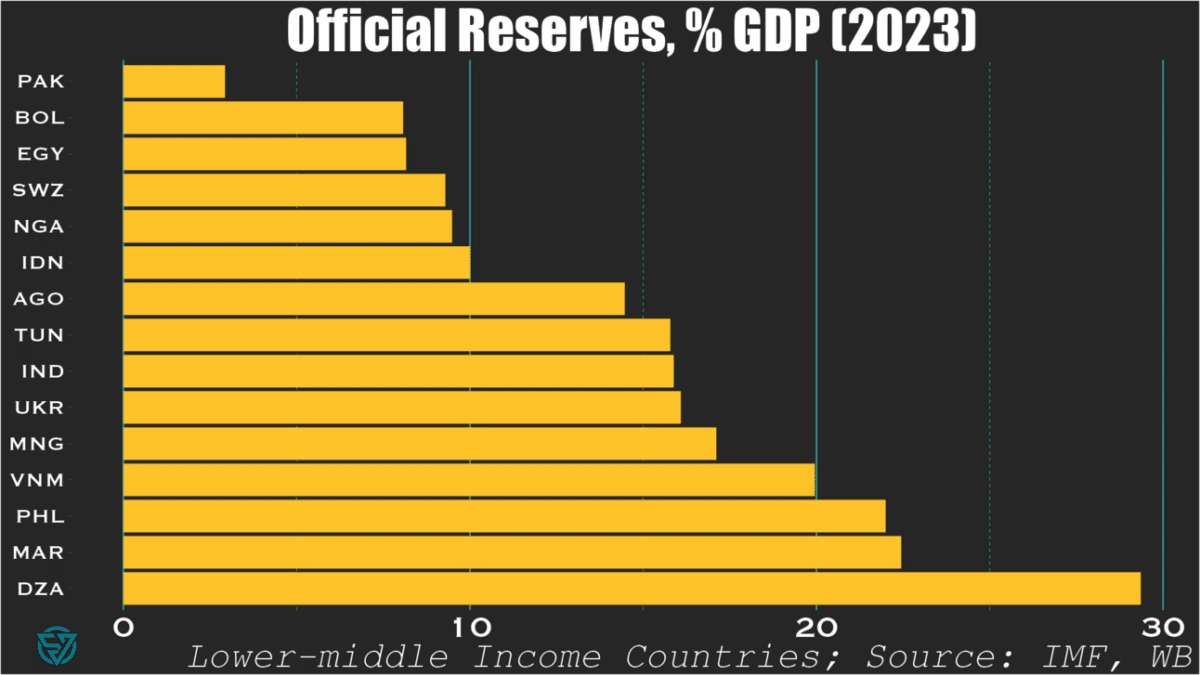

Lower-middle income countries

Turns out I was right: among countries in its income bracket, Pakistan has the lowest reserves-to-GDP ratio of all.

Bolivia, Egypt, Swaziland, Nigeria, and Indonesia are not far behind, at 10% or less.

Yet international reserves are far from the only macro indicator that matters of course. So I suppose we should be forgiving of Indonesia, which generally has much of its (macro) house in order.

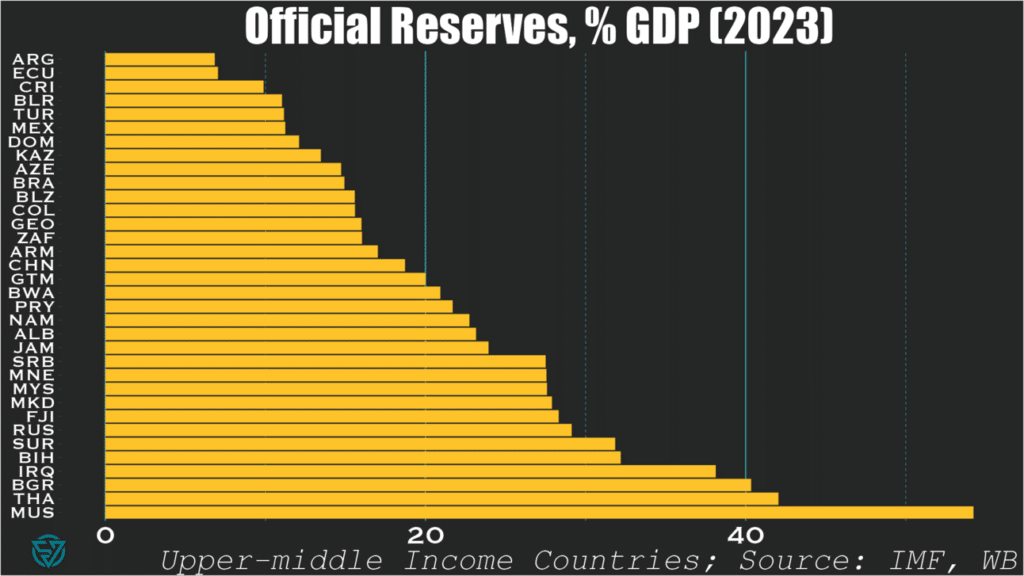

Upper-middle income countries

Looking at upper-middle income countries, only three in-sample are sub-10%: Argentina, Ecuador, and Costa Rica. I suppose Latin America really does have a savings problem.

As expected, these slightly richer countries generally exhibit higher reserve-to-GDP ratios than their poorer counterparts. No surprise there.

What is surprising, however, is to see oil-exporters like Azerbaijan, and Kazakhstan sub-15 percent.

Mexico, Brazil, and Colombia also produce oil and also have low ratios. But, then again, they are also Latin American…

“What’s the big deal?”, I hear you asking.

Well, Ukraine is a lower-middle income country fighting a war and undergoing debt restructuring. Yet Kyiv still manages to have more in the bank than wealthier countries with much lower-levels of security threats.

To me, that speaks volumes about economic management.