As global markets grapple with the prospect of higher rates for longer, it’s important to keep an eye on another important potential headwind: the direction of worldwide central bank asset purchases.

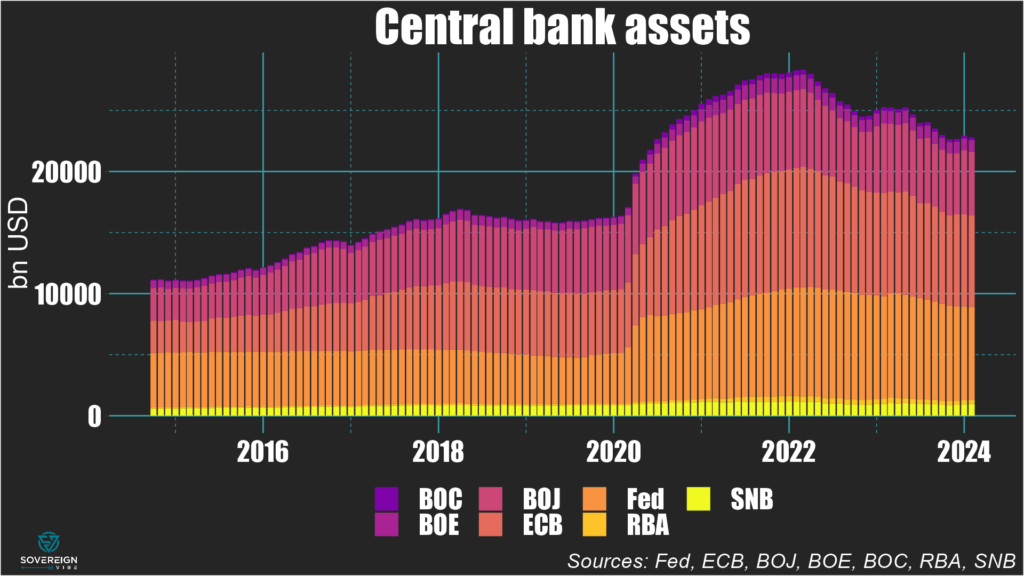

Without delving too deeply into the history of unconventional monetary policy, post-Global Financial Crisis the world’s major central banks implemented quantitative easing programs. This meant buying government bonds as a way to further support recovery by injecting cash into the economy. As a result, central bank balance sheets expanded significantly.

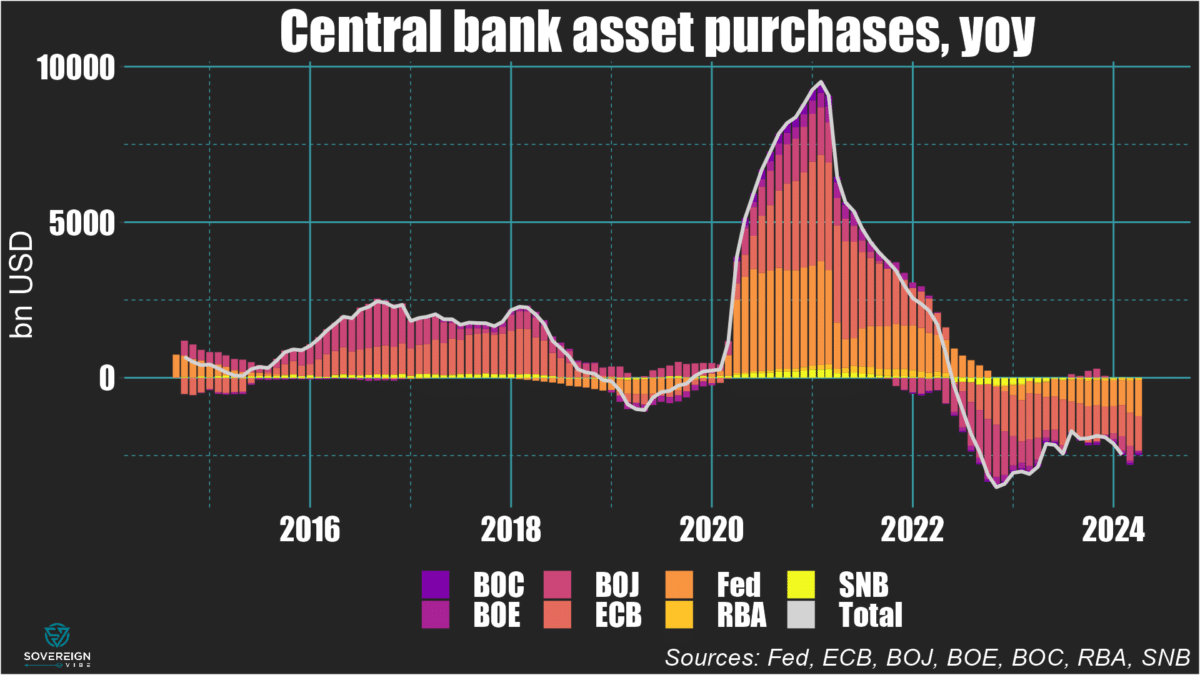

All the extra liquidity swilling around as a result of these purchases clearly has an impact on markets. When central bank buying decreases, this often seems to coincide with challenging periods for the S&P500, the MSCI All-World Index, and others. For example, 2018 and 2022 saw poor market returns, just as central bank asset purchasing was dipping in to negative territory, as presented in the chart below.

Looking at the balance sheets of major central banks, purchases of total assets are simply any changes from one period to the next. I’ve chosen a 12-month rolling window to show you annual purchases each month here.

Central bank buying was positive throughout much of the 2010s, hovering around $2.5tn year-on-year over 2016-2018, before turning negative in late 2018 and most of 2019. Annual purchases then skyrocketed to nearly $10tn during the pandemic, amid market ebullition from H2 2020 until the Omicron Covid variant dampened sentiment in November 2021 .

Since Q2 2022, annual central bank asset accumulation has been negative, reaching a nadir of some -$3tn in H2 of that year, which was a rough one for most asset classes. From late 2022 and through most of 2023, net buying headed back towards positive territory, with last year witnessing strong, broad-based returns.

In 2024, purchasing is starting to decrease again, which would be a negative signal for markets if the trend is confirmed. This tighter stance aligns with the likelihood that the Fed will keep rates at current levels for much of the year and the Bank of Japan allowing short term rates to increase when it abandoned yield curve control last October.

However, there may be a silver lining for markets. Weak growth and low inflation prints in the Eurozone are likely to lead the ECB to cut rates in 2024. While the ECB may not abandon the quantitative tightening program launched in March 2023, it is unlikely to ramp it up at a time when it needs to loosen policy. This is especially true since it has managed to reduce its balance sheet from €8.8tn in 2022 to around €6.6tn today, as visualized in dollar terms below.