Emmanuel Macron wasn’t the only person traveling from France to Berlin last week: I was as well, to attend the inaugural Berlin Energy Forum on May 21st. Here are the key takeaways:

- First introduced in December 2022 and February 2023, energy sanctions are having mixed effects, but more can be done.

- Introduced in December 2023, the threat of secondary US sanctions against non-Russian financial institutions engaging in certain types of transactions with Russia are proving effective, as banks cut ties with Russian counterparts.

- The West missed a chance to devastate the Russian economy in 2022.

- Russia is in a very strong macroeconomic position right now, but this is coming at the expense of long-term growth, with the military-industrial complex using labor and resources at the expense of national development projects.

- Saudi Arabia and other Middle Eastern oil exporters are the big winners here.

Missed opportunity

The West had the opportunity to wreck the Russian economy in 2022, as its sanctions in response to the Russian military’s February invasion of Ukraine began to bite. But the sanctions had a limited effect because billions of Western money continued to flow into Russia as oil and gas payments. Putting money in an escrow account could have had a major impact.

Meanwhile, Russia’s central bank governor Elvira Nabiullina responded brilliantly in 2022 with large interest rate hikes, capital controls, and other FX restrictions. Moreover, Russia has been preparing since the 2014 sanctions by building up its shadow fleet of oil tankers ahead of time and by diversifying export routes, e.g. an oil pipeline to China.

Saudi Arabia and OPEC are playing an important role via keeping supply constrained and prices relatively high, benefiting Russia. Low-cost producers such as Saudi Arabia have more pricing power over the global oil market. So even if a higher-cost oil producer such as the United States could ramp up production immediately, the Saudis and other low-cost producers can still swing the market price by constraining supply.

Relevant sanctions actions

Western capitals only started applying energy sanctions against Russia nearly a year after the February 2022 invasion, with the crude oil price cap and embargo introduced in December 2022 and the oil products price cap and embargo in February 2023. The goal of these sanctions is to keep Russian oil volumes on the market, so that prices at the gas pump remain stable globally, while undermining Russia’s oil revenues via lower prices and fewer clients.

In December 2023, the US Treasury sanctioned 41 oil tankers comprising Russia’s shadow fleet, which has had an impact. However, enforcement has slowed in 2024, while Moscow has managed to add new vessels to the fleet.

Also in December 2023, President Biden issued an Executive Order to impose secondary sanctions on financial institutions engaging in transactions that violate the oil price cap or other sanctions against Russia. These have so far proven to be effective, as banks in China, the UAE, and Turkey limit payments to Russia and ask for increased compliance documentation from counterparties. These secondary sanctions were a top concern at the recent Putin-Xi summit in Beijing.

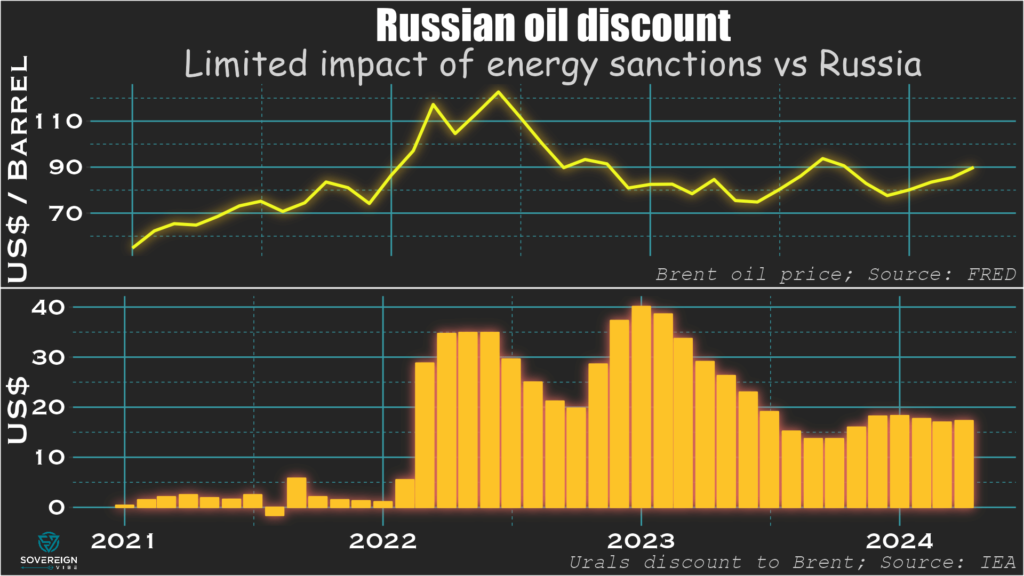

Discount on Russian oil

Everyone involved in Russian oil trade wants to be compensated for the risk of buying “tainted” product. The discount on Russian Urals oil rose in H1 2022 to $30-$35, as a geopolitical risk premium and had nothing to do with sanctions. This gradually declined as market players learned what they could get away with. This discount rose again from December 2022 as the crude price cap and embargo were first announced.

Each $10 of discount costs Russia $20 billion in export earnings if in place over the course of a year, so there is a tangible impact. But also consider the side-effects: the discount provides a subsidy to the buyer, e.g. China, India, Turkey, giving them an industrial advantage over Russia’s opponents.

The Western embargo worked because there is a discount on Urals, which Western countries used to buy, but none on Russian ESPO oil delivered from Siberia to China. It is clear that the $60 price cap on Russian oil hasn’t worked, as there are no two separate concentrations of transactions at $60 and the market price.

In the summer of 2023, Russia mobilizes its 41-strong shadow fleet, oil prices rise, and Russia’s discount drops. The US Treasury’s Office of Foreign Assets Control (OFAC) starts targeting the shadow fleet, so the discount starts rising again from end-2023. But OFAC stops enforcing these sanctions sometime in Q1 2024, so the discount hasn’t widened further. Part of the problem is that by the time governments sanction a vessel, it has been renamed and the company re-registered.

Three problems with energy sanctions on Russia

The first way to get around sanctions is violation. 29% of the Russian oil trade touches on G7 services, so 29% should be under the $60 cap. But only 2% is: the buyers are lying, which is attestation fraud. The buyers are no longer international oil traders but suspected subsidiaries of Russian companies recently registered in Dubai and in other jurisdictions.

The second is evasion. The shadow fleet now carries ~80% of Russian crude and ~50% of oil products, shares that have risen quickly in recent months.

The third hindrance is an unwillingness to disrupt access of Russian oil volumes to the global market. This is needed to wage economic warfare, but it is doubtful that G7 taxpayers would accept this. For instance, the US has given India unofficial clearance to accept Russian oil from ghost tankers as it doesn’t want the market to be too tight.

A strong macro position in the short- and medium-term

Although the discount on Urals oil has caused Russia to lose some oil revenues, relatively high oil prices have made up for those losses. Russia’s oil export earnings and budget oil revenues haven’t declined. The budget deficit widened in Dec 2022-Feb 2023. But the larger deficit in early 2023 was partly because Finance Minister Anton Siluanov was front-loading expenditures to avoid an end-of-year surprise.

By summer 2023 Russia had started getting revenues from from new oil export machine to India after the long oceanic voyages got put into place. The budget stayed on track for 2023. For 2024 year-to-date, budget revenues are up by 50%, while expenditures have risen by only 20%. Within that, oil and gas revenues have increased by 80%, while non-oil and gas revenues are up by a respectable 40%. This latter category is largely internal to Russia, and thus not sanctionable from the outside.

Russia has little in the way of external debt vulnerability: even without its frozen assets, Russia could just about pay off all of its $326 billion of external debt in cash anytime. There was a spike in Russia’s current account surplus in March 2024 to $13 billion, the second-highest reading in 15 years. Industrial production is growing, with Purchasing Managers’ Indices above 50. Unemployment is down to around 3%, and wages are rising faster than inflation.

However, this macro strength is also the symptom of a demographic problem and is coming at the expense of long-term growth. Chronically low birth rates and brain drain have now combined with resources directed to defense industries and the military to create tight labor supply conditions, if not shortages in some areas. This means that Russia is unable to pursue some of its non-defense national development projects, which is likely to weigh on long-term growth.