Double-whammy of higher U.S. yields and stronger dollar, with peak deglobalization still to come

Most people think my newsletter is only about sovereign debt.

This is a fair assumption: after all, “sovereign” is in the name.

But it’s also about deglobalization, geoeconomic fragmentation, slowbalization.

Or whatever other convoluted term you want to label the post-2016 Trump victory 1.0 and Brexit world as.

I write about these topics as well because they are so closely intertwined with what is happening in the emerging markets and sovereign debt space.

The daily symptoms of this world are often sanctions and tariffs, or any other number of phenomena that harden borders and disintegrate international relationships.

And it’s this reigning ambiance that also led me to call this newsletter “Sovereign Vibe.”

Countries are turning inward, putting themselves first, and promoting isolationist and protectionist policies in one form or another.

It’s sovereign first, friends next, enemies last, and multilateralism forgotten.

Never has that been more true than after Trump’s sweeping 2024 electoral triumph, carrying the U.S. popular vote and a strong mandate for “America First” policies.

Buckle up: we’re going to be in for a wild four years and beyond…

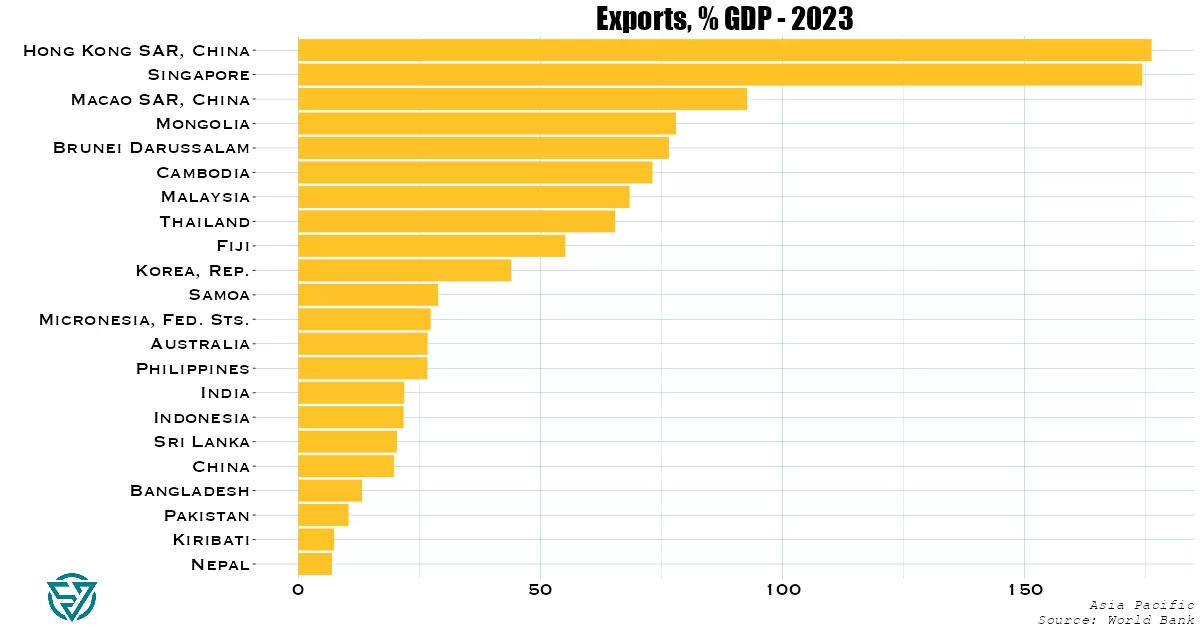

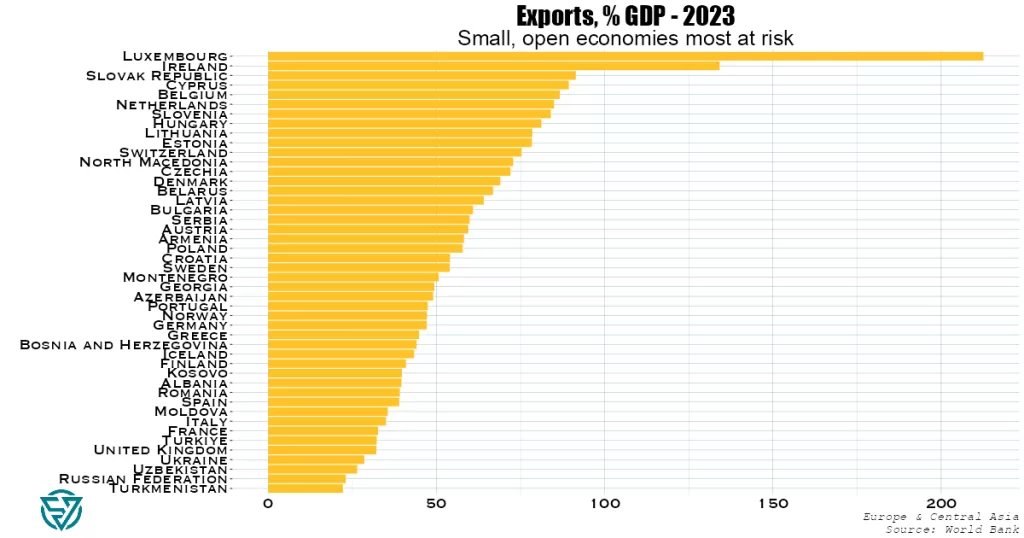

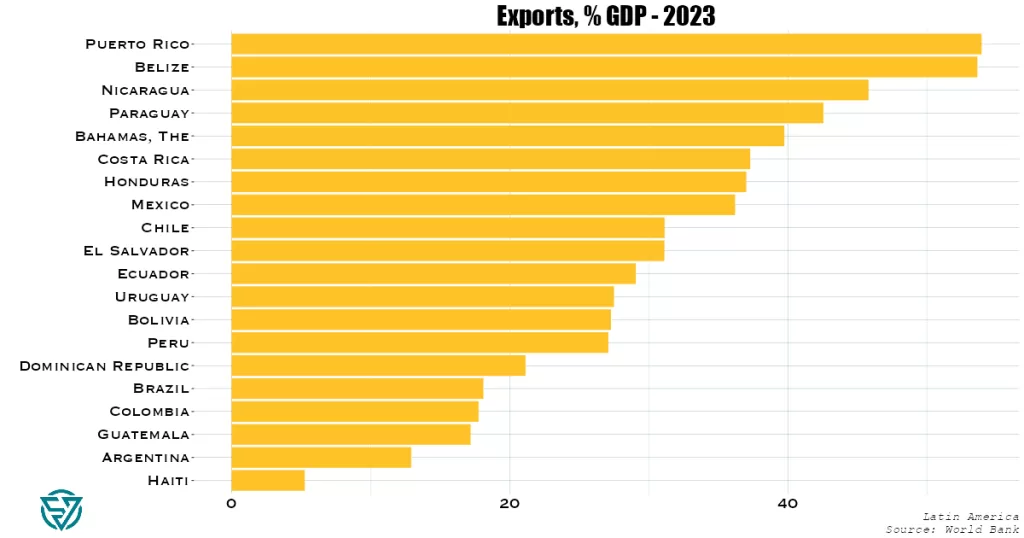

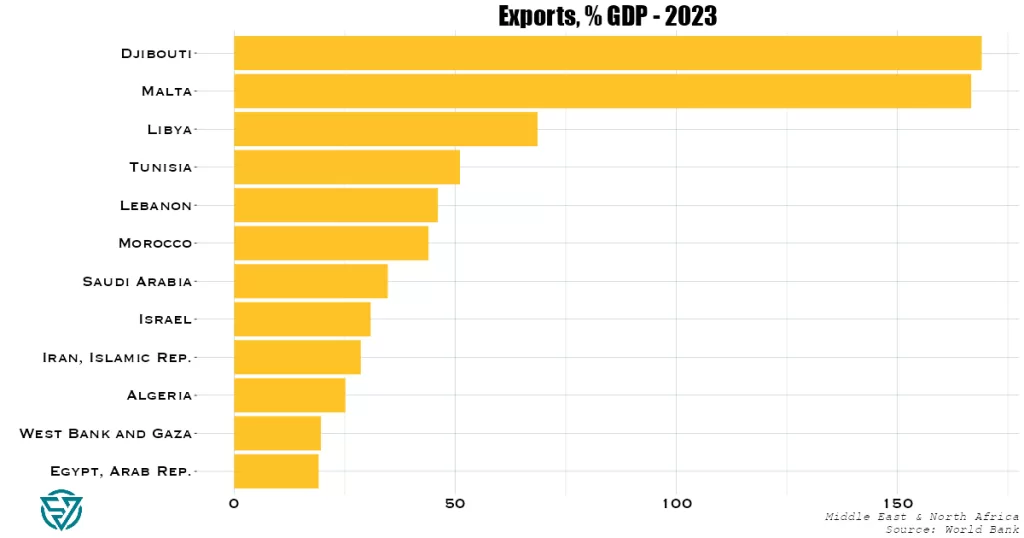

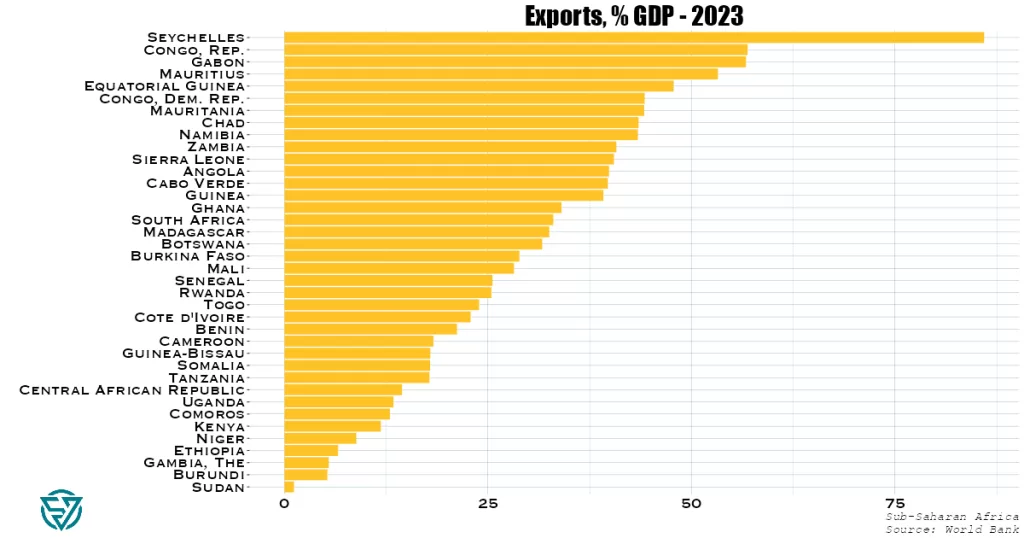

Exporters at risk

With Trump proposing 60% tariffs on imports from China and 10-20% on imports from the rest of the world, countries with a heavy reliance on exports are at risk.

This is especially true for countries with direct export exposure to the U.S., though interconnected global supply chains means that countries with high shares of exports to GDP may be particularly vulnerable.

While Trump’s trade policies may take aim mainly at manufactured goods, it is unclear the extent to which they will target services and raw materials.

The charts below break down export exposure by region:

Fed rate-cutting

The conditions were supposed to be favorable to emerging markets.

The beginning of a Fed rate-cutting cycle is reliably a good omen for the EM universe.

Lower U.S. yields mean lower yields for EM debt, especially if it is dollar-denominated.

While lower borrowing rates for EMs assumes spreads remain somewhat steady when U.S. rates are lower, in any case the effect of lower U.S. rates helps drive capital flows towards EM.

Trump trades in full swing

But Trump’s victory has just blown that narrative out of the water.

Sure, U.S. yields were already rising in October on the back of strong non-farm payroll data and robust economic growth, though this was tempered by weak jobs data late last week.

Yet the market reaction has pushed U.S. yields up further across the yield curve, in a bear steepening, which sees long-term rates rise fastest.

This means that markets expect increases in:

nominal growth & inflation: as a result of lower taxes, higher spending and higher fiscal deficits.

uncertainty: due to policy volatility, including on trade tariffs, hence the higher term premium at the longer end of the curve.

Meanwhile, other “Trump Trades” are in full swing: U.S. stocks, the USD, and Bitcoin are all up.

EM under pressure

In this new higher-U.S.-yield, stronger-USD environment, EM currencies have taken a battering in the immediate aftermath of the election result.

The broad EM currency index registered its largest daily loss since early 2023, with the Mexican peso and Eastern European currencies suffering.

Asian equities pulled down the MSCI EM equity index by 0.7% on November 6th, as market participants evaluated the impact of Trump’s tariff policies.

High economic-political uncertainty paired with low volatility amplifies market risks

In its recently-released Global Financial Stability Report, the IMF warns that the disconnect between rising economic and geopolitical uncertainty and low financial volatility increases market risks.

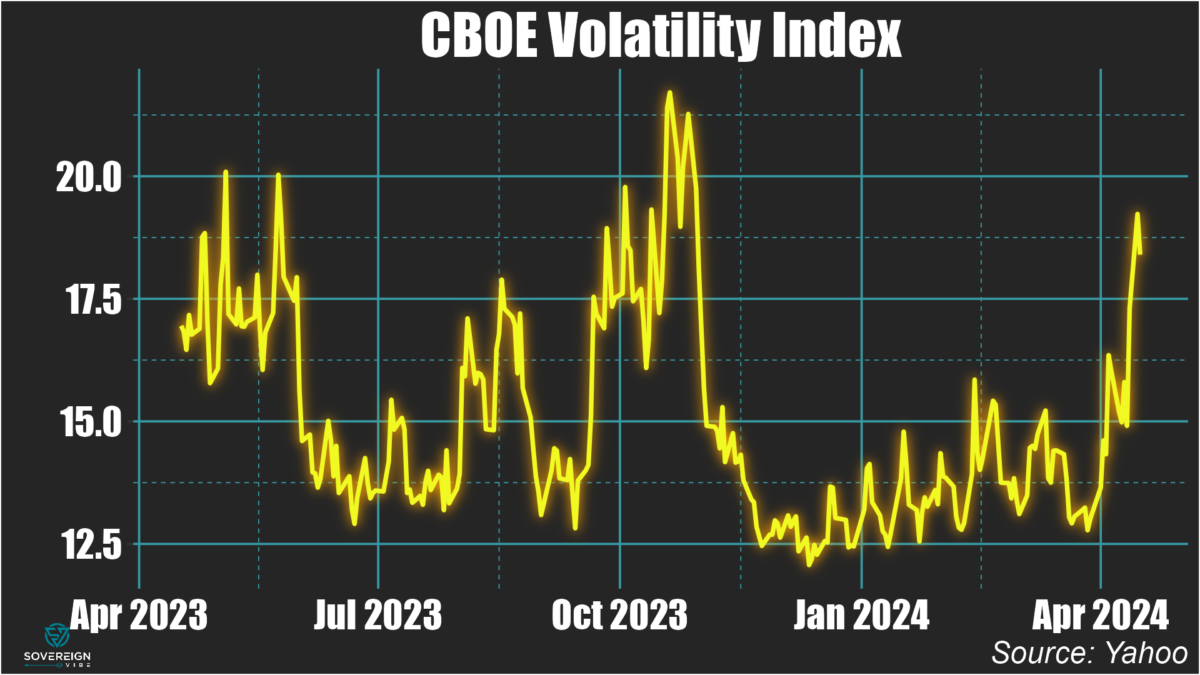

The CBOE Volatility Index – a barometer of equity market volatility – has remained at or below 20 for much of 2024.

The IMF’s warning is in keeping with an April 2024 edition of this newsletter, “Are markets underpricing geopolitical risks?”

August volatility

The sole exception to this low volatility occurred in early August, when the Bank of Japan spooked markets with an unexpected interest rate hike.

This surprise unwound massive carry trade positions from the yen into assets denominated in emerging market currencies, causing the VIX to surge.

Carry trades involve borrowing in a low-interest rate currency to invest in a high-interest rate currency.

Kazuo Ueda has been serving as the Bank of Japan’s Governor since April 2023. FT montage/Bloomberg

Threats to lofty valuations

This year credit and equity markets have remained strong despite slowing earnings growth and rising fragilities in parts of the corporate and commercial real estate sectors.

Amid already-lofty valuations, there are concerns that, as many central banks pursue their easing cycles, interest rate cuts could lead to asset bubbles and rises in private and government debt and non-bank leverage.

The Fund underscores the uncertainties around military conflicts and the future policies of newly elected governments – in a nod to the many elections in 2024, including in the U.S.

Yet this year only a monetary policy event – i.e. the BoJ-carry trade de-leveraging – has caused volatility to rise, rather than any military or political factors.

While some military or political factors could roil markets, economic policy surprises and threats to corporate and household resilience could just as easily cause volatility to surge.

Sudan’s brutal but forgotten civil war has affected Egypt’s economy but has otherwise had a negligible economic impact beyond its borders. AFP

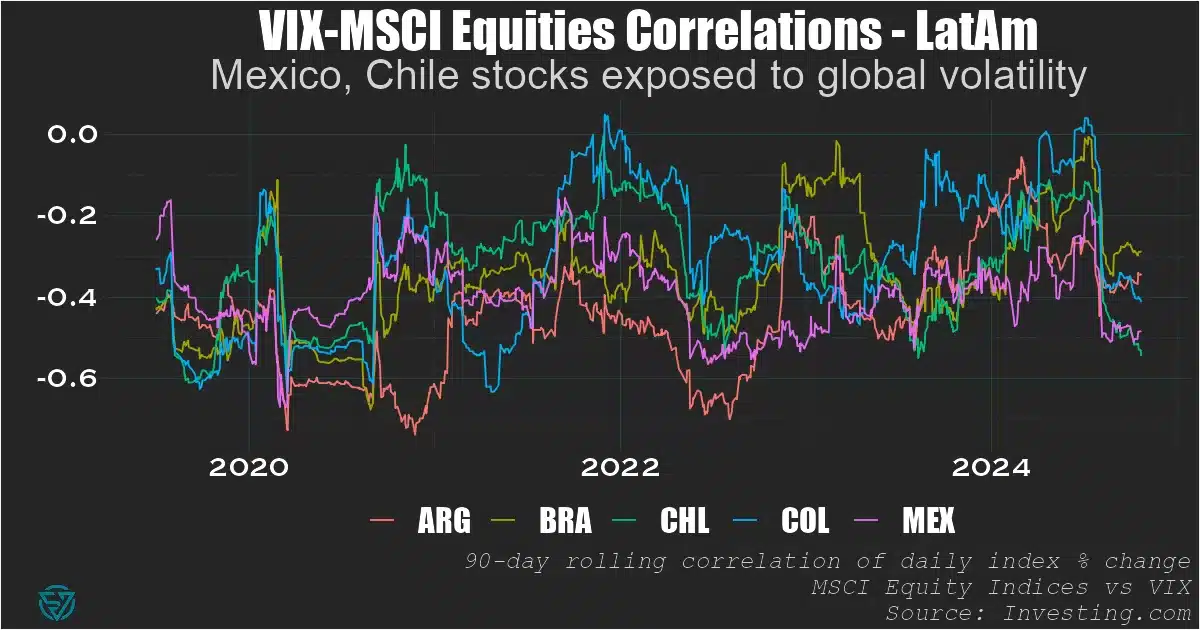

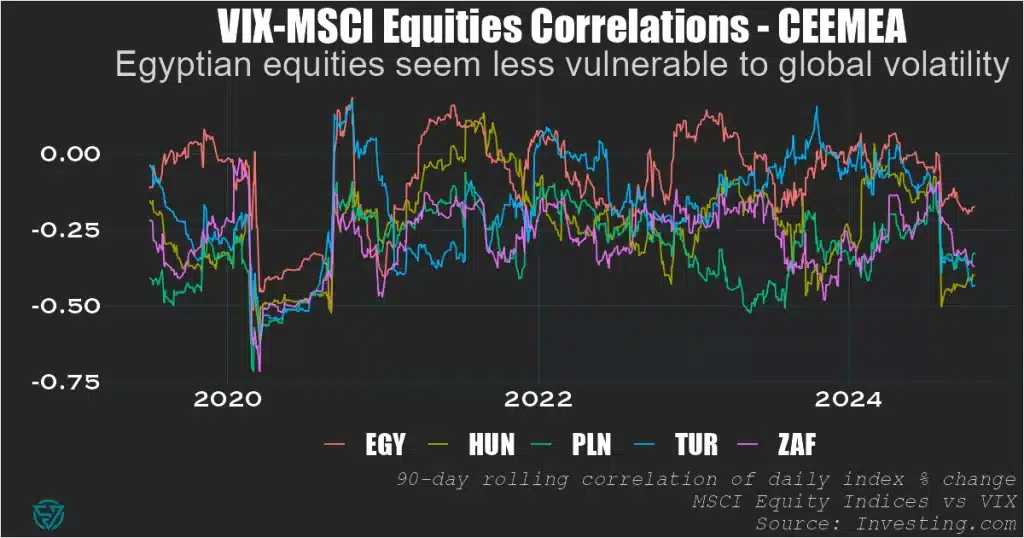

VIX-equity market correlations

Regardless of what causes equity market volatility, seeing how emerging country equity markets are correlated with VIX yields some clues as to which countries are more vulnerable.

To do this, I compare daily changes in VIX to daily MSCI index returns and smooth that data out over a 90-day period.

These VIX-MSCI correlations are generally negative, as expected, meaning that a rise in volatility is associated with a decline in daily returns.

The relationships are naturally dynamic over time, given the presence of idiosyncratic market drivers in each country and the varying sources of global market volatility.

CEEMEA

Looking across the three EM regions, in CEEMEA Egypt currently appears less negatively-correlated – and therefore less vulnerable – to VIX.

In all five countries, the negative VIX correlations dropped to nearly -0.75 during the first wave of the pandemic in H1 2020, underscoring the risk to EMs from global vol.

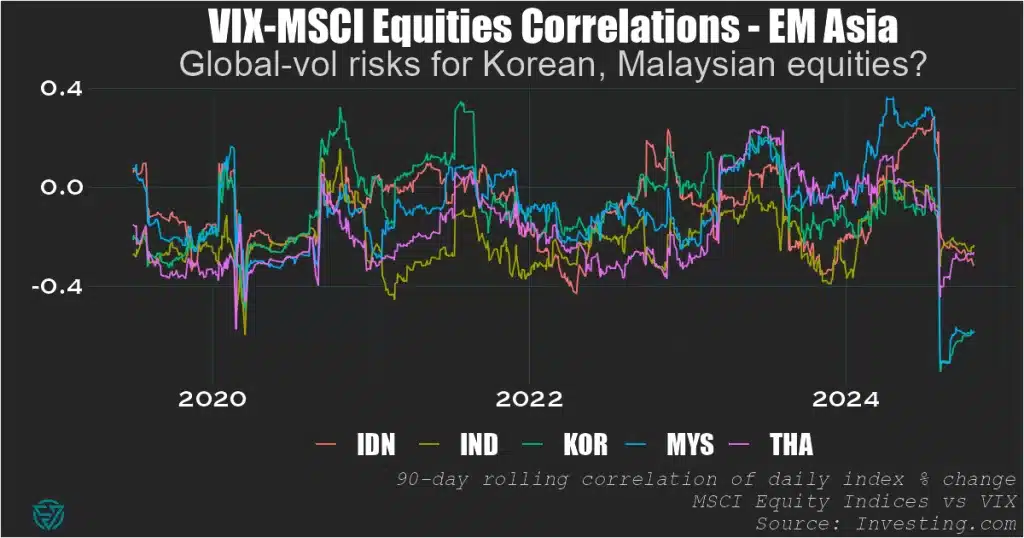

EM Asia

In EM Asia, Korean and Malaysian equity markets appear most at risk from changes in VIX.

We can’t really ascribe it solely to them being small, open economies, as their VIX correlations aren’t systematically more negative than their larger regional peers.

But certainly something about the current environment – whether global or local – is causing these correlations to be at -0.6, which points to significant VIX vulnerability.

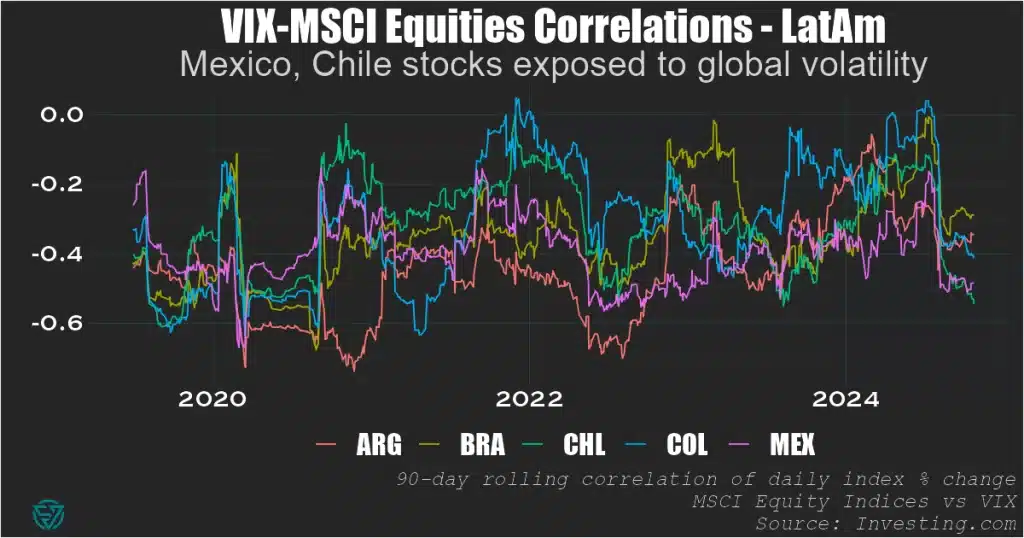

LatAm

As for LatAm, Mexico and Chile stocks are most exposed to global vol.

Their equity market correlations with volatility are around -0.5, meaning they seem to face less VIX risk than Malaysia or Korea but more than any of the CEEMEA countries.

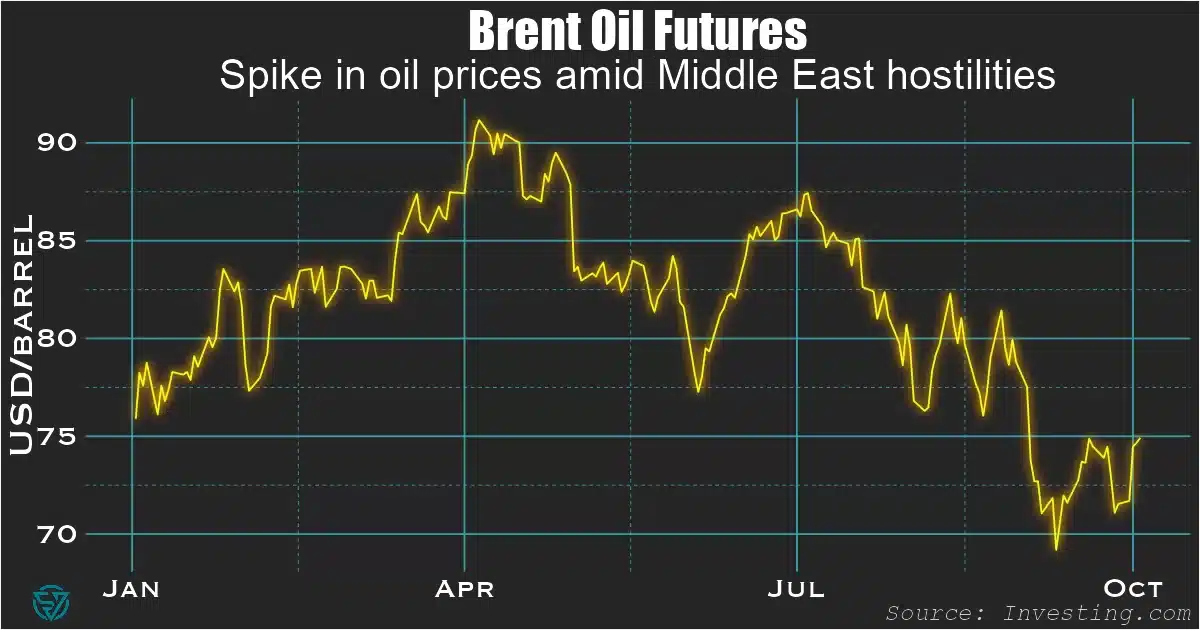

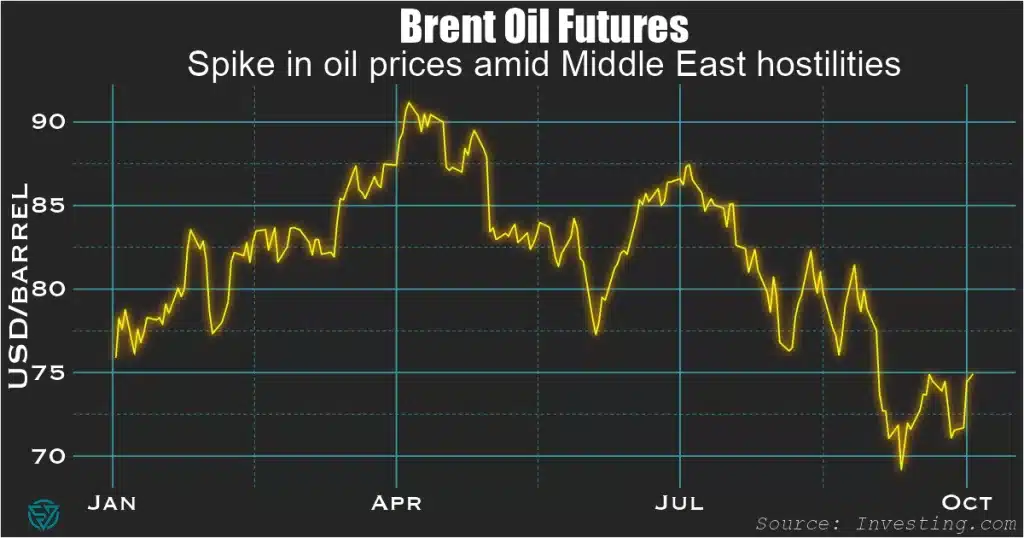

The recent escalation presents downside market risks, albeit these are limited.

Brent oil prices have risen quickly this week to reach $74.92 per barrel at the time of writing on Thursday, reflecting concerns at potential disruption to Iranian supply.

Market participants see a non-zero chance of Israel targeting Iran’s oil facilities in response to over 180 Iranian missiles fired towards its territory.

April 2024 redux

Today’s situation contrasts with the Iran-Israel missile and drone strikes in mid-April 2024. These didn’t cause oil prices to increase, given Israel’s muted response at the time.

In fact, April prices decreased on the back of slower US business activity and limited concerns over the Middle East.

The difference this time is clearly Netanyahu’s willingness to use a more aggressive approach against Lebanon and Iran, justifying rising prices.

Limited fallout

The conflict has yet to spill over to the broader Persian Gulf, which would be a driver for a larger jump in prices.

In the meantime, OPEC+ cuts to production in recent years have resulted in 5 million barrels per day of excess capacity, which could be restored in case of Iranian supply disruptions.

Although these Middle East tensions have shown some signs of dampening investor risk sentiment over the past week, the effect has been limited.

Over the past week, the S&P500 is down marginally, and the dollar index has strengthened, both of which are consistent with a risk-off mood.

As for other havens, these haven’t moved in a risk-off direction. US Treasury yields are up (on the back of strong payrolls), the yen has weakened, and gold has traded flat.

Stay focused on policy, macro data, and earnings

For all these reasons, investors shouldn’t worry too much about the Israel-Lebanon/Iran disrupting markets much beyond what may be a temporary surge in oil prices.

As is usually the case, monetary and fiscal policy, macroeconomic data releases, and earnings reports will drive market reactions more than politics or geopolitics.

For instance, in the US, jobless claims, Purchasing Managers’ Index reports, services activity data, and the non-farm payrolls report are all due to be released this week.

These will affect markets much more than the Israel-Iran situation, given the need to position around the path of Fed policy in the rate-cutting cycle that began last month.

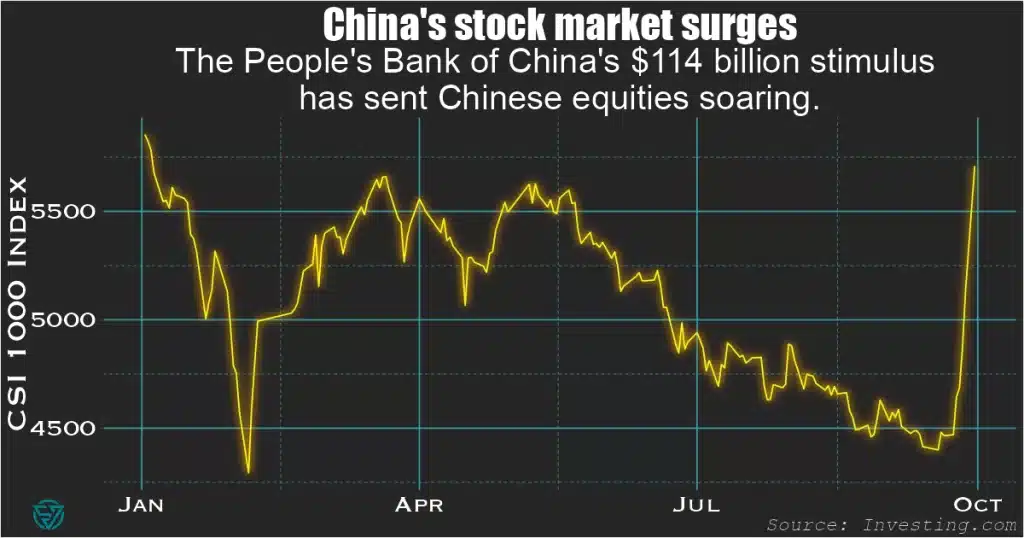

China’s recent stimulus package is another case in point. Last week the People’s Bank of China announced rate cuts on mortgages and reserve requirements, in addition to a $114 billion facility to fund stock purchases.

These are designed to support the distressed real estate market and reverse deflation. Local equity markets reacted with the single largest daily gain since 2008, even though the impact of these measures on earnings is of course yet to be seen.

In any case, the geopolitical tensions around a Japanese destroyer sailing through the Taiwan Strait were barely felt in markets last week despite the China’s fuming response and putting its military on “high alert.”

Emmanuel Macron wasn’t the only person traveling from France to Berlin last week: I was as well, to attend the inaugural Berlin Energy Forum on May 21st. Here are the key takeaways:

First introduced in December 2022 and February 2023, energy sanctions are having mixed effects, but more can be done.

Introduced in December 2023, the threat of secondary US sanctions against non-Russian financial institutions engaging in certain types of transactions with Russia are proving effective, as banks cut ties with Russian counterparts.

The West missed a chance to devastate the Russian economy in 2022.

Russia is in a very strong macroeconomic position right now, but this is coming at the expense of long-term growth, with the military-industrial complex using labor and resources at the expense of national development projects.

Saudi Arabia and other Middle Eastern oil exporters are the big winners here.

Missed opportunity

The West had the opportunity to wreck the Russian economy in 2022, as its sanctions in response to the Russian military’s February invasion of Ukraine began to bite. But the sanctions had a limited effect because billions of Western money continued to flow into Russia as oil and gas payments. Putting money in an escrow account could have had a major impact.

Meanwhile, Russia’s central bank governor Elvira Nabiullina responded brilliantly in 2022 with large interest rate hikes, capital controls, and other FX restrictions. Moreover, Russia has been preparing since the 2014 sanctions by building up its shadow fleet of oil tankers ahead of time and by diversifying export routes, e.g. an oil pipeline to China.

Saudi Arabia and OPEC are playing an important role via keeping supply constrained and prices relatively high, benefiting Russia. Low-cost producers such as Saudi Arabia have more pricing power over the global oil market. So even if a higher-cost oil producer such as the United States could ramp up production immediately, the Saudis and other low-cost producers can still swing the market price by constraining supply.

Relevant sanctions actions

Western capitals only started applying energy sanctions against Russia nearly a year after the February 2022 invasion, with the crude oil price cap and embargo introduced in December 2022 and the oil products price cap and embargo in February 2023. The goal of these sanctions is to keep Russian oil volumes on the market, so that prices at the gas pump remain stable globally, while undermining Russia’s oil revenues via lower prices and fewer clients.

In December 2023, the US Treasury sanctioned 41 oil tankers comprising Russia’s shadow fleet, which has had an impact. However, enforcement has slowed in 2024, while Moscow has managed to add new vessels to the fleet.

Also in December 2023, President Biden issued an Executive Order to impose secondary sanctions on financial institutions engaging in transactions that violate the oil price cap or other sanctions against Russia. These have so far proven to be effective, as banks in China, the UAE, and Turkey limit payments to Russia and ask for increased compliance documentation from counterparties. These secondary sanctions were a top concern at the recent Putin-Xi summit in Beijing.

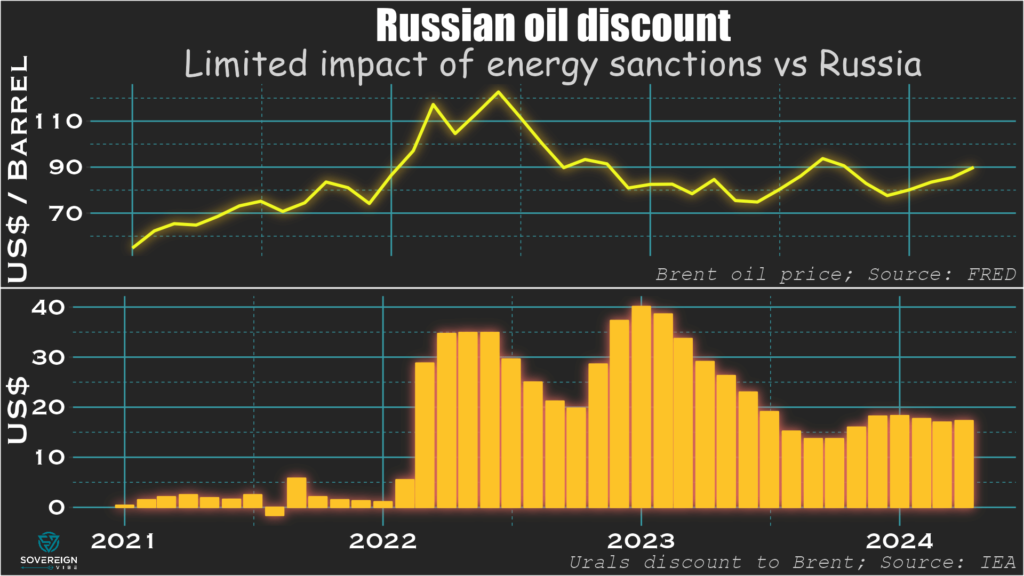

Discount on Russian oil

Everyone involved in Russian oil trade wants to be compensated for the risk of buying “tainted” product. The discount on Russian Urals oil rose in H1 2022 to $30-$35, as a geopolitical risk premium and had nothing to do with sanctions. This gradually declined as market players learned what they could get away with. This discount rose again from December 2022 as the crude price cap and embargo were first announced.

Each $10 of discount costs Russia $20 billion in export earnings if in place over the course of a year, so there is a tangible impact. But also consider the side-effects: the discount provides a subsidy to the buyer, e.g. China, India, Turkey, giving them an industrial advantage over Russia’s opponents.

The Western embargo worked because there is a discount on Urals, which Western countries used to buy, but none on Russian ESPO oil delivered from Siberia to China. It is clear that the $60 price cap on Russian oil hasn’t worked, as there are no two separate concentrations of transactions at $60 and the market price.

In the summer of 2023, Russia mobilizes its 41-strong shadow fleet, oil prices rise, and Russia’s discount drops. The US Treasury’s Office of Foreign Assets Control (OFAC) starts targeting the shadow fleet, so the discount starts rising again from end-2023. But OFAC stops enforcing these sanctions sometime in Q1 2024, so the discount hasn’t widened further. Part of the problem is that by the time governments sanction a vessel, it has been renamed and the company re-registered.

Three problems with energy sanctions on Russia

The first way to get around sanctions is violation. 29% of the Russian oil trade touches on G7 services, so 29% should be under the $60 cap. But only 2% is: the buyers are lying, which is attestation fraud. The buyers are no longer international oil traders but suspected subsidiaries of Russian companies recently registered in Dubai and in other jurisdictions.

The second is evasion. The shadow fleet now carries ~80% of Russian crude and ~50% of oil products, shares that have risen quickly in recent months.

The third hindrance is an unwillingness to disrupt access of Russian oil volumes to the global market. This is needed to wage economic warfare, but it is doubtful that G7 taxpayers would accept this. For instance, the US has given India unofficial clearance to accept Russian oil from ghost tankers as it doesn’t want the market to be too tight.

A strong macro position in the short- and medium-term

Although the discount on Urals oil has caused Russia to lose some oil revenues, relatively high oil prices have made up for those losses. Russia’s oil export earnings and budget oil revenues haven’t declined. The budget deficit widened in Dec 2022-Feb 2023. But the larger deficit in early 2023 was partly because Finance Minister Anton Siluanov was front-loading expenditures to avoid an end-of-year surprise.

By summer 2023 Russia had started getting revenues from from new oil export machine to India after the long oceanic voyages got put into place. The budget stayed on track for 2023. For 2024 year-to-date, budget revenues are up by 50%, while expenditures have risen by only 20%. Within that, oil and gas revenues have increased by 80%, while non-oil and gas revenues are up by a respectable 40%. This latter category is largely internal to Russia, and thus not sanctionable from the outside.

Russia has little in the way of external debt vulnerability: even without its frozen assets, Russia could just about pay off all of its $326 billion of external debt in cash anytime. There was a spike in Russia’s current account surplus in March 2024 to $13 billion, the second-highest reading in 15 years. Industrial production is growing, with Purchasing Managers’ Indices above 50. Unemployment is down to around 3%, and wages are rising faster than inflation.

However, this macro strength is also the symptom of a demographic problem and is coming at the expense of long-term growth. Chronically low birth rates and brain drain have now combined with resources directed to defense industries and the military to create tight labor supply conditions, if not shortages in some areas. This means that Russia is unable to pursue some of its non-defense national development projects, which is likely to weigh on long-term growth.

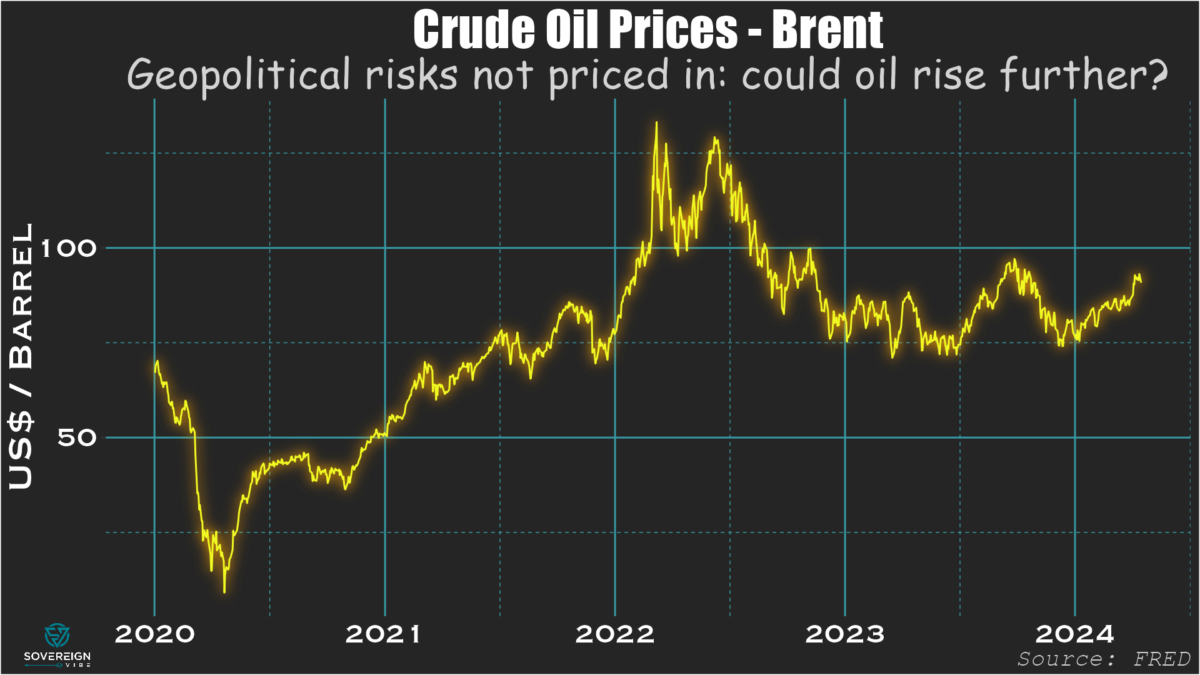

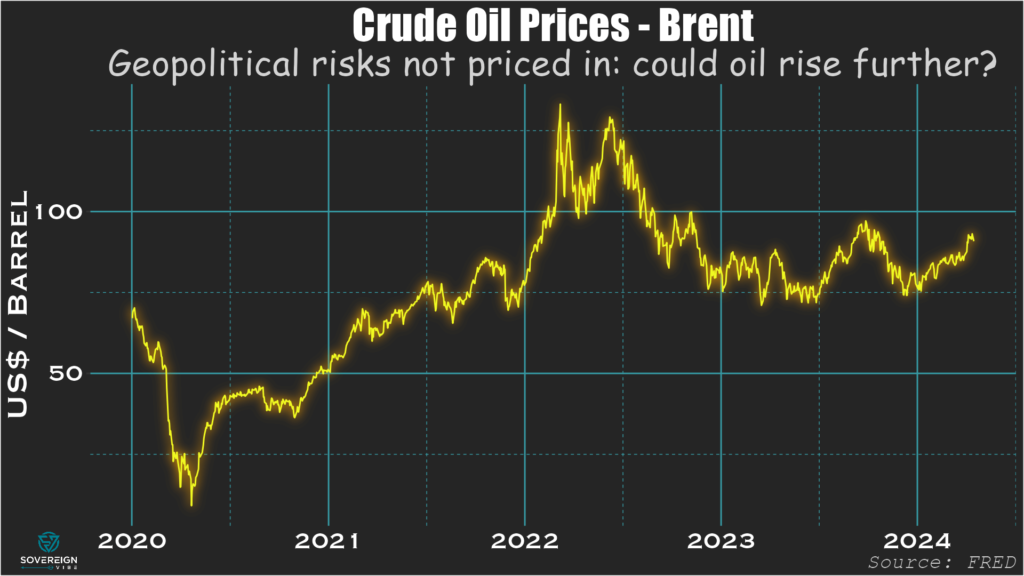

Oil prices have actually declined in the wake of Iran-Israel.

In remarks made on Tuesday this week, JPMorgan Chase boss Jamie Dimon stated, among other things, that he’s surprised at oil not rising further amid recent geopolitical tensions.

Brent crude has mostly been trading in the $85-90 range over the past month, though that is still up significantly from around $75 at the beginning of the year.

The man certainly has a point here, especially if energy infrastructure suffers damage in the Middle East and Europe. Yet the Iran-Israel strikes over the past ten days haven’t had a discernible impact.

In fact, oil prices have declined from around $90 to $88 in recent days on the back of slower US business activity and easing concerns over the Middle East. The American cool-off makes good sense, at least.

But with war raging in Ukraine, disruptions to Red Sea maritime traffic, the ongoing Gaza situation, and a series of other conflicts around the world, perhaps markets are becoming desensitized to bad news. At least for now.

In any case, the geopolitical backdrop strikes me as exceedingly gloomy, and perhaps investors are getting complacent about geopolitics, just as they were about inflation around the turn of the year.

Speaking of which, with sticky US inflation and the possibility of another rate rise now on the cards, the double-whammy of an even stronger USD and even higher oil prices would be especially challenging for oil-importing emerging markets. This is not an outcome anyone should want, since the EM/FM universe is awash in dollar-denominated debt.

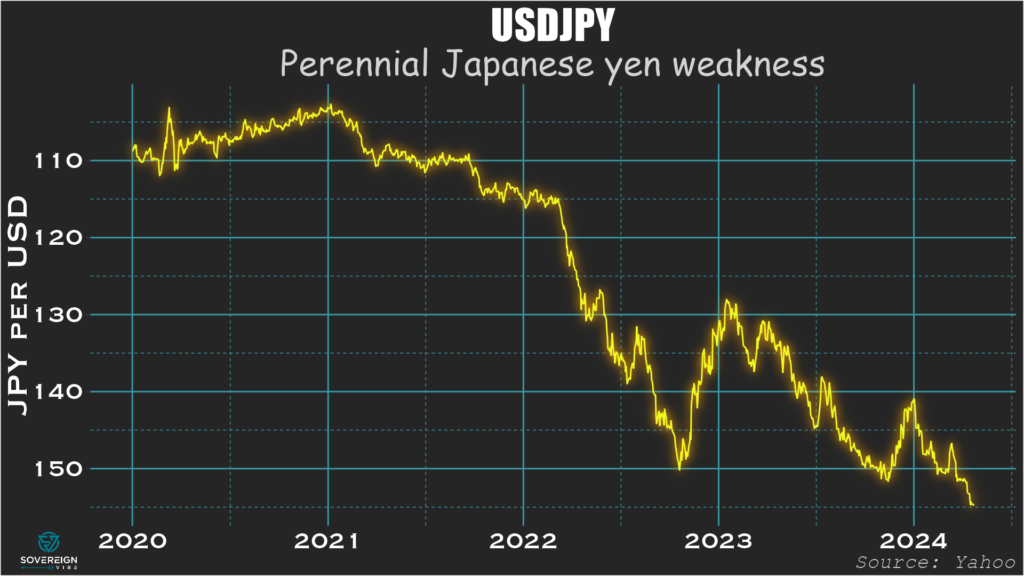

I’m not the only one in a risk-off mood, with gold currently at record highs. Though skittish sentiment isn’t full-fledged. One of the other main safe haven assets, the yen, is persistently weak, with PMI still below break-even despite some signs of recovery.

I wouldn’t be surprised to see the yen and oil rise in coming weeks given all the smoldering fuses currently inhabiting a geopolitical landscape of powder-kegs.

The headline article in yesterday’s FT focused on the “soaring” Vix index, a well-known measure of investor skittishness.

Much ado about VIX

VIX rises when market participants expect more volatility in the S&P 500, as it reflects the cost of buying options used to profit from changes in stock prices.

It’s clear that markets are concerned that interest rates will be higher for longer in the US as the Fed grapples with sticky inflation and by escalating Iran-Israel tensions.

These are the reasons that pushed VIX this week to its highest level since October (see chart). That spike occurred amid investor worries over Hamas’s attack on Israel and before Fed chair Jerome Powell’s dovish end-of-year remarks.

VIX is actually quite low

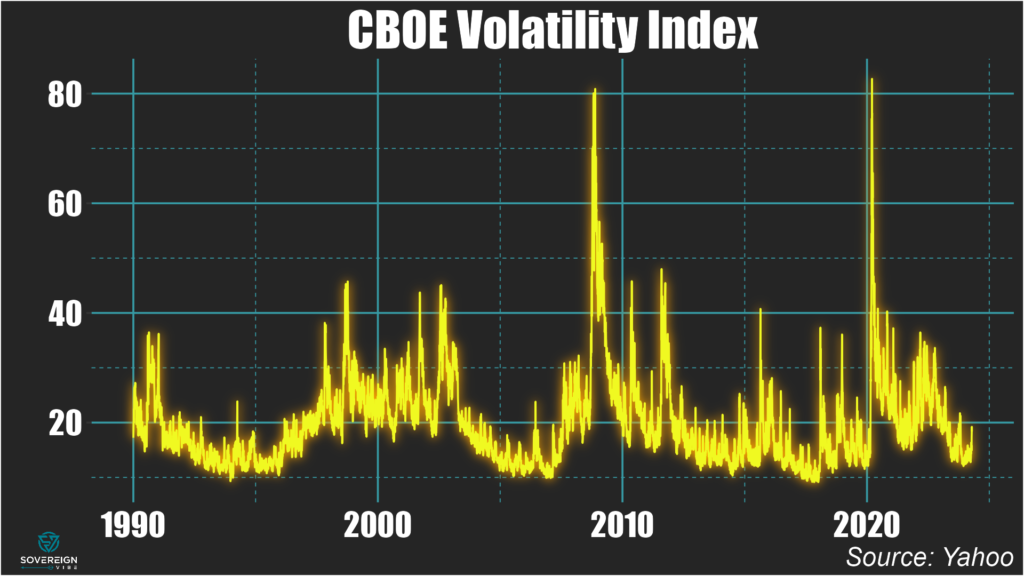

While it is true that this could mark a turning point for markets, what stands out to me is how low VIX went in December and January. Upbeat sentiment around the Fed lowering rates by June or earlier would certainly have warranted somewhat of a decline.

But Israel’s retaliation against Gaza, Houthi attacks on maritime traffic in the Red Sea, and reversals on the battlefield for Ukraine’s military amid US Congressional delays on aid have punctuated the past several months. These should have dampened investor euphoria more than they did.

Moreover, taking the long view, VIX isn’t exactly “soaring” (see chart). Perhaps it should be higher than where it currently is, and may well rise.

But, frankly, with the pandemic and the wars in Ukraine and Gaza defining the decade so far, this modest rise in the VIX shouldn’t be at all surprising. This is what I believe is called, in the official parlance, a nothingburger.

As for the supposedly “soaring” VIX, for the FT I have only one question:

With so much of the world headed to the polls in 2024, a quick stock-take of results so far and a look ahead are in order. The outcome of each contest shapes broader international trends of deglobalization.

Of populists & liberals

The paradox is that both populist and liberal political parties have pursued policies leading to international economic fragmentation. On the populist side, trade tariffs à la Trump are the most obvious example. Populism has of course also lead to schisms in western cooperation, whether Republican reticence on NATO and Ukraine, or pro-Russian leadership in Hungary and, more recently, Slovakia (see below).

Liberal political forces are also responsible for deglobalization. The prime example is the widespread use of economic sanctions by the Biden administration and Western Europe against Russia. Yet the current US administration has not only kept the Trump era’s trade barriers in place, it has also introduced more protectionist measures through the landmark Inflation Reduction Act.

Moreover, the success of liberal parties in the broad West can benefit cohesion among allies at the expense of decoupling from opponents. Case in point, Finland’s new president comes from a pro-Europe, pro-NATO party, highlighting how joining NATO bolsters cooperation within the West while also – quite understandably – turning away from Russia.

Populism has the edge

Despite these nuances, a high-level view of electoral outcomes around the world sheds light on the direction that future international economic relationships will take. By the end of the year, the US, India, Indonesia, Mexico, and many other countries will have voted. The question isn’t so much whether the world will continue to fragment, but rather how, which is what monitoring elections can help answer.

So far this year, populist forces have advanced to varying degrees in Slovakia, Indonesia, Senegal, Poland, and will likely maintain power in India. The military continues to loom over politics in Pakistan, while Bangladesh’s authoritarian Awami League has left virtually no space for any opposition.

In contrast, results in Taiwan, Finland, and Turkey have favored more liberal political parties. Similarly, upcoming legislative elections in South Korea will likely see the center-left and center-right parties continue to dominate the political landscape.

Electoral highlights year-to-date

Poland: The nationalist, opposition PiS party came out ahead in local elections on April 7th, but Prime Minister Tusk’s ruling coalition will likely hold on to power in most regions.

Slovakia: The result of April 6th’s second round runoff in Slovakia are in, with the ascension of pro-Russian politician Peter Pellegrini to the presidency confirming the country’s pivot towards Moscow, after Robert Fico’s return as Prime Minister in October 2023.

Turkey: The victory of the opposition Republican People’s Party in local elections on March 31st were a setback to President Erdogan’s ruling AKP, with Istanbul’s mayor Ekrem Imamoglu strengthened by this outcome.

Indonesia: The general election on February 14th marks a turn away from incumbent Joko Widodo’s center-left PDI-P to the nationalist, right-wing populist Gerindra party under current defense minister Prabowo Subianto, who will be sworn in as president in October.

Pakistan: International media have contested the fairness of the February 8th elections, though former prime minister Imran Khan’s PTI secured the largest share of the vote despite being in prison. The PML-N’s Shehbaz Sharif is now prime minister of a coalition government.

Senegal: Political novice Bassirou Diomaye Faye rose to the presidency in the March 24th election, defeating the government-backed candidate. Although Faye has announced several significant policy changes, the composition of his economic team has reassured investors.

Taiwan: The results of the January 13th presidential election represent continuity for Taiwan in its opposition to the One China policy, with the center-left DPP’s Lai Ching-te to be inaugurated as president in May 2024.

Bangladesh: The US State Department claims that January 7th’s general election wasn’t free and fair. In power since 2009, incumbent Prime Minister Sheikh Hasina of the Awami League has won election for the fourth consecutive time.

Finland: The January 28th and February 11th two-round presidential election resulted in the victory of Alexander Stubb, of the pro-NATO, pro-European liberal-conservative National Coalition party.

April elections

India: While there is little doubt that Narendra Modi’s BJP will secure victory in the seven-round general election, the Lok Sabha, running from April 19th – June 4th, it appears voters are willing to accept some democratic backsliding in exchange for stronger economic growth.

South Korea: The center-left DPK holds the most seats in the National Assembly, while its historic rival, the conservative PPP, holds the presidency. These two main parties appear to be neck and neck in polling for the April 10th legislative election.

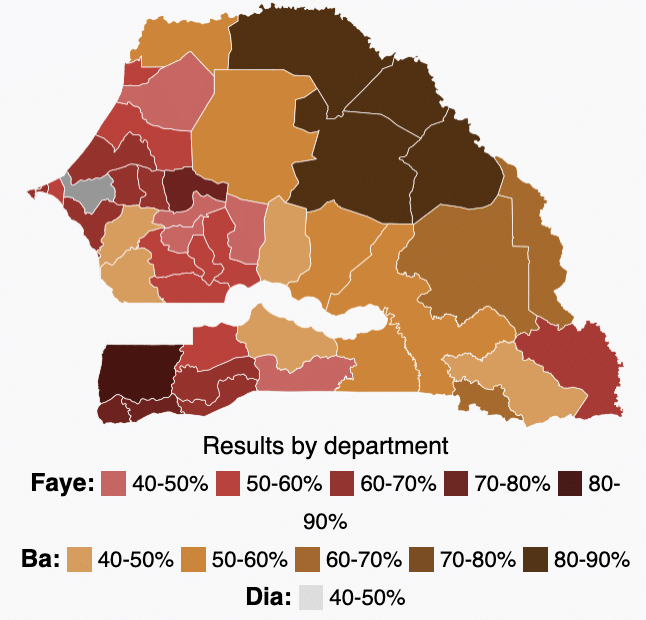

Today’s spotlight is on Senegal’s presidential election in March 2024 and the spectacular rise to power of political novice Bassirou “Diomaye” Faye, a 44-year old former tax inspector who went from prison to the presidency in scarcely 10 days. Digging beneath the surface of the electoral results reveals some oft-neglected ethnic undercurrents at play in Senegal and elsewhere in the Sahel that investors and observers should keep front of mind.

Why democratic stability is so rare in the Sahel

One of the things that struck me when living and working in Africa was the yawning gap between the international press coverage of electoral politics and the realities on the ground, which were both obvious and patiently explained to me by local friends.

I am of course referring to the ethnic dimensions of politics that are ever-present in so many African countries but that mainstream international media so often ignores.

In Africa, ethnicity doesn’t explain everything, but nothing can be explained without ethnicity.

Bernard Lugan

Democracy wins

Last month’s presidential elections in Senegal were first and foremost about the Senegalese people expressing their desire for change. As things currently stand, it is also a positive story of the country’s institutions resisting to pressure.

Indeed, Senegal has come back from the brink, after outgoing president Macky Sall sought to delay the elections indefinitely, and which – thankfully – the Constitutional Council overruled. The vote on 24 March saw opposition candidate Bassirou “Diomaye” Faye win a resounding victory that precluded the need for a second round runoff. A former tax inspector and political novice, Faye had been released from politically-motivated imprisonment only days before.

Source: Senegal’s Presidential Office, via Reuters & Le Monde

Yet the triumph was above all for Senegalese democracy, with government candidate Amadou Ba conceding the next day. The country thus remains a beacon of democratic stability with peaceful transitions of power since independence in an otherwise fragile region that has recently suffered a wave of coups d’état: Mali, Burkina Faso, Niger, Guinea. Beyond West Africa, Sudan, Chad, and Gabon have each had recent, idiosyncratic, coup-like political instability as well.

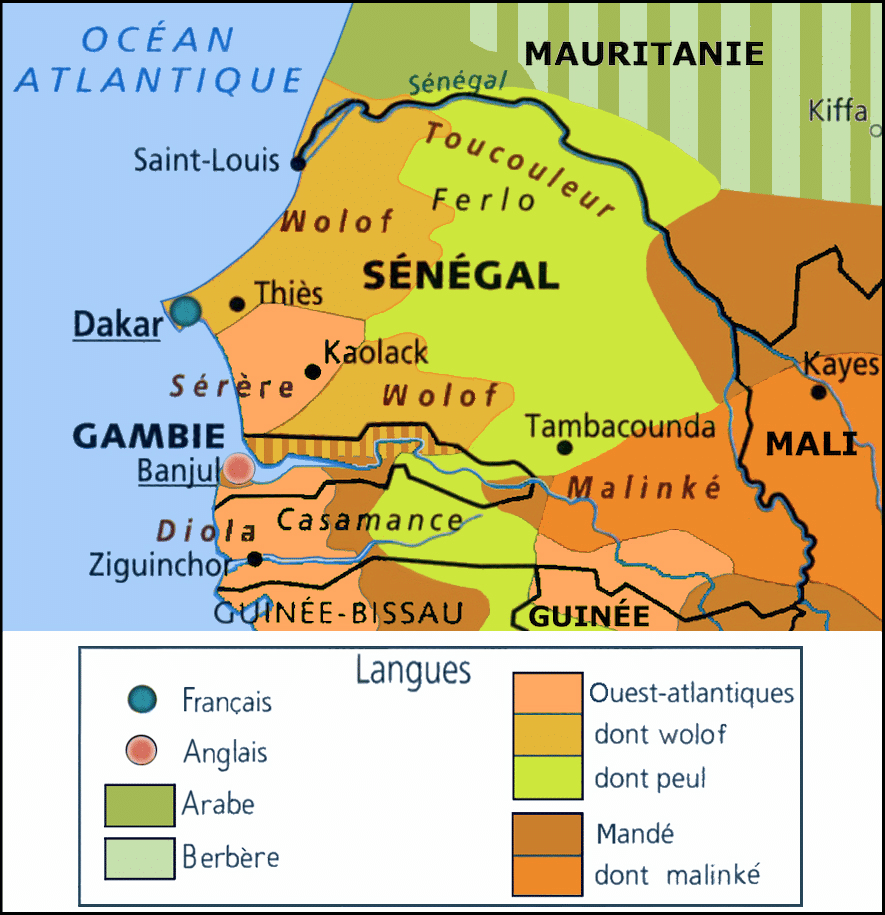

Mapping the ethnic X factor

I don’t want to exaggerate the importance of ethnicity in this election. For all intents and purposes, the result is a clear repudiation of Sall’s government and his anointed would-be successor, Ba, and overrides potential ethnic considerations.

Nevertheless, comparing a map of the electoral results to an ethno-linguistic map of Senegal suggests that ethnicity is still important. Sall is Fula (in French: Peul) and has had his political stronghold in the northern parts of the country, where many Fula live. These voting patterns were borne out in March’s election, with Ba getting much of his support from Fula-populated areas.

Source: Wikipedia

Source: G.G. Beslier, Le Sénégal

In contrast, Faye was much more dominant in areas populated by the Wolof, the Mandé / Malinké in the southeast and south, and in the southwest. Faye was until recently the right-hand man of Ousmane Sonko, who was ultimately prevented from running in the election. Sonko hails from the southwestern city Ziguinchor, where Faye secured a strong turnout, and has been chosen as prime minister.

The Sahelian ethno-democratic-demographic doom loop

On a continent that crams some 3000 ethnic groups speaking around 2100 languages into a mere 54 countries, it is myopic to completely ignore the ethnic undercurrents at play, even in cases where it isn’t the primary driver. Yet analyzing the political salience of ethnicity in Africa is more than just a useful intellectual exercise.

Think how, for example, as the largest nomadic pastoral community in the world, the Fula are present in Senegal and Guinea, and in Chad and Cameroon, and in every country in between. As climate change drives the Sahara’s expansion ever southward through the Sahel, we can expect land use-driven tensions to continue rising between the more martially-oriented nomadic pastoralists of the north and the more numerous sedentary agriculturalists to the south.

To that point on demographics, Western democratic ideals imposed on an African context partly explains many countries’ breakneck population growth. Individualism is at the center of the one-person one-vote approach to electoral democracy and works well in many parts of the world. But traditions of individual liberty were only introduced to African countries recently, where, historically, communitarian-led structures of societal organization tended to dominate.

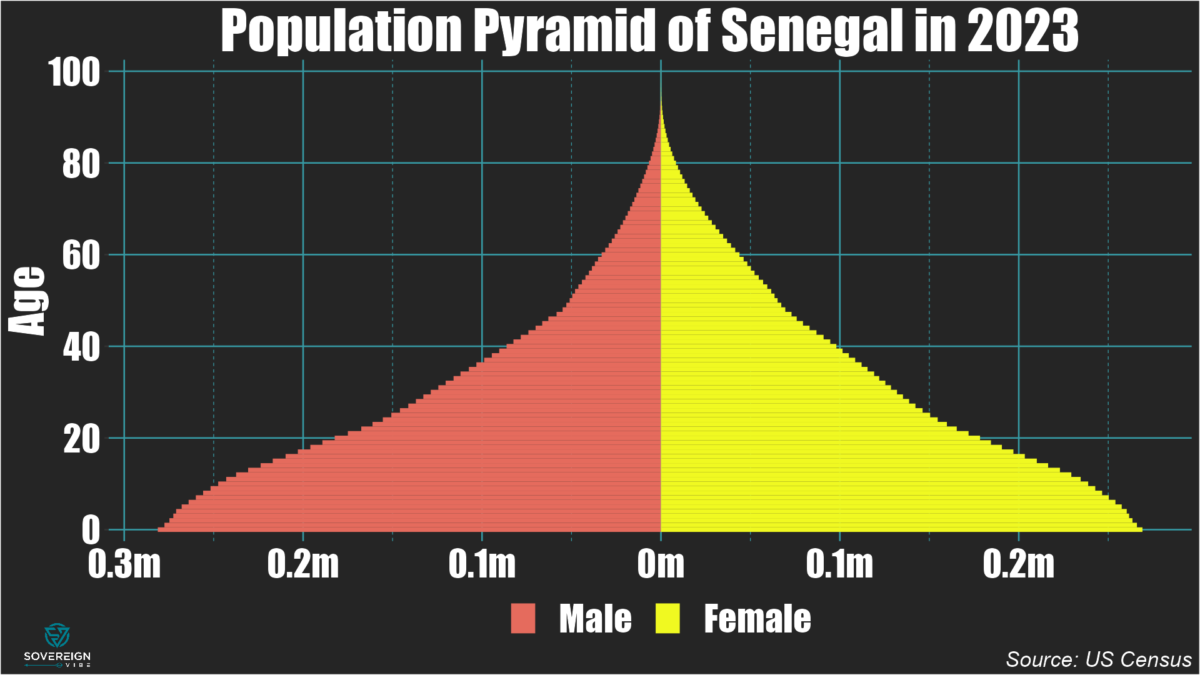

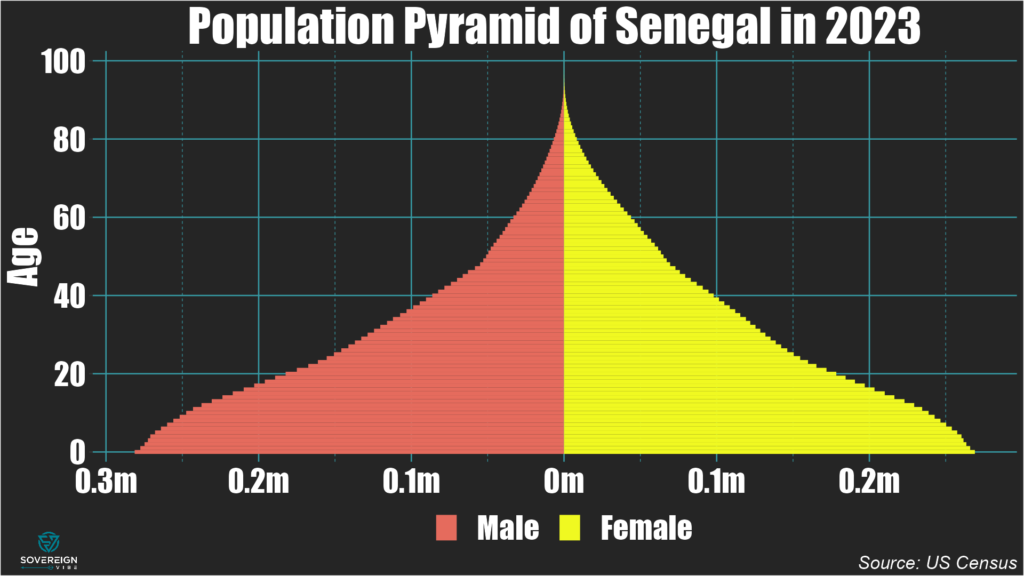

Senegal’s population is growing at a rapid clip.

Thus Western-style democracy has incentivized each ethnic group to vie for political power by growing its population. This makes complete sense if one recognizes the communitarian focus that continues to drive politics in so many African countries to this day. Case in point, as of 2023 Senegalese women give birth to four children on average, and 75% of the country’s population is under 35 years old. Of course, the usual caveat applies: no single factor is fully responsible for a demographic outcome.

The bitter irony is that democracy has destabilized several of Senegal’s neighbors precisely because it has inverted the power relationship between the previously-dominant nomads and the sedentary farmers. Historically, these fierce warrior-pastoralists didn’t really require strength in numbers to subjugate their more pacific southern neighbors.

But in a context where democracy excludes the nomads from political power, it should not be at all surprising that these peoples would try to revolt or secede. This is precisely the driving force behind the ongoing conflicts and instability across the near-entirety of the Sahelian arc, rather than some inchoate jihadism. The several Tuareg / Azawad rebellions that have occurred since the 1960s serve as a prime example. Senegal alone has been spared. For now.

With all that in mind, can a victory of democracy in an African context be anything other than a pyrrhic one? I certainly hope so, and Senegal’s institutions give good reason to. Yet even as this result is rightly celebrated, the specter of roiling demographics and instability throughout so much of the region looms large over West Africa’s future.

What next for investors?

Investors have so far reacted to Faye’s victory with caution, as he is in many ways an unknown entity. It is still early days, so investors ought to remain circumspect while waiting to see the shape that his economic policies end up taking.

For now, what we know from Faye’s inauguration is that the economic agenda will focus on reducing cost-of-living pressures and on tackling corruption, while also having to address the high unemployment rate in this youthful country. On the external front, Faye and Sonko have espoused sovereignty and deep change, including reforms to or a complete transition away from the CFA currency.

Abandoning the CFA could prove tricky, as the currency has been a source of stability throughout much of the region, aside from a sharp devaluation in 1994. On the other hand, Senegal likely has the policy credibility and institutional strength to pull it off. Moreover, the CFA is almost certainly highly overvalued, so the move to a more flexible currency could benefit export activity.

The French Connection

As for the relationship with France, Sall had kept close ties while also diversifying Senegal’s partners. It seems likely that Faye will keep Paris at arm’s length, without necessarily shutting the door entirely, if the cordial 30-minute conversation he had with Macron last week is anything to go by.

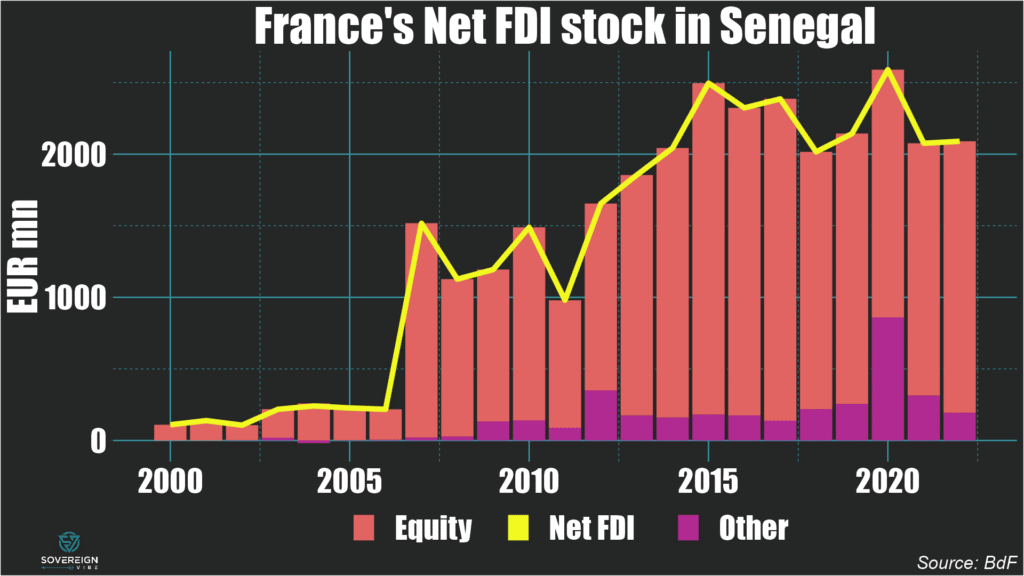

In the meantime, France’s net foreign direct investment stock in Senegal has remained above the €2bn mark in recent years, unlike declines in the French economic presence that have been registered elsewhere in francophone Africa. This level of FDI involvement in Senegal is close to 8% of GDP and represents nearly a fifth of FDI in the country, underscoring the ongoing presence that French economic interests are likely to have.

Today marks the grim anniversary of Russia’s full-scale invasion of Ukraine on February 24, 2022. Yet the conflict since 2022 is in many ways larger than the current military operations on the ground, both in terms of time and space. It is of course only the latest and most intense iteration of Russian aggression in the country, which started in earnest in 2014 with Russia seizing Crimea and launching military operations in the Donbas under the pretext of supposed separatism.

Spatially, events in Ukraine have global implications for geopolitical competition between the West and Russia, along with its allies of convenience – chief among them China but also pariahs such as North Korea and Iran. In tandem with the Covid-19 pandemic, the 2022 war in Ukraine marks the end of an era: the second of two death knells of the post-Cold War period.

Macroeconomic snapshot

Beyond the immense human toll, social disruption, and infrastructure destruction, the macroeconomic effects on Ukraine since 2022 have also been tremendous, obviously. The budget deficit went from a respectable -3.7% of GDP in 2021 to a gaping hole of nearly -30% in 2022, and possibly -20% in 2023. In 2024, the government’s shortfall is projected to reach $43 billion, which is probably equivalent to around a quarter of GDP.

Similarly, output dropped by about a third in 2022, with little in the way of recovery in 2023.

Output gaps have swung wildly in Ukraine since its independence. In percentage of potential GDP, IMF World Economic Outlook October 2023 data indicate:

These swung from positive double digits in 1992-1993 to negative double digits for the rest of that decade.

Actual output finally rose above trend in 2004, with the cycle accelerating until the global financial crisis forced a contraction in 2009.

Growth was recovering through 2013, until in 2014 Russia seized Crimea and began a covertly-led irredentist proxy war in Ukraine’s Donbas region. The output gap dropped to -10% in 2015.

From 2016 output rebounded again until the pandemic dampened activity in 2020, followed by a swift recovery to 2019 levels in 2021.

Since Russia’s full-scale invasion in February 2022, the output gap has once again plummeted, to -15% that year and to -10% in 2023.

Deglobalization, reglobalization, or slowbalization?

To be sure, deglobalization began at least as early as 2016, as that year saw the election of Donald Trump; the ensuing tensions with China and Iran; and Brexit. Global fragmentation has only worsened in the years since, with Covid; Ukraine and the related sanctions; and Joe Biden continuing Trump’s trade protectionism.

The world has now entered a new period in which countries are reconfiguring their trading relationships and supply chains in reaction to heightened geopolitical tensions, logistical frictions, and increased barriers to the movement of people and goods. The world’s borders have hardened, so cross-border movement is less fluid.

Hence the terms “deglobalization,” “reglobalization,” and “slowbalization,” though none of these encapsulates the nuances of what is happening. There is even evidence that international trade has rebounded strongly since the pandemic and that geopolitical alignment doesn’t explain much when it comes to international trade.

Still, the rafts of Ukraine-related sanctions; pandemic-related travel restrictions and supply chain disruptions; and trade reconfigurations such as “friend-shoring” or “near-shoring” are leaving their mark and, to a large extent, appear to have staying power. This is part of the reason I named this blog Sovereign Vibe.

21st-century global “stewardship”

It should come as no surprise that I, like Ukrainians and most of my fellow Westerners, consider the Kremlin to be at fault for the ongoing hostilities in Ukraine. Indeed, the Russian government is clearly responsible for seizing Crimea in 2014, jump-starting a war in the Donbas that same year, and fully invading the country in 2022. There are no legitimate justifications whatsoever for this aggression, Moscow’s propagandistic claims notwithstanding.

Yet the war in Ukraine is also symptomatic of Western, and chiefly American, failures in responsible global stewardship. Supporting Ukraine and opposing Russia is important in seeking an optimal outcome from a Ukrainian and Western point of view but provides no path forward on managing relations with Russia in the future.

The point is that there never should have been a war in Ukraine from 2022, or from 2014 for that matter. The heart of the problem is Russia’s revanchism under Vladimir Putin, which itself is an outcome in reaction to the Soviet collapse and ensuing chaos in Russia and the other newly-independent remnants of the USSR. This seems like an obvious point, but none of this was pre-ordained.

Geopolitical lessons

While authoritarianism under Putin is an outcome shaped almost exclusively by forces within Russia itself, the West missed a crucial opportunity in the 1990s to incentivize an erstwhile opponent into becoming an ally, much as visionary American and Western leadership did with Germany and Japan post-WWII. Although the USSR was not defeated militarily, observers should at the very least be able to imagine a post-Cold War order where Russia plays the role of a neutral cooperator, rather than an autocratic kleptocracy bent on geostrategic spoliation.

Shock therapy à la Dick Cheney

Western policy towards Russia failed miserably in the 1990s on at least two occasions. The first is in the immediate aftermath of the Soviet collapse, when Jeffrey Sachs and other Western economists advised the Russian government to adopt rapid market reforms, privatizations, and liberalization policies, known as “shock therapy.” Crucially, these advisors saw the need for significant Western aid to accompany these reforms, much as the Marshall Plan had helped Western Europe rebuild after WWII.

However, Dick Cheney, who was the US Secretary of Defense at the time, successfully pushed for shock therapy to be adopted without the aid. The predictable result was that, in the 1990s, Russia – and Ukraine as well as other former Soviet republics – suffered an economic and industrial collapse, a weakening of already-fragile institutions, a rise in poverty, and the emergence of robber barons who came to dominate the country’s politics.

“Dermocratia”

The second mistake of Western policy towards Russia flowed from the first. By the time Boris Yeltsin was up for re-election in 1996, Russian voters had become disenchanted with the economic suffering under the country’s new market economy and nascent democratic institutions. So much so that the term “dermocratia” was popularized, as a play on the words “democratia” and “dermo,” which mean “democracy” and “shit” in Russian, respectively.

Needless to say, Yeltsin was facing an uphill battle, but he had the support of the oligarchs, who were in fact more powerful than he was. Notably, Western governments also hoped to see him re-elected, as the chief opposition came from the Communist Party of the Russian Federation, which in some ways was the ideological successor to the Soviet leadership that had for so many recent decades been the US’s strategic foe.

To make a long story short, the election was marred by many irregularities, without which the communists might well have prevailed. Western capitals conveniently turned a blind eye to this meddling, further weakening the legitimacy of democratic institutions in the eyes of ordinary Russians.

No apologies

These Western mistakes in the 1990s are in no way an excuse for the authoritarian turn that Russia has taken under Putin. The Russian leadership alone is responsible for this outcome. Nor is the West somehow at fault for Russian aggression in Ukraine, Georgia, or beyond as a result of NATO expanding its European membership eastwards to countries willing to join of their own accord, as Putin apologists such as John Mearsheimer or Stephen Cohen claim.

But certainly American leadership in the 1990s under Bush and Clinton lacked the vision to try to bring Russia onside in the way that their more illustrious predecessors had done with Germany and Japan in the aftermath of WWII. Let this be a lesson for the future, as the West tries to imagine what Russia’s role in the world can and should be.

As tempting as it is to wish that Russia is a problem that would just go away, it won’t. Only by working backwards from “what good looks like” regarding Russia can Western leaders hope to address the root cause of the war in Ukraine, which is Russia’s revanchist position as international spoiler.

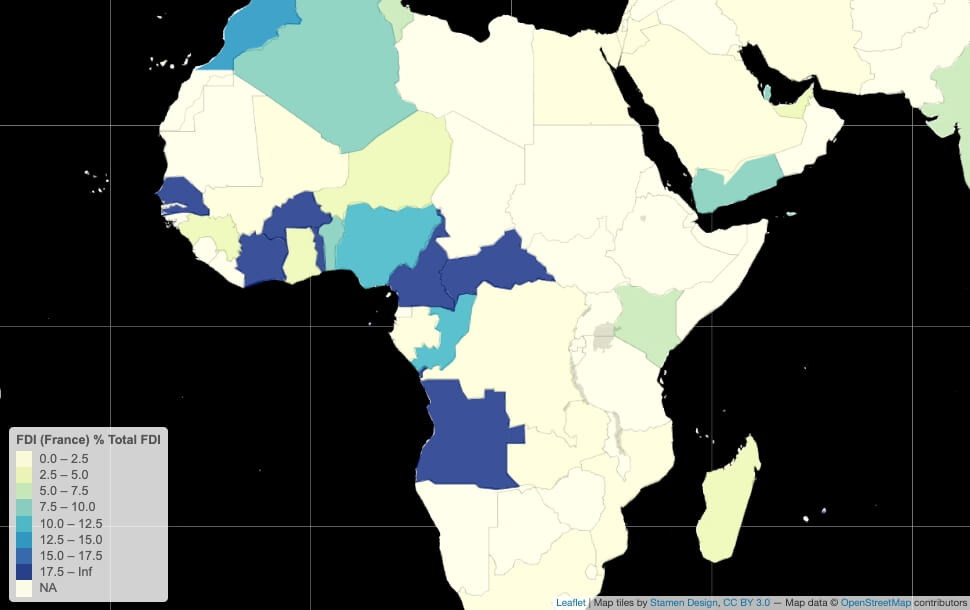

The recent wave of coups in Africa has increased scrutiny of France’s role on the continent. Looking at France’s net stocks of foreign direct investment in its former colonies reveals some surprises for those not closely monitoring these trends, and helps provide some sense of where Paris’s relations are with this group of countries. A snapshot of Franco-African economic relations helps debunk the oft-exaggerated importance of French influence in Africa, despite it being too early for a Françafrique post-mortem. Using foreign direct investment as a proxy delivers useful context for observers wondering where the next coup might strike, not as a causal factor, but as an illustration of heterogeneity.

As a percentage of all FDI in Sub-Saharan Africa by country, France is best represented in Senegal, Côte d’Ivoire, Burkina Faso, Togo, the Republic of Congo, Cameroon, and Angola. Of these countries, only Burkina Faso has experienced a coup d’Etat in recent years. French FDI as a percentage of GDP is highest in Senegal, the Congo, the Central African Republic, and Angola, and was also significant in Niger in the mid-2010s. The point is that the French factor, especially in the economic sphere, fails to shed much light on why any of the coups in Gabon, Niger, Chad, Burkina Faso, Mali, and Guinea occurred, each of which has its own idiosyncratic explanations.

Coup’s next?

As for the prospects of further military takeovers in Africa’s Sub-Saharan francosphere, Senegal and Congo appear the least likely candidates. In Senegal, President Macky Sall is not seeking an unconstitutional third term in the 2024 election, in keeping with the country’s history of political stability. In Congo, President Denis Sassou-Nguesso’s apparently ironclad grip on the country has shown no signs of wavering. In Cameroon, President Paul Biya’s late August military reshuffle could offer him some temporary protection, though the ongoing conflict with separatist rebels in its anglophone region is a source of risk.

None of the countries in the Sahel are completely immune from another putsch. In Chad, Mahamat Idriss Déby Itno’s future will depend on his ability to exercise control to the same degree as his father, the previous president. In Burkina Faso, 34-year-old Captain Ibrahim Traoré has already done well to last a full 12 months, while in Mali the Touaregs are a perennial thorn in Bamako’s side. Facing no credible threat of foreign intervention, Niger appears to be under tight control – for now.

Côte d’Ivoire’s 2025 presidential election is an upcoming flashpoint in an ethnic powder-keg, with President Alassane Ouattara already having changed the constitution to enable a third term from 2020. Since the International Criminal Court in the Hague acquitted former president Laurent Gbagbo of all charges in 2019, it’s a politically-explosive resurrection given the context of ongoing ethnic favoritism in Ivorian politics. To complicate matters further, the largest of the country’s three main ethnicities – Ouattara and Gbagbo hailing from the other two – hasn’t held the presidency since 1999, setting the stage for further grievances.

France FDI timelines

The charts below present a snapshot of how France’s FDI presence has evolved in select Central and West African countries, where Paris is regarded as having the most influence in Sub-Saharan Africa. As can be seen from the map above, its FDI presence is weaker in East and Southern Africa, even where it once had a colonial presence (e.g. Madagascar, Comoros, Djibouti). The high-level overviews presented below focus only on broad aspects of France’s investment footprint in these countries and often overlook the activities of French groups with a pan-African presence, including Total, Bolloré Africa Logistics, Air Liquide, CMA CGM, and Castel, among many others.

Central Africa

With all eyes on Libreville following Gabon’s August coup, facile narratives of France’s relevance are overblown, historical, linguistic, and security ties notwithstanding. France’s FDI involvement in GDP terms was higher in Gabon than in any other Central African country at one point in the mid-2000s, though Congo has had more French investment stock as a share of its economy for most of this century. In dollars, however, Angola has attracted the largest quantity of French investment.

Use vertical slider to compare USD vs % GDP figures.

Gabon’s main economic drivers are the oil, manganese, and wood sectors, with a French presence in each of these and well beyond. The French oil major Total has ongoing but diminished activities, following its sale of some of its Gabonese assets to the Anglo-French oil company Perenco in 2021. The Euronext-listed metallurgical and mining company Eramet continues to operate the country’s chief manganese concessions, while the Rougier group is a significant wood processor and exporter.

Yet Gabon’s economic partnerships have been tilting away from France for over a decade. Singapore has been a major player in the country since the agri-business company Olam entered into a joint venture with the government in 2010 to create a Special Economic Zone. The Paris-listed oil junior Maurel & Prom continues to operate in Gabon but has been majority-controlled by the Indonesian state oil company Pertamina since 2017. In 2022, Gabon joined the Commonwealth, alongside Togo, another former French colony, even as Libreville’s trading relationships shifted away from France and towards Asian partners.

France is a leading foreign investor in Angola, accounting for 60 subsidiaries and 45 local companies that employ around 10,000 people – trailing only Portugal and China on this metric. France has benefited from President João Lourenço’s efforts to rebalance economic ties away from Chinese, Russian, and Turkish interests in favor of Western partners. The French presence is concentrated in the oil and oil services sectors, with Total, Maurel & Prom, and Technip among the major players. Total alone accounts for 40% of Angola’s national oil production and is one of the country’s largest employers, alongside the French brewer Castel.

Total’s presence accounts for a large share of France’s FDI footprint in the Republic of Congo, where most French companies operate in the oil services and construction sectors. French firms currently employ around 15,000 people, though this is down from over 25,000 in 2015. Italy, the US, and China are the other main foreign investors in the country.

West Africa

Côte d’Ivoire accounts for France’s highest stock of FDI in francophone West Africa, followed closely by Senegal. The latter being the smaller economy of the two, France’s presence in Senegal is heavier in GDP terms. There was also a strong French economic presence in Niger in the mid-2010s, according to the data from the Banque de France below, though this has fallen off sharply in recent years.

Use vertical slider to compare USD vs % GDP figures.

France is the largest foreign investor in Côte d’Ivoire, with around 240 subsidiaries and some 1,000 companies owned by French citizens. These investments are spread across numerous economic sectors, reflecting the highly-diversified nature of the Ivorian economy.

France also has the highest proportion of foreign investment in Senegal, though its share has declined markedly since the mid-2010s. This involvement is also spread broadly across economic sectors, including banking, retail, telecoms, and industrials.

In Niger, China, France, and Nigeria comprise the main foreign investors, with a focus on extractive and manufacturing industries. French FDI peaked in the mid-2010s amid rail infrastructure investments by the Bolloré logistics group, road investments by the uranium miner Orano, and uranium transport investments by the Necotrans/R Logistic group.